Your benchmark made a bigger bet than you did

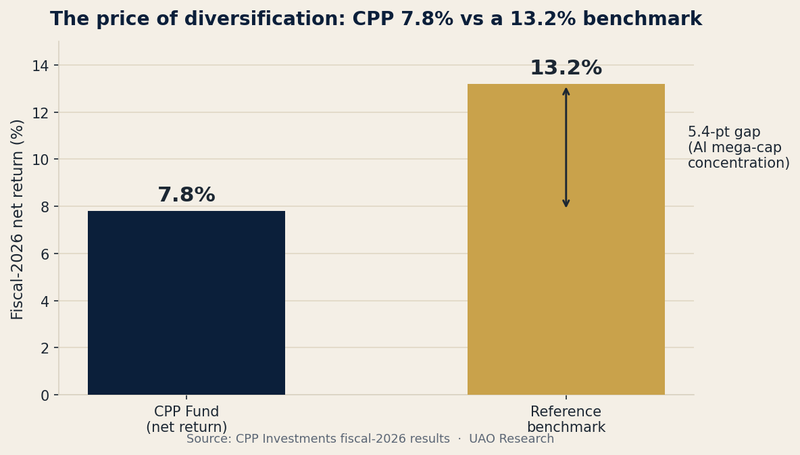

H1 ends with the allocator's uncomfortable problem: diversification reduced risk, but made portfolios look wrong against a concentrated index.

Briefings, research, charts and analysis on the institutions, capital flows and systemic risks shaping long-horizon portfolios.

H1 ends with the allocator's uncomfortable problem: diversification reduced risk, but made portfolios look wrong against a concentrated index.

H1 ends with the allocator's uncomfortable problem: diversification reduced risk, but made portfolios look wrong against a concentrated index.

H1 ends with the allocator's uncomfortable problem: diversification reduced risk, but made portfolios look wrong against a concentrated index.

H1 closes with breadth on the surface — and concentration underneath.

Test email preview - Issue 48

H1 2026 closed with diversification working - but the breadth had migrated to Asia and may already be the next concentration trade.

Value factor investing systematically targets underpriced equities using financial metrics. Institutional allocators use it as a core equity building block, though recent decade-long underperformance has tested conviction among large endowments and pension funds.

Multi-factor investing combines systematic exposure to proven equity factors to improve portfolio construction. Institutional investors increasingly blend factor tilts with traditional asset allocation for efficiency and risk control.

Currency hedging is a critical risk management tool for asset owners with global portfolios. This guide explains hedging mechanics, cost trade-offs, and governance frameworks used by major pension funds and sovereign wealth funds.

Quality factor investing systematically identifies companies with superior profitability, balance sheet strength, and earnings stability. Leading pension funds and endowments integrate quality screens into core equity allocations to reduce drawdowns while maintaining long-term growth exposure.

Momentum investing—the systematic exploitation of persistent price trends—has become a core component of institutional factor allocation strategies. We examine the mechanism, empirical foundation, implementation challenges, and fiduciary implications for sovereign wealth funds, pension funds, and en

Low volatility investing systematically selects securities with below-average price swings, offering reduced portfolio turbulence without necessarily sacrificing returns. Leading institutional investors have integrated this factor across equity allocations, though its effectiveness depends on market