|

UNIVERSAL ASSET OWNERS

The UAO Daily Brief

Volume 1, Issue 53 · Monday, July 6, 2026 · 7:00am ET / 15:00 GST

SOVEREIGN WEALTH MONITOR · THE STATE ON THE CAP TABLE

|

|

|

|

LISTEN · THE UNIVERSAL OWNER

Today's episode — “Washington Wants Five Percent” · ~6 min.

|

The Scenario Lab's live read puts the headline probability at 40% (▲+15pp) that state equity participation in frontier AI advances within 12–24 months. The full editorial decomposition — five branches, and what would prove us wrong — is in today's deep dive below.

| Open the live scenario → |

The most consequential capital-allocation idea of the week did not come from an allocator. The Financial Times reported that Sam Altman has discussed OpenAI donating 5% of its equity — roughly $43 billion at its last valuation — to a new U.S. sovereign wealth fund. The important fact is not that Washington may get 5% of OpenAI. It is that a systemically important AI company is testing whether equity can become the price of political license.

Also today: one of Australia's biggest managers has removed government bonds from retirement portfolios entirely — “no longer a hedge” — just as Japan's GPIF, the world's largest pension fund, reported that domestic bonds were its only losing asset class in a ¥41.4 trillion year. And a U.S. heatwave is turning the AI power build-out into a social-license problem. Three stories, one thread: the register of who owns what is being renegotiated.

1. OpenAI proposed donating 5% of its equity to a US sovereign wealth fund → TechCrunch

2. AMP says bonds no longer a hedge, cuts from some pension funds → Bloomberg

3. US heatwave raises alarms over AI data centre energy demands → Al Jazeera

The UAO Daily Brief is institutional intelligence, not investment, legal or tax advice. Researched and edited by the UAO editorial desk; figures are sourced to named reporting, company disclosures, official releases or cited analysis.

1. OpenAI proposes putting Washington on its cap table — 5% to a new U.S. sovereign fund.

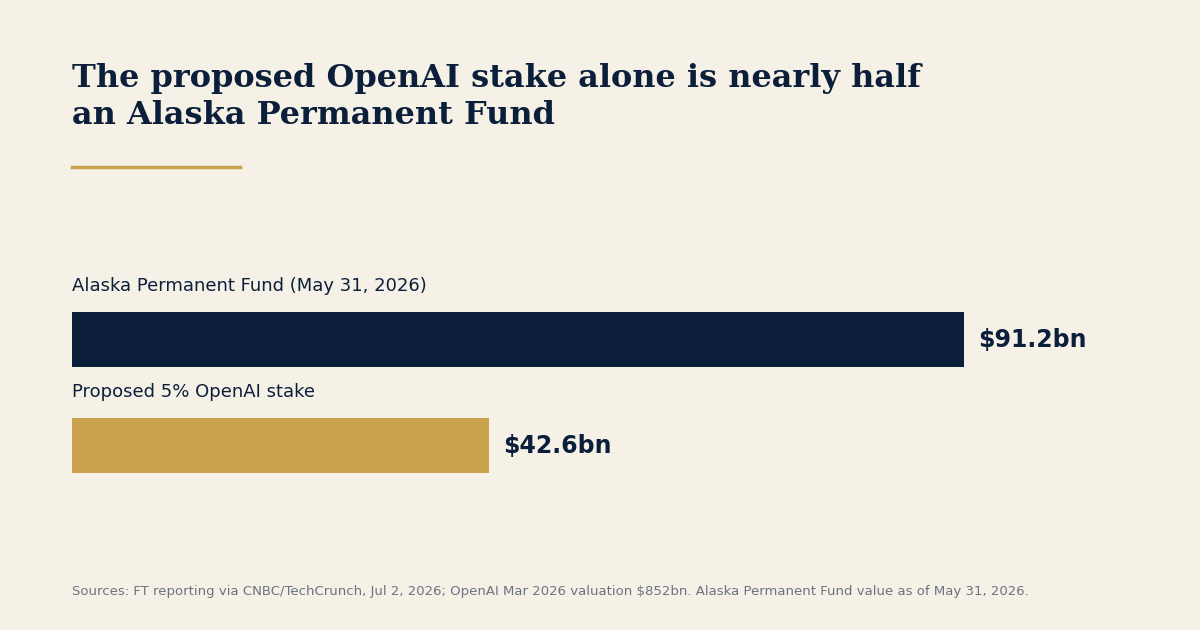

Sam Altman has discussed giving 5% of OpenAI's equity to a new U.S. sovereign wealth fund, the Financial Times reported on July 2 — a stake worth roughly $42.6 billion against the $852 billion post-money valuation set in OpenAI's March round. Altman reportedly suggested other leading U.S. AI developers — reporting named Anthropic, Google and Meta — could allot similar stakes, though there is no indication any have agreed; CNBC reported the administration and Anthropic have not discussed a stake. The talks, described as conceptual, were held with President Trump, Commerce Secretary Howard Lutnick and Treasury Secretary Scott Bessent, and any formal vehicle would likely require Congress. The precedent is no longer hypothetical: Washington has held a 10% stake in Intel since August 2025, converted from $8.9 billion in federal grants — and President Trump has said publicly he “should have asked for more.” The stated model is the Alaska Permanent Fund, created in 1976 and worth more than $91.2 billion as of May 31; the OpenAI stake alone (5% of $852bn = $42.6bn) equals roughly 47% of it. The wider pattern holds: Senator Sanders' AI sovereign-fund-by-levy bill was referred to Senate Finance on June 18, and Canada seeded its first federal sovereign fund with C$25 billion (about US$18 billion) in April. The contrarian case is on the record too — Bloomberg Opinion argued June 30 that a government that owns its AI companies cannot cleanly regulate them.

The counter-signal: the FT argued Monday that OpenAI and Anthropic may struggle to float at current marks — extreme infrastructure costs (OpenAI has committed over $1.4 trillion to data centers against roughly $14 billion in expected 2026 losses), model commoditization, and competition from Microsoft and Google cloud the profit pool — and Reuters reported in late June that OpenAI is weighing a delay of its listing to 2027. If near-trillion-dollar private marks need public markets to validate them, the “5% public stake” is not just political insurance. It may be pre-IPO valuation architecture: the state is being invited onto the cap table before the public market has voted.

Implication for owners: If your largest public holdings acquire the U.S. government as a fellow shareholder, the question is not the 5% — it is whose interests the other 95% is run for, and how a regulator-shareholder votes. Stewardship teams should have a position before they are asked for one.

| Read the full story → |

Sources: CNBC (FT reporting), July 2, 2026; Forbes, July 2, 2026; CNN Business, July 2, 2026; CNBC (Intel stake), August 22, 2025; Bloomberg Opinion, June 30, 2026.

2. AMP removes government bonds from pension portfolios — as GPIF shows the cost of holding them.

AMP, the Australian manager overseeing A$162 billion ($112 billion) as of February, has eliminated government bond holdings from its retirement portfolios for younger investors and cut allocations across other funds over the past six to twelve months, CIO Anna Shelley told Bloomberg on July 3. Her reasoning is structural: inflation is expected to stay elevated — “we're in a long-term, structurally difficult market for bonds — and we're not convinced that they will provide the diversification benefits.” The proceeds moved into corporate credit, commodities and agriculture, and funded an overweight in global equities that helped AMP's MySuper 1970s portfolio return 11.3% in the year through June 30. A pension manager going to zero, on the record, moves the stock-bond-correlation debate from allocation committees to boardrooms.

The counterpoint at scale landed the same day: Japan's GPIF — the world's largest pension fund — reported a 16.47% return for fiscal 2025, with ¥41.4 trillion in investment gains, its sixth consecutive positive year and second-best result on record. The detail that matters for the bond debate: domestic bonds were GPIF's only losing asset class — a ¥3.7 trillion loss as Bank of Japan rate hikes lifted yields — while domestic and foreign equities generated roughly ¥37 trillion of the gains. The world's biggest asset owner made its year on equities and lost money on its home bond book; that is the arithmetic AMP is acting on.

Implication for owners: The government-bond allocation is no longer a default; it is a position that must be argued for. Expect “what replaces the hedge” — real assets, commodities, cash optionality — to dominate allocation reviews into 2027.

Sources: Bloomberg (CIO Anna Shelley), July 3, 2026; GPIF fiscal 2025 results, July 3, 2026; Nippon.com (Jiji), July 3, 2026.

3. The AI power build-out meets a heatwave — and its social license.

A severe U.S. heatwave is straining power grids and water supplies just as AI data-center demand accelerates, Al Jazeera reported July 3 — and the friction is increasingly visible at the retail-utility level: in the Lake Tahoe basin, Liberty Utilities must secure a new wholesale power supplier for its roughly 50,000 customers after wholesale supplier NV Energy declined to renew its contract,* while Henrico County, Virginia — home to 37 data centers — asked schools to limit power use. The generation mix is bending to meet the load: natural gas's share of planned U.S. capacity additions has risen from 11.1% in 2024 to 18.1% in 2026, per American Action Forum analysis of federal data. Universal owners sit on every side of this: they hold the hyperscalers driving demand, they are buying the grids and generation meeting it, and their beneficiaries are the households competing for the same electrons.

Implication for owners: Treat social license as a priced risk in AI-infrastructure deals, not a footnote. The assets are long-duration; the public patience being drawn down is not — it flows into siting delays, interconnection queues and utility-rate politics.

| Read the full story → |

Sources: Al Jazeera, July 3, 2026; American Action Forum, 2026.

The proposed OpenAI stake alone is nearly half an Alaska Permanent Fund.

Sources: FT reporting via CNBC/TechCrunch, Jul 2, 2026 (5% of OpenAI's $852bn Mar 2026 valuation = $42.6bn, roughly 47% of the fund); Alaska Permanent Fund value ($91.2bn) as of May 31, 2026.

Why it matters: the fund Altman cites as his model took fifty years of oil royalties to reach $91.2bn. One AI company's 5% — $42.6bn, about 47% of it — would get there in a stroke, before any other company contributes a dollar. That is how fast equity, not revenue, is becoming the political currency of the AI era.

“When the state stops taxing the boom and starts owning it, every other shareholder's governance calculus changes. The universal owner's job this decade may be less about finding the AI trade than about negotiating who else sits on the register — sovereign funds, governments, and now perhaps the American state itself.”

If governments become shareholders in the companies they regulate, should universal owners treat AI governance as stewardship, policy risk, or sovereign-risk exposure?

The Fed, July 28–29. After June's projections raised the 2026 median to 3.8%, markets price one 25 bp hike by October — a hiking Fed into a softening jobs market is the macro tension of the quarter. FOMC calendar →

OPEC+ keeps adding barrels. Seven OPEC+ members approved another 188,000 b/d output increase for August on Sunday — a fifth consecutive monthly increase — and oil fell on the decision, with Brent easing toward $72 Monday. Cheaper oil cuts both ways for sovereign savers: softer inflows, easier inflation. CNBC →

Private credit's institutional bid. The FT reported Monday that direct-lending funds targeting large institutions raised at least $16 billion in the second quarter — the second-strongest quarter in four years — even as Q1 fundraising hit a three-year low and retail redemption requests set records. The institutional bid is strengthening as the retail bid weakens.

Temasek's annual review, expected this month. Watch the net-portfolio-value print and what it signals about Singapore's U.S. exposure. Temasek Review library →

Washington's next move on the AI fund. Whether Treasury or the White House formalizes anything before the August recess — and whether Anthropic, Google or Meta engage publicly. The state of the talks →

The State Buys In. — The four questions the owners of the other 95% should ask before Washington joins the register: governance, conflict architecture, the equity-for-license precedent, and the dividend that buys the build-out its social license — plus the UAO scenario map and what would prove us wrong. Full essay below and on the web.

When governments start taking equity stakes in your largest holdings, policy risk stops being a footnote. The Policy Risk Radar tracks live policy and regulatory risk signals for long-horizon portfolios — free on UAO.

| Open the radar → |

Issue No. 05 · July 5, 2026 · “The New Cap Table.” This week's flip-book edition — read it on the site or download the PDF.

| Read the flip-book → |

The State Buys In

The question. If Washington were to receive a 5% stake in OpenAI — and if that model were later extended to other frontier AI developers — what changes for the institutions that already own the rest? According to FT reporting on July 2, Sam Altman has discussed giving the U.S. government 5% of OpenAI's equity, worth roughly $42.6 billion against the company's $852 billion March post-money valuation, as part of a broader idea to give the public a financial stake in AI's upside. OpenAI executives reportedly suggested that other leading U.S. AI developers — reporting named Anthropic, Google and Meta — could allot similar stakes to a government vehicle, though there is no indication those companies have agreed; CNBC reported that the administration and Anthropic have not discussed a stake. The model being invoked is the Alaska Permanent Fund: created by constitutional amendment in 1976 and first funded in 1977, the public-wealth vehicle built from oil revenues stood at more than $91.2 billion as of May 31 and pays residents an annual dividend. Talks remain conceptual — held directly with President Trump, Commerce Secretary Lutnick and Treasury Secretary Bessent — and any formal U.S. vehicle would likely require Congress. The market question is immediate anyway: if the state joins the cap table, what happens to the owners of the other 95%?

The precedent is already on the books. The U.S. government has held a 10% stake in Intel since August 2025, converted from $8.9 billion in federal grant money — the largest direct federal equity position in an American industrial company since the auto rescues. President Trump has said publicly that he “should have asked for more.” Whatever one thinks of the Intel arrangement, it converted “the state as shareholder” from speculation into documented U.S. policy practice — the Altman proposal is the second data point on a curve Washington is already drawing.

Why the framing matters. This is not nationalization or a windfall tax — it is an offered gift, explicitly designed, per the FT, to “secure good relations with the administration and address political blowback.” That is precisely what should hold a long-horizon investor's attention: equity is being used as a political instrument by the companies at the center of the market's largest theme.

The valuation subtext matters too. A public wealth fund stake would not merely distribute AI upside; it could help validate it. OpenAI and Anthropic are approaching the point where private-market marks must be tested by public-market investors — and the FT argued Monday that both may struggle to float, pointing to extreme infrastructure costs (OpenAI has committed more than $1.4 trillion to data centers, with roughly $14 billion in expected 2026 losses), model commoditization, competition from Microsoft and Google, and uncertainty over durable foundation-model profits; Reuters reported in late June that OpenAI is weighing a delay of its listing to 2027. A government stake, especially one framed as citizen participation, could turn political risk into valuation support: the company becomes harder to attack, harder to tax punitively, and easier to describe as a national asset than a private monopoly. That is the uncomfortable allocator question: is public ownership a social contract, or a pre-IPO de-risking instrument?

Why this rhymes with everything else in 2026. In June, Senator Sanders introduced the American AI Sovereign Wealth Fund Act — a one-time 50% levy on the stock of “systemically important” AI companies, paid into a public fund his office values at an estimated $7 trillion; the bill was referred to the Senate Finance Committee on June 18, with no evidence of near-term passage, but it establishes the left flank of the same idea. In April, Canada launched its first federal sovereign fund, the Canada Strong Fund, seeded with a C$25 billion (about US$18 billion) federal contribution. States are converting policy leverage into equity ownership of the productive assets of the AI era — chips, grids, models — rather than merely taxing or regulating them. For Gulf and Asian sovereign readers this is a familiar playbook arriving in Washington; what is new is an issuer volunteering the stake.

Question one: governance. A 5% government stake is small enough to be passive on paper and large enough to matter in practice. Run the register arithmetic: at Alphabet, the largest institutional holders are Vanguard at roughly 7% and BlackRock at roughly 6%; at Meta, Vanguard holds roughly 8.5%. A 5% government block would arrive as an instant top-three institutional-scale holder of an index anchor — and at Alphabet and Meta, dual-class structures mean the economics would not carry control, which sharpens rather than softens the question: a holder that size without votes still has the regulator's phone. Does the fund vote? If it votes, it votes as a regulator-shareholder — the entity that sets export controls, procurement, antitrust posture and safety rules for the same companies. Every other holder of those names — which is to say, every universal owner, since these companies anchor the index — acquires a co-shareholder whose objective function is not fiduciary. The honest answer to “whose interests is the company now run for?” becomes genuinely plural.

Question two: conflict architecture. Bloomberg Opinion's June 30 case against an AI sovereign fund is the cleanest statement of the risk: once the state's balance sheet benefits from AI-company equity, its incentives entangle with the incumbents' — against open competition, against challengers, and potentially against enforcement. Universal owners have spent two decades pressing for independent boards and clean related-party rules; a government stake inverts the audit. The stewardship question writes itself into next proxy season.

Question three: precedent. If 5% buys regulatory goodwill in AI — after 10% bought Intel a strategic partnership — the template is portable: to semiconductors broadly, to pharmaceuticals, to exchanges. Long-horizon investors should price the possibility that “equity for license” becomes a recurring feature of U.S. industrial policy, as it already is in parts of Asia and the Gulf. That moves discount rates on politically exposed cash flows in both directions: lower policy risk for incumbents inside the tent, higher entry barriers priced against everyone outside it.

Question four: distribution. The Alaska model's genius is the dividend — it converts abstract national wealth into a check households defend. An AI fund that pays citizens a dividend would build a political constituency for AI profitability itself. For owners worried about the social license of the build-out — this morning's heatwave story is the live example — that is the most underrated feature of the proposal: it is an attempt to give the public a reason to want the data centers to win.

UAO Research estimates, not reported facts — the editorial decomposition of the Scenario Lab's live 40% headline read.

45% — OpenAI-only or narrow pilot. A non-voting or passive public-benefit vehicle is explored, but Congress limits the design. No full Alaska-style dividend.

25% — No equity deal; the idea mutates. The 5% proposal fails politically, but the principle survives as levies, procurement conditions, or AI-infrastructure fees.

15% — A broader AI public wealth fund gains traction. Other labs resist, but the Alaska/Norway-style model stays alive as AI job-displacement anxiety grows.

10% — Equity-for-license spreads beyond AI. Semiconductors, rare earths, grid infrastructure, defense tech and pharmaceuticals become candidates.

5% — The citizen dividend becomes the policy center. A true “AI dividend” emerges as the compromise between populist pressure and industry self-preservation.

What would prove us wrong: an explicit White House or Treasury statement ruling out equity participation; Anthropic, Google and Meta publicly refusing with no congressional text by year-end; or an OpenAI listing that proceeds with no public-stake feature attached.

Allocator posture. This is not a trade. It is a governance file. Universal owners should prepare three positions before the issue reaches proxy season: first, whether they support government co-ownership of index-defining companies at all; second, whether any public stake must be non-voting, arm's-length and Santiago Principles-compliant; and third, whether “equity-for-license” should be treated as lower political risk for incumbents or higher rule-of-law risk for the market as a whole. The difference between a Norway-style arm's-length fund and a politically directed industrial-policy vehicle is not cosmetic. It is the difference between a new fellow LP and a new governance risk factor. The owners best placed to shape that design are the ones reading this.

Sources: CNBC (FT reporting), Jul 2, 2026; TechCrunch, Jul 2, 2026; Forbes, Jul 2, 2026; CNN Business, Jul 2, 2026; Bloomberg Opinion, Jun 30, 2026; PMO Canada, Apr 27, 2026; Reason, Jun 2, 2026; CNBC (Intel stake), Aug 22, 2025; NPR, Aug 22, 2025; GPIF fiscal 2025 results.

An earlier version of this brief stated that “roughly 50,000 customers near Lake Tahoe were told to find a new power provider amid data-center-driven demand.” That framing was imprecise, and we have corrected it. The ~50,000 figure is the customer base of Liberty Utilities, the local electric utility. It is Liberty — not its customers — that must secure a new wholesale power source, after its wholesale supplier, NV Energy, declined to renew their contract (announced March 2026, since extended to the end of 2027 and tied to NV Energy’s Greenlink West transmission project, with the transition expected around 2028). Liberty has stated publicly that customers will not lose service during the transition. NV Energy cited data-center demand in northern Nevada among several factors, including transmission constraints; the NV Energy–Liberty arrangement dates to 2009 and was always intended to be temporary. We thank the reader who flagged this. — The UAO Editorial Desk

|

UNIVERSAL ASSET OWNERS

Intelligence for long-horizon capital. The UAO Daily Brief is published each weekday at 7:00am ET.

universalassetowners.com |