|

TODAY'S VIDEO BRIEFING · THE DIVERSIFICATION TAX

|

The first half of 2026 closes today with a lesson most benchmark reports will miss: diversification did work. It just did not look like a generic “own everything” trade inside the S&P 500.

The real breadth was outside the US mega-cap frame. Asia closed the quarter with historic gains — Japan's Nikkei up about 38% in Q2 (reclaiming 70,000), South Korea's KOSPI up 71%, and Taiwan up more than 46% — driven by the memory and AI-chip cycle. For a universal owner, that is the uncomfortable correction to the easy “AI concentration” story. The market did broaden — but into another part of the same supply chain.

That is the H1 problem for long-horizon capital. The investor who under-owned US AI mega-caps may still have captured the global AI-infrastructure trade through Korea, Taiwan, Japan and emerging markets. The investor who measured diversification only against a US policy benchmark may have missed the better question: did we actually own the global breadth — or did we simply own a different concentration? H1 did not kill diversification. It relocated it — and then started concentrating it again.

A 50/50 barbell pairing climate-tech equity with carbon-project finance, developed in partnership with GORD Council and the UN Environment Programme according to the fund materials. Rasmal Ventures — Full Spectrum Climate Fund I · View the strategy deck →

1. The June 30 paradox: the market broadened and concentrated at the same time.

H1 2026 closed on a powerful Asian quarter — and the same week showed why that breadth is a trap. Reuters reported (June 30) South Korea's KOSPI up 71% for the quarter (more than doubling year to date), Taiwan up more than 46%, and Japan's Nikkei reclaiming 70,000, all on the memory and AI-chip cycle; an EM index rose roughly 22%. US large-cap also printed records: AP put the June 29 close at S&P 500 7,440.43, Dow 52,182.74 (a record, above 52,000), and Nasdaq 25,820.14. Yet on June 29 the KOSPI itself fell about 3% — Samsung −5%, SK Hynix −3% — on foreign selling ahead of Korea's roughly $1.3tn AI investment plan. When two chip names can drag an entire national market down even as its quarter prints +71%, the breadth is real on the surface and the concentration is real underneath.

Implication for owners: The easy “US AI concentration” story missed where the market actually broadened. The real breadth trade was Asia, memory and semiconductors — and the uncomfortable twist is that this “diversification win” is already concentrating into the same AI supply chain.

Sources: Reuters (Asian markets, Jun 30, 2026); AP (US close, Jun 29, 2026); index levels via Trading Economics. UAO Research.

2. The owner's question: did you own the global breadth, or just a different concentration?

For the universal owner, H1 was a test of whether diversification was real or notional. The fund that holds the world by construction captured the Asia, Korea, Taiwan and EM breakout automatically. The home-biased active allocator had to choose it — and most did not, because the dominant narrative said the only trade that mattered was US mega-cap AI. The lesson is not “diversify more.” It is “diversify globally, and check what you actually own.”

Because the breadth has its own crowding. TSMC, Samsung and SK Hynix now make up close to a quarter of the MSCI Emerging Markets index. An allocator who captured H1's outperformance through Korea and Taiwan may have diversified away from US mega-cap concentration straight into Asian chip concentration — the same AI supply chain, a different passport. Genuine diversification in H2 means owning breadth that is not all one cycle.

Implication for owners: Run the look-through. If your H1 outperformance came from Korea and Taiwan, decide consciously whether that is diversification or a second helping of the AI trade — before the chip cycle decides for you.

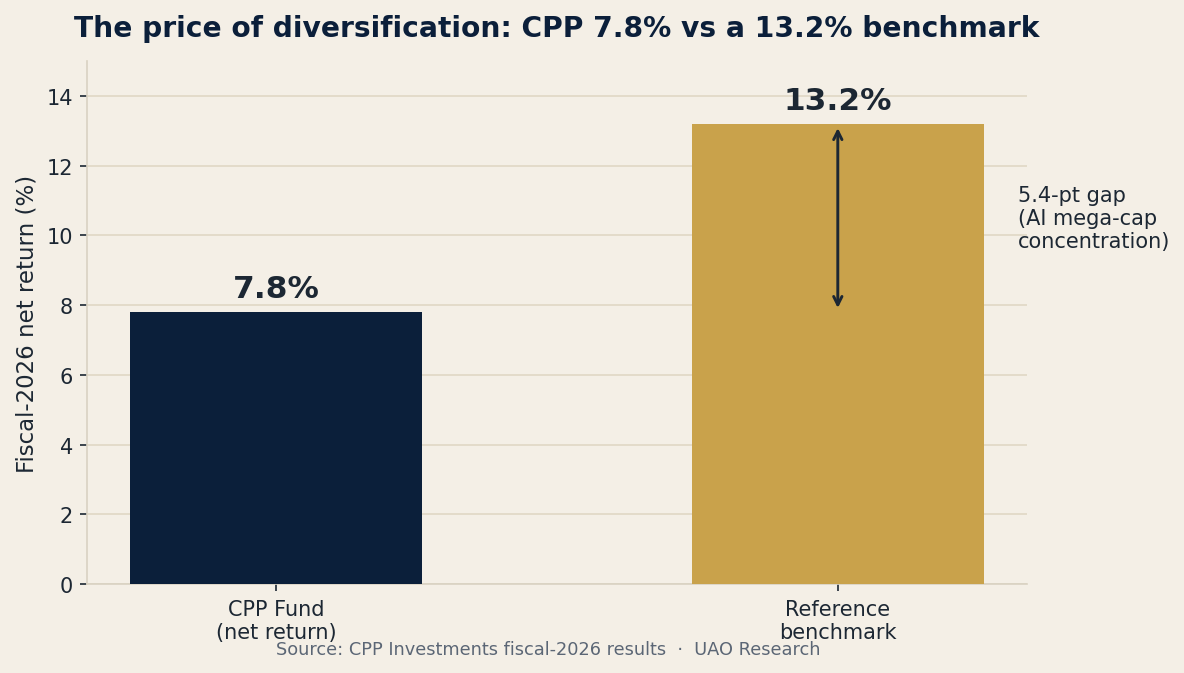

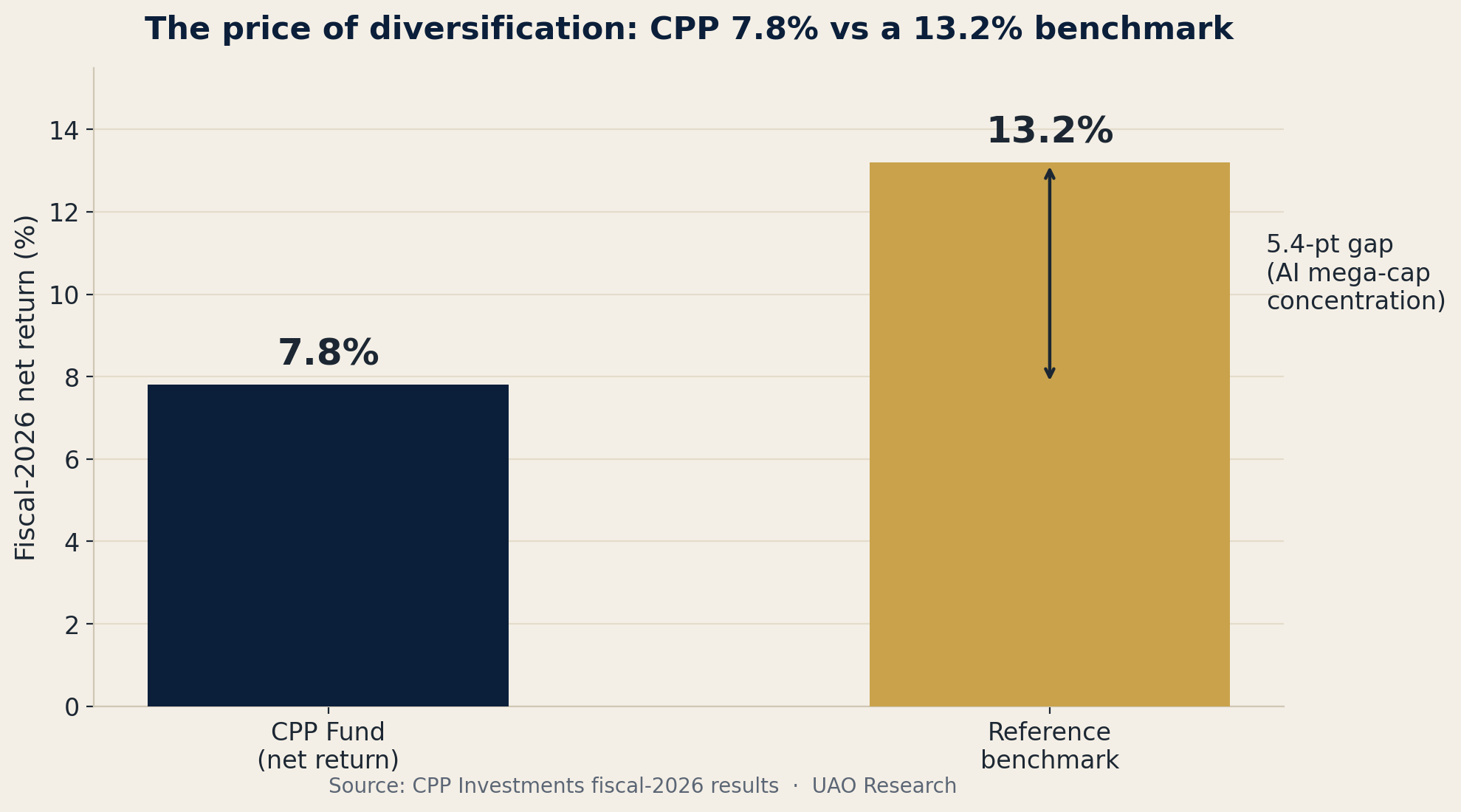

3. The May result that explains why today's H1 close matters: CPP's 7.8% vs a 13.2% benchmark.

The cleanest governance case study of the year is not today's news — but it is exactly why today's scoreboard matters. In fiscal 2026 (ended March 31), CPP Investments returned 7.8% and grew to C$793.3bn, while its own reference benchmark returned 13.2%. It attributed the 5.4-point gap to “the concentrated AI-driven rally in large-cap technology and communication services stocks that powered passive indexes but found less representation in the fund's more deliberately diversified structure.”

It showed what diversification can cost when the benchmark is being pulled by a narrow rally — though over ten years CPP still beat that benchmark by 0.7% a year, net of costs, and called the one-year gap “a design feature.” Read against today's close, the lesson sharpens: a US-anchored benchmark made the diversified owner look wrong, even as the real global breadth was paying off in Asia. The benchmark became a bet — and the diversifier's trade is starting to become one too.

Implication for owners: Your benchmark is no longer a neutral yardstick. Decide whether your tracking error against a concentrated index is a risk you are taking or avoiding — on the record, before performance attribution names it for you.

Source: CPP Investments fiscal-2026 results (reported May 21, 2026). Figures in Canadian dollars. Carried as a governance case study, not this-week news. UAO Research.

4. The reserve-manager layer: a strong dollar fighting a structural gold bid.

For central banks, SWFs and FX overlays, H1's defining cross-current was the dollar. Reuters put it as the best-performing major currency, up about 3% (DXY ~101) into H2 — pushing the yen to 161.98, its weakest since 1986, and reversing the dollar's worst first half since the early 1970s — on sticky May CPI of 4.2% and a Fed that held at 3.50–3.75% and flagged a possible hike. The strong dollar pressured gold, which round-tripped from a January record near $5,595 to roughly $4,040. Yet the structural bid did not pause: central banks bought a net 244 tonnes in Q1, with the Bank of Korea announcing its first gold-related reserve investment since 2013 via overseas-listed ETFs.

Implication for owners: Separate the FX overlay (cyclical, hedgeable) from the reserve-currency thesis (structural). Don't let one quarter's dollar strength close a ten-year question.

Sources: Reuters (dollar, H1 2026); FRED (10Y); Trading Economics (gold); World Gold Council.

5. What owners are doing while public benchmarks concentrate: buying what the index can't hold.

The clearest expression of the diversified response is in private markets. The Macquarie-led A$11.7bn ($8.3bn) take-private of Qube Holdings, Australia's biggest logistics and ports-and-rail operator, is expected to become effective on or about July 8, subject to remaining conditions (more than 98% of shareholders approved; the ACCC did not oppose), with implementation scheduled for August 14 — backed by Temasek (12.5%), GIC (6.59%), Korea's National Pension Service (4.3%), and CalPERS (2.7%). Patient capital is paying up for direct control of hard, cash-generative infrastructure outside the listed mega-cap trade. The discipline, as the deep dive argues: “outside the index” is only diversification if the underlying factor is genuinely different — logistics is; a hyperscaler-leased data center may not be.

Sources: Macquarie · Infrastructure Investor. Scheme effective ~Jul 8 (subject to conditions), implementation Aug 14. UAO Research.

The governance case study: CPP returned 7.8% while its benchmark made 13.2%.

Source: CPP Investments fiscal-2026 results. UAO Research.

The Benchmark Became the Bet

H1 did not kill diversification. It relocated it — and then started concentrating it again. Here is the governance problem underneath.

For fiscal 2026, CPP Investments returned 7.8% and grew net assets to C$793.3 billion. The benchmark returned 13.2%. CPP's own explanation matters: benchmark performance was driven by concentration in public equities, especially large-cap technology and communication-services companies tied largely to artificial intelligence, while CPP's diversified mix limited its participation in that rally.

That is the cleanest recent example of a deeper shift: the policy benchmark has stopped behaving like a neutral yardstick and started behaving like a concentrated allocation decision. Cap-weighted indices were never truly neutral — CFA and GIPS guidance has long warned that broad market-cap-weighted benchmarks can carry significant company and industry concentration. What changed is that the concentration is now visible, large, and pointed at a single theme.

The scale is concrete. BlackRock estimates the top 20 companies now account for 49% of the S&P 500 and contributed 64% of its five-year return; it puts AI-linked exposure at roughly a third of the S&P 500, versus about 8% in an ex-S&P-100 version of the index. A globally diversified owner now under-weights that theme relative to the index almost by definition.

And here is the twist H1 added: the obvious place to diversify away from US mega-cap AI — Korea, Taiwan, emerging-market chips — is the same AI supply chain. TSMC, Samsung and SK Hynix are now close to a quarter of the MSCI EM index. The diversifier's trade is itself concentrating. So the universal owner faces concentration on both sides of the ledger: in the benchmark it is measured against, and in the breadth trade it used to escape it.

This is where the risk moves from markets to governance. A one-year gap can be explained. A second year creates pressure. A third becomes a boardroom problem — consultants ask about tracking error, trustees ask why the fund is “missing” the market, staff are pushed to close it. And the simplest way to close a gap caused by under-owning mega-cap concentration is to own more of it, often after the crowd has already been paid. That is how prudent institutions get marched into crowded trades without ever formally deciding to take the risk.

The private-market answer is more complicated than it looks. Data centers, power, transmission, cooling, private credit, infrastructure and AI venture can create control, income and access — or be the same AI trade in another wrapper. McKinsey estimates global data centers need $6.7 trillion by 2030, including $5.2 trillion for AI workloads; Goldman Sachs estimates roughly $7.6 trillion of AI-infrastructure capex from 2026 to 2031. Private infrastructure diversifies away from public indices only if the underlying exposure is genuinely different. If the cash flows still depend on hyperscaler demand, chip cycles, power and AI monetisation, the owner has not diversified — it has migrated the same factor onto private balance sheets.

So there are four honest options.

One — own the concentration intentionally. Raise mega-cap or AI exposure if the IC believes the case justifies it — recorded as a decision, not smuggled in as benchmark compliance.

Two — budget the tracking error explicitly. Keep the diversified book, but tell the board in advance what relative underperformance is acceptable if mega-cap AI keeps leading. The failure is not the gap; it is pretending it won't appear.

Three — rebuild the benchmark architecture. Custom, capped, blended or liability-aware benchmarks that disclose concentration and factor exposure, and separate the policy benchmark from the reference portfolio. As MSCI frames it, concentration management is a governance decision as much as a portfolio-construction one. CFA/GIPS guidance already says to weigh benchmark construction and concentration when judging performance.

Four — manufacture real diversification, not cosmetic diversification. Private, real, credit and infrastructure should compete on a common risk-adjusted basis against public alternatives — not be assumed diversifying because they sit outside the index, and not be a second helping of the same AI cycle. This is the total-portfolio / relative-value path CPP itself uses.

The universal owner cannot stock-pick its way out of systemic exposure. It owns the market, including the concentration — and, this year, including the diversifier's concentration too. The discipline is to decide, consciously and on the record, how much of each you will hold. The funds that survive the next repricing will be the ones whose boards knew exactly how much AI beta they owned — in US mega-caps, in Asian chips, in private infrastructure, and in the benchmark itself.

The scenario: a sustained-concentration regime in which the passive benchmark keeps beating diversified owners long enough to force a governance capitulation — ICs lift mega-cap weights into the records to close tracking error, just as H1's breadth starts to broaden the market out (and then re-concentrate in Asian chips). Click any player and ask the desk what they do next.

| Open the live scenario → |

LISTEN · THE UNIVERSAL OWNER · “THE DIVERSIFICATION TAX” |

“H1 did not kill diversification. It relocated it — to Korea, Taiwan and Japan — and then started concentrating it again into the same AI supply chain. The universal owner's job in H2 is to tell the difference between owning the world and owning the same bet twice.”

• Asian chip concentration — whether the Korea/Taiwan/Japan breadth becomes the next crowded trade. • H1 fund letters — how many allocators report CPP-style tracking-error gaps. • Qube scheme (~Jul 8) — effective date and remaining conditions. • Fed path — a hike repricing would test the dollar and the mega-cap multiple. • Central-bank gold — whether Q2 buying held despite the price round-trip.

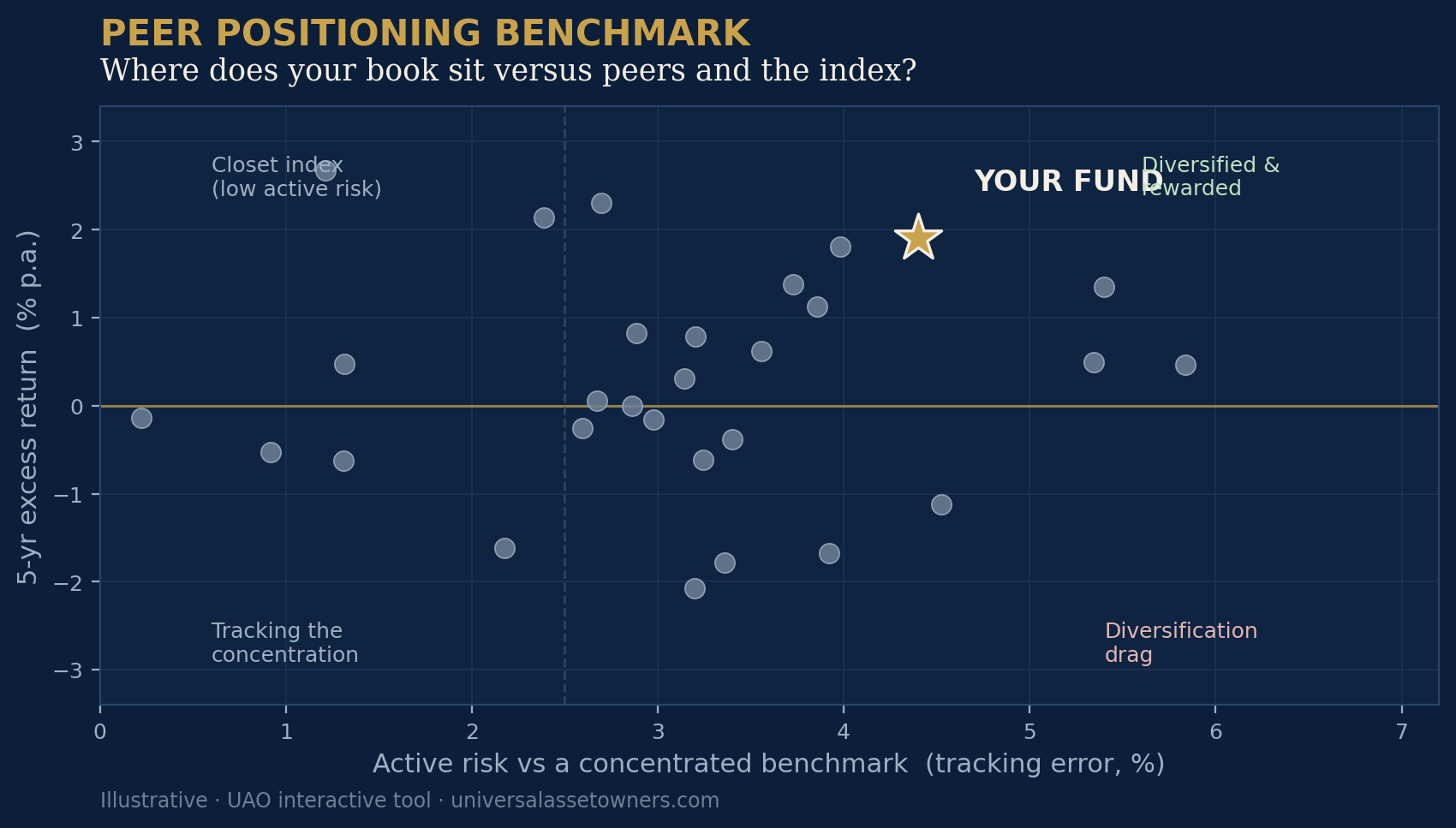

A free, interactive tool that shows where your allocation sits versus peers and a concentrated index — so you can see, before your board does, how much of your tracking error is a deliberate diversification choice.

| Open the tool → |

|

UNIVERSAL ASSET OWNERS

Intelligence for long-horizon capital. The UAO Daily Brief is published each weekday at 7:00am ET.

universalassetowners.com |