|

The first half of 2026 closes today with the best Asian quarter in years and the Dow breaking 52,000 for the first time. But on Monday in Korea, the market fell — dragged down by just two chip names that now move the whole tape.

Breadth on the surface, concentration underneath. When the benchmark you are measured against becomes a concentrated bet, prudent diversification looks like underperformance.

A 50/50 barbell pairing climate-tech equity with carbon-project finance, developed with the GORD Council and the UN Environment Programme according to the fund materials. Rasmal Ventures — View the strategy deck →

1. The June 30 paradox: the market broadened and concentrated at the same time.

Reuters reported (Jun 30) Korea's KOSPI up 71% for the quarter (more than doubling YTD), Taiwan up more than 46%, and Japan's Nikkei reclaiming 70,000; an EM index rose roughly 22%. US large-cap also printed records — AP put the Jun 29 close at S&P 7,440.43, Dow 52,182.74 (a record), Nasdaq 25,820.14. Yet on Jun 29 the KOSPI fell ~3% — Samsung −5%, SK Hynix −3% — on foreign selling ahead of Korea's ~$1.3tn AI plan. Two chip names drag a whole national market down even as its quarter prints +71%: breadth on the surface, concentration underneath.

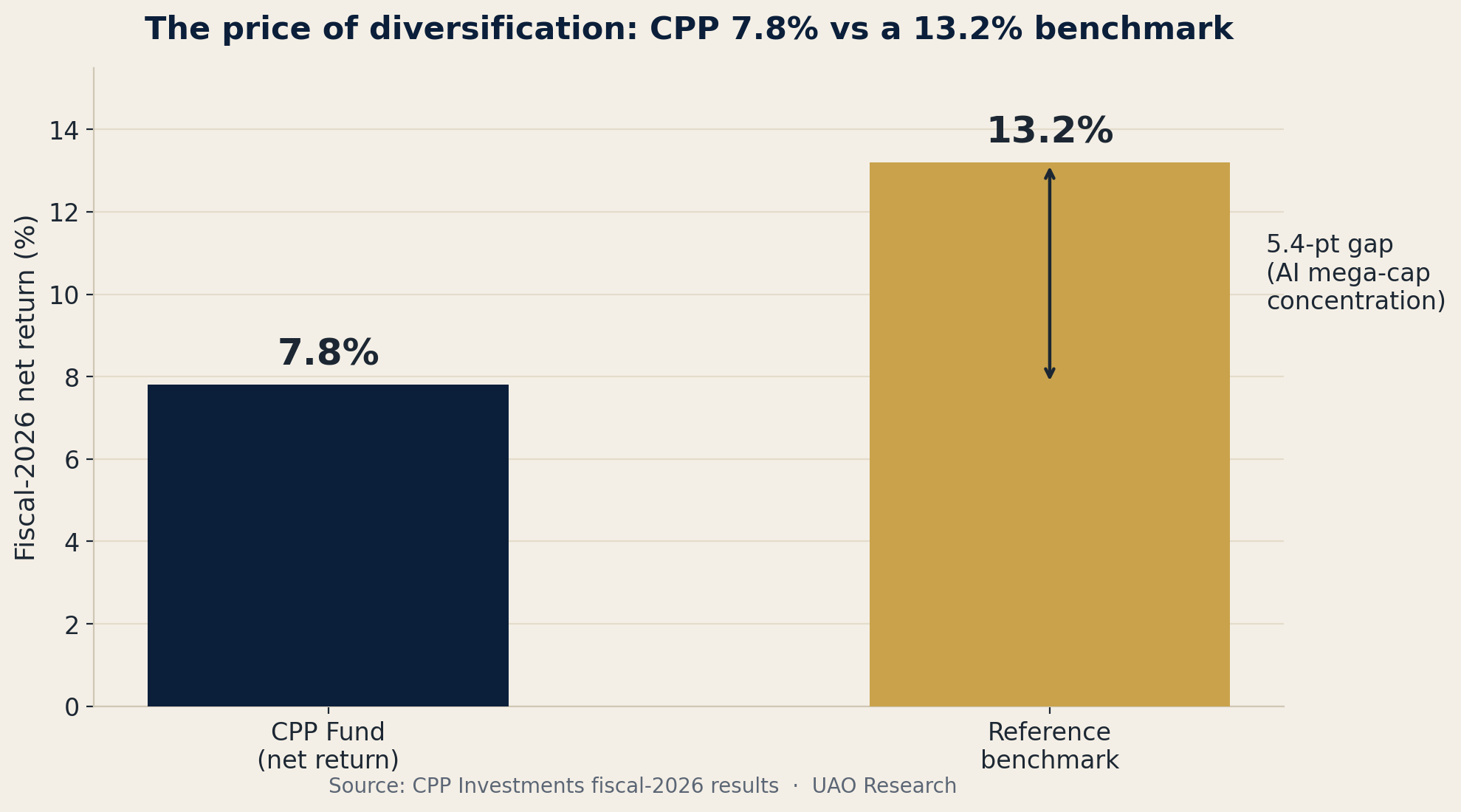

2. The evidence: CPP earned 7.8%, its benchmark 13.2%.

CPP Investments closed fiscal 2026 at C$793.3bn with a 7.8% net return — against a benchmark that made 13.2%. It blamed the 5.4-point gap on being diversified away from the AI mega-cap rally; over ten years it still beat that benchmark by 0.7% a year, calling the gap "a design feature."

3. The regime: a strong dollar fighting a structural gold bid.

May CPI 4.2%; Fed held 3.50–3.75%; the dollar was the best major currency (+~3%), pushing the yen to 161.98 (weakest since 1986). Gold round-tripped to ~$4,040 — yet central banks bought a net 244 tonnes in Q1.

4. The counter-trade closes next week.

The Macquarie-led A$11.7bn ($8.3bn) take-private of Qube is expected effective ~July 8, with Temasek (12.5%), GIC (6.59%), Korea's NPS (4.3%) and CalPERS (2.7%) backing it — patient capital buying control of hard infrastructure outside the listed mega-cap trade.

CPP returned 7.8% while its benchmark made 13.2%.

“H1 did not kill diversification. It relocated it — to Korea, Taiwan and Japan — and then started concentrating it again into the same AI supply chain. The job in H2 is to tell the difference between owning the world and owning the same bet twice.”

The Benchmark Became the Bet — top 20 S&P names = 49% of the index, 64% of its 5-yr return. Read the full deep dive.

| Read the full deep-dive → |