A single strait moves oil, LNG, inflation, rates, shipping and defense at once — and it's back. Plus private credit meets its stress test as it's sold into the 401(k), and Temasek maps the AI-and-income barbell.

UAO EditorialJuly 8, 20268 min read

Universal Asset Owners

The UAO Daily Brief

Volume 1, Issue 55 • Wednesday, July 8, 2026 • 7:00 am ET / 15:00 GST

The story that changed the portfolio overnight is not a deal — it is a chokepoint. Renewed conflict in the Strait of Hormuz has put oil, LNG, shipping, insurance, inflation, rates and defense back into a single transmission channel. It lands in the same 24 hours that private credit is being pushed into the $13tn 401(k) system exactly as HSBC pulls back and the Bank of England warns — and that Temasek maps where long-duration capital goes next. Today: why Hormuz is a universal-owner shock, not a headline; private credit's retail push meets its stress test; and Temasek's AI-and-income barbell — plus the hidden correlation tying them together.

• US strikes Iran, revokes oil waiver after Hormuz attacks — Axios

• Bank of England, Financial Stability Report, July 2026 — Bank of England

• Temasek's record portfolio and 2031 map — Global SWF

Today's Intelligence — Top Stories

1. Hormuz is back in the portfolio.

On July 7, after Iranian attacks on three commercial vessels in the Strait of Hormuz — a Qatari LNG tanker struck and left at risk of exploding, a Saudi crude tanker damaged — the US struck more than 80 Iranian targets, including 60-plus IRGC fast-attack boats, and revoked the waiver that had permitted Iranian oil sales; Iran said it hit US installations in Bahrain and Kuwait. The Joint Maritime Information Center raised transit risk to "severe," and some tankers turned back or went dark. CNBC, Jul 7.Axios, Jul 7.

Markets repriced fast. Oil rose around 5%, Brent back toward $76, after President Trump said the interim de-escalation was "over"; the US 10-year Treasury yield pushed toward 4.5% and Japan's 30-year yield hit a record high; Gulf tanker rates jumped toward $300,000 a day. Notably, the reaction was contained — oil held well below the early-2026 war peaks and back-channel diplomacy is not formally dead.

Implication for owners. Hormuz is not foreign policy — it is a transmission channel. A single chokepoint that carries roughly a fifth of the world's oil and gas moves energy prices, inflation expectations, central-bank policy, shipping and insurance costs, Gulf sovereign risk and defense budgets at the same time. This is the shock a universal owner cannot diversify away: it hits the whole portfolio on one day — and it lands just as the June NY Fed survey put one-year inflation expectations at 3.7% (three-year 3.3%), the highest in years, even as the labour market cools. NY Fed, Jul 7. The Fed is trapped between a softening jobs market and a fresh oil-inflation impulse; the policy paths are already diverging — on July 8 the Reserve Bank of New Zealand raised its cash rate 25bp to 2.50%, its first hike in three years. Bloomberg, Jul 8.

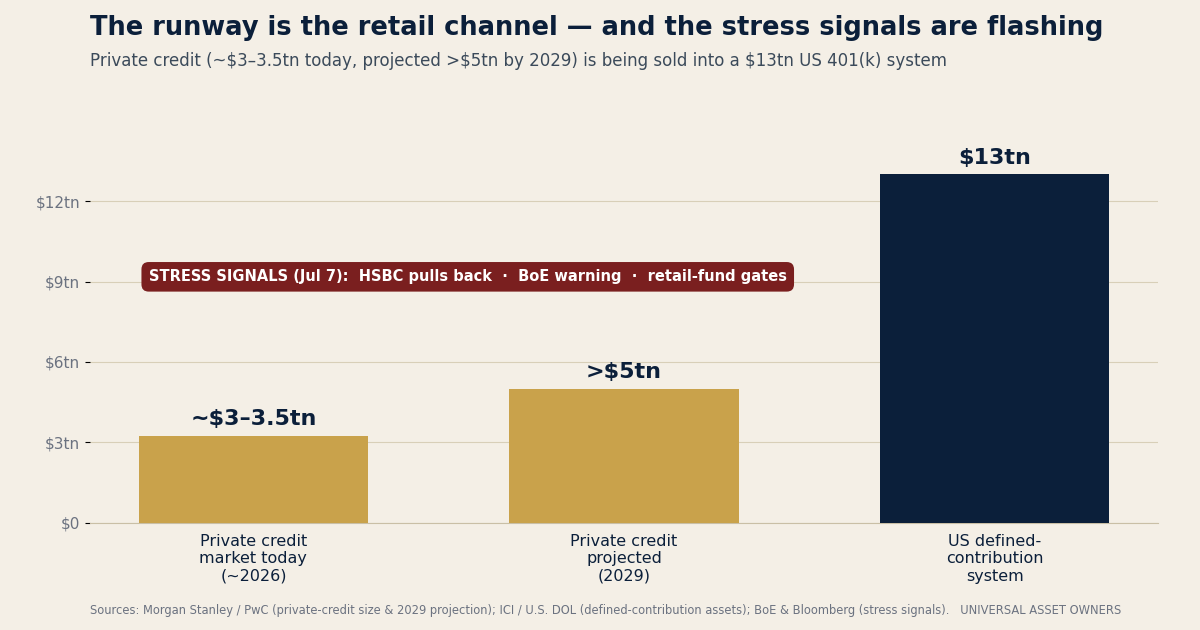

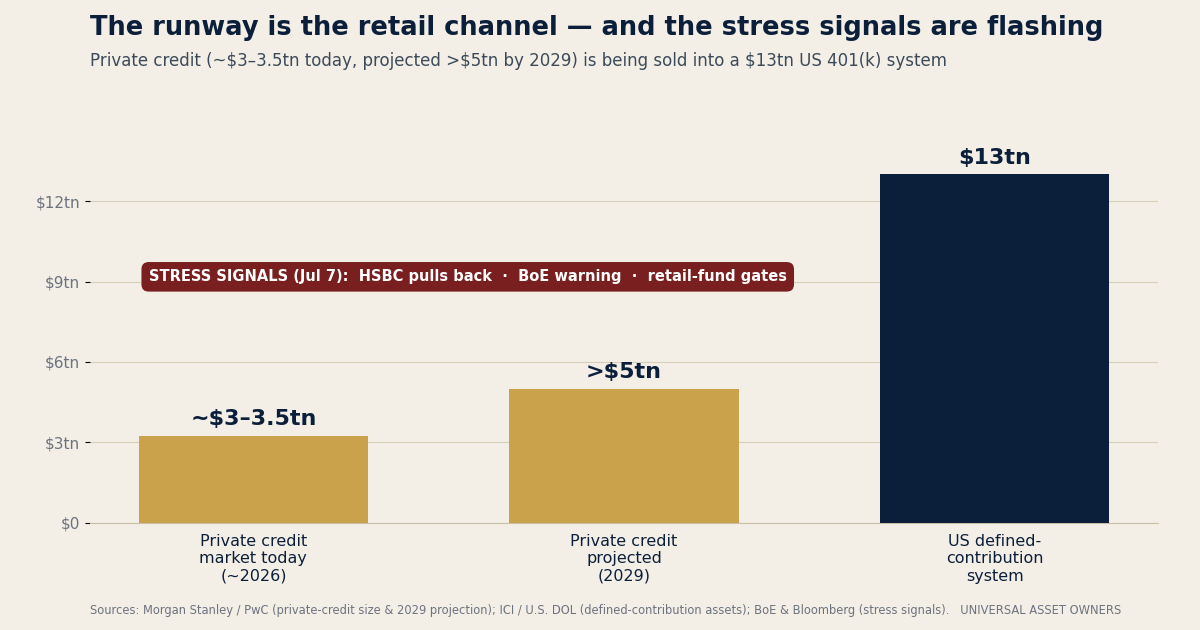

2. Private credit is being retailed just as the stress signals arrive.

The US is moving toward a process-based safe harbor that would give fiduciaries an asset-neutral safe harbor — widely expected to open the door to private equity and private credit — inside the $13tn 401(k) system — the DOL's proposed rule (comment period closed June 1) is still a proposal, but the products are ready: BlackRock has said it plans a LifePath fund holding private assets (~5–20% by age), and Empower has aligned with Apollo, Goldman and Blackstone. MoFo.PLANADVISER.

But the last 24 hours delivered the counter-evidence. HSBC said it will retreat from riskier private-credit lending after a roughly $400m loss (a fraud-linked collapse at the lender, not a systemic default wave) and paused a planned $4bn own-fund commitment. Bloomberg, Jul 7. The same day, the Bank of England's Financial Stability Report warned that risky credit — private credit included — is vulnerable to tighter conditions, flagging elevated retail-fund redemptions (some already gated), valuation opacity, leverage and interconnectedness. Bank of England, Jul 2026.

Implication for owners. Private credit is now roughly $3–3.5tn, projected past $5tn by 2029 — fed until now by institutional LPs paid an illiquidity premium to lock capital up. A wall of price-insensitive DC money compresses that premium; a daily-valued 401(k) is the hardest possible wrapper for an asset that does not trade; and when a lender as large as HSBC steps back on underwriting quality as the retail channel opens, incumbents must ask whether they are the smart money exiting or the patient capital left holding the least-liquid tranche. The counter is on record: Americans for Financial Reform finds DC plans without alternatives outperformed alt-heavy DB plans, net of fees. AFR.

3. Temasek draws the sovereign allocation map: AI, private credit, core-plus infrastructure.

Singapore's Temasek reported a record net portfolio value of S$518bn (US$400.8bn) for the year to March 31 — a second straight record — on a 10.5% return, and set out an unusually explicit map: lift AI exposure to as much as 15% by 2031 (from ~6%); roughly double private credit toward a 5% target (from ~2%); and build core-plus infrastructure — renewables, nuclear, storage — toward ~5%. CNBC, Jul 8.Global SWF, Jul 8.

Implication for owners. As HSBC pulls back and the BoE warns, a sophisticated sovereign is increasing private credit — but deliberately: sized, senior-secured, income-oriented, linked to the AI and infrastructure build-out. The lesson is not "avoid private credit"; it is that retail private credit and sovereign private credit are diverging into two products with the same name. The Gulf makes the point from the other direction: Global SWF data show the region deployed a record ~$53.9bn across 108 deals in H1 2026, and Abu Dhabi's L'Imad — now ~$300bn after absorbing ADQ, working with BCG on a rebuild — is being engineered into a dealmaking powerhouse.

Policy & Capital Flow Watch

• Trade: The US declined on July 1 to extend USMCA in its current form — annual reviews now run toward a possible 2036 expiry, leaving North American supply chains and tariffs unresolved (a KPMG survey found ~42% of Canadian manufacturers weighing a US move). CSIS.

• Defense: At the Ankara summit NATO reaffirmed a 5%-of-GDP defense target by 2035 (3.5% core + 1.5% resilience) — a multi-decade allocation theme across defense, infrastructure and industrials. CRS.

• Chokepoints: As Hormuz risk hit "severe," Singapore and Indonesia declared the Strait of Malacca will stay free and toll-free — the world's trade arteries are repricing in opposite directions.

Research note — the hidden correlation

AI, power, private credit and geopolitics are one trade

The Bank of England's report this week did more than warn on private credit; it flagged financial-stability risks from AI — crowded positioning, leverage, cyber exposure and uncertain profit assumptions. Connect the wires: a Hormuz shock raises energy costs; AI raises power demand and data-centre capex; private credit and infrastructure finance that build-out; central banks face fresh inflation. The same portfolios are long AI equities, AI infrastructure, private credit, data-centre power and risky credit — and the correlation may only reveal itself in stress. That, not any single headline, is the universal-owner story. Bank of England FSR.

Allocator Radar — who moved capital in the last week

• Sovereigns are de-risking listed equity. Invesco's 2026 study (~$29tn surveyed) finds SWFs cut equity allocations to 30% (from 32%), with infrastructure now ~9% of assets — the fastest-growing alternative. Invesco.

• Public capital is funding the physical layer of AI. CPP Investments committed US$1.75bn to EQT's AI-infrastructure strategy (EdgeConneX; 10+ GW of data-centre capacity) — underwriting power and compute, not just data-centre equity. Bloomberg.

• Gulf capital chose mega-trends over noise. Gulf SWFs deployed a record $53.9bn across 108 deals in H1, including $1.7bn into India (biggest half since 2024), despite the regional war. The National.

The Big Picture

Geopolitics is now the organizing principle of long-term capital

Zoom out and today's headlines rhyme. CPP Investments has built a four-scenario "deglobalisation radar" with Oxford — 70-plus indicators across trade, capital, migration, policy and US-China relations — to treat fragmentation as investable, not just a risk to hedge. Benefits & Pensions Monitor. Roland Berger's July study finds geopolitical upheaval has overtaken interest-rate uncertainty as family offices' top external risk, pushing them toward private equity, infrastructure, precious metals and healthcare. Roland Berger. And Invesco's sovereigns are cutting listed equity toward infrastructure and private markets. Different pools, one move: from generic diversification to explicit geopolitical portfolio design.

From the research desk — this week's institutional reading

• Bank of England, Financial Stability Report (Jul 7) — private-credit liquidity mismatch, retail-fund gates, and AI concentration risk. BoE.

• Invesco, Global Sovereign Asset Management Study 2026 — ~$29tn of sovereigns cut equities to 30%, lean into infrastructure and private markets. Invesco.

• UNCTAD, World Investment Report 2026 — global FDI +6% to $1.6tn but concentrated in ~20 economies, increasingly around AI infrastructure. UNCTAD.

• Financial Stability Board, Vulnerabilities in Private Credit (May) — the systemic-risk backbone to this week's headlines. FSB.

Chart of the day

Sources: Morgan Stanley / PwC (private-credit size & 2029 projection); ICI / U.S. DOL (DC assets); BoE & Bloomberg (stress signals).

Scenario Lab — today

The Retailization of Private Credit

Trace the chain: a DOL safe-harbor rule → 401(k) inflows → a compressed illiquidity premium → a liquidity mismatch that, in a late-cycle downturn, turns a credit event into a liquidity event.

Deep dive — Private credit: democratization, or a permanent-capital exit ramp?

The question. Is lowering the fiduciary barrier to private assets inside the $13tn DC system a genuine democratization — or a permanent-capital distribution channel for the managers who need one? The last 24 hours sharpened it: as the regulatory door opens, a global bank pulled back, a central bank warned, and a sovereign leaned in — three institutions reading the same asset class three different ways.

The DOL's proposal reframes fiduciary duty from outcome to process — something a large manager can engineer at scale. But it remains a proposal; the fee and litigation fights are ahead. The incumbent's problem is structural: a $3–3.5tn market heading past $5tn has to be funded, and the institutional LP base is at target and net-selling secondaries. The retail DC channel answers that ceiling — vast, sticky, price-insensitive capital. If it becomes the marginal buyer, the premium compresses, sentiment-beta rises, and the hold-through-a-gate edge stops being scarce as it stops being valuable.

The fresh evidence. HSBC repriced underwriting after a ~$400m loss and paused a $4bn commitment. The BoE broadened the fragility case to leverage, opacity and interconnectedness and flagged retail-fund gates. Temasek is increasing private credit toward 5% — senior-secured, income-oriented, linked to AI and infrastructure. The same asset read as danger by a bank and a regulator and as opportunity by a sovereign tells you the label has stopped describing one product.

Allocator posture. Price today's vintages for a lower forward premium and higher correlation. Follow HSBC's discipline, not its headline. Be a disciplined seller of commoditized exposure into the retail bid. And if you are also a DC fiduciary, govern the tension of placing on your own menu an asset your investment office may be trimming — and that a central bank flagged this week.

Researched and edited by the UAO editorial desk. Figures trace to the named sources above. Where sources disagree — as they do on whether alternatives belong in retirement plans — we say so rather than average them.