|

Today's edition is brought to you by

|

|

Watch · Today's briefing

The blockade returns — and the toll is paid through the insurance line, not the barrel.

|

|

The Lead

The blockade returns. The rules of passage don't.

Since the current conflict began early this year, moving oil through the Strait of Hormuz has carried a private risk premium — war-risk cover, crew-safety constraints, contract exclusions — that Washington could not abolish. In the last twenty-four hours it moved instead to put an official price on that risk. President Trump announced that the U.S. would reinstate a maritime blockade of Iran, with enforcement scheduled to begin at 4 p.m. ET (20:00 GMT) today — it had not begun at publication — and separately proposed that the U.S. be reimbursed 20% of cargo value for securing the strait. The UAE Ministry of Defence said Iranian cruise missiles struck two UAE tankers in Omani waters, killing one crew member and injuring eight. The U.S. said it had completed a third consecutive night of strikes on Iranian coastal defences. Brent settled 9.59% higher at $83.30, its largest percentage gain since May 2020 (~$84–85 early Tuesday). Iran's foreign minister called his country "always the GUARDIAN of the Strait" and dismissed the fee as a haggle — "20% is of course too much." That the dispute is already about the number tells you the frame has shifted from whether the corridor is open to who may price it.

For universal owners, the price move is the least interesting part. The important change is one of category: Hormuz is moving from a temporary supply disruption into a governance dispute over who may secure, administer, insure and monetise an international corridor. Be precise, because the market isn't: the blockade is announced and scheduled (it had not begun at publication); the 20% charge is only proposed — there is no published mechanism to collect it, and the IMO says there is no legal basis for charging ships to cross an international strait. Different facts, different half-lives.

Here is why the distinction still doesn't save you: a blockade, a proposed charge, and a legal rejection reinforce each other — and together they can reprice passage before any fee is ever collected, through war-risk insurance, transit declines and conditional access. The counterargument is real and belongs in the frame: neutral traffic remains permitted, no collection mechanism exists, and flows could normalise within days. So test the thesis against evidence, not rhetoric — vessel interceptions, war-risk exclusions, charter rates and transit counts after 4 p.m. ET. You can underweight a barrel. You cannot underweight the rules of passage. The scarce asset is no longer the barrel — it is reliable, insurable passage, and the capacity to underwrite it.

|

|

Today's Deep Dive

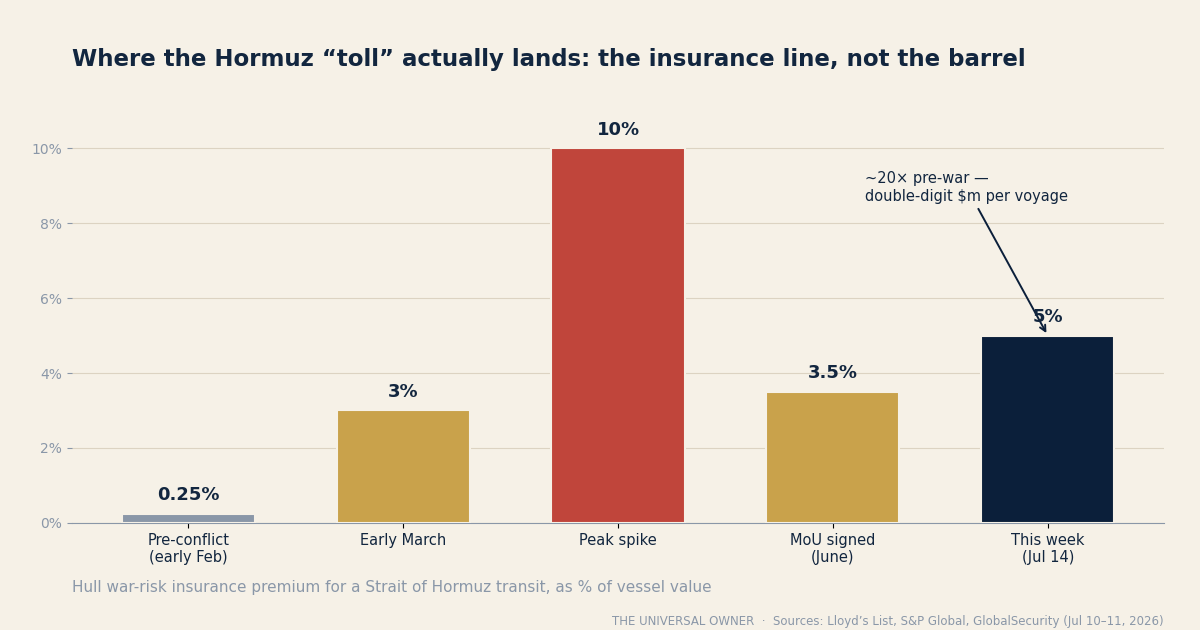

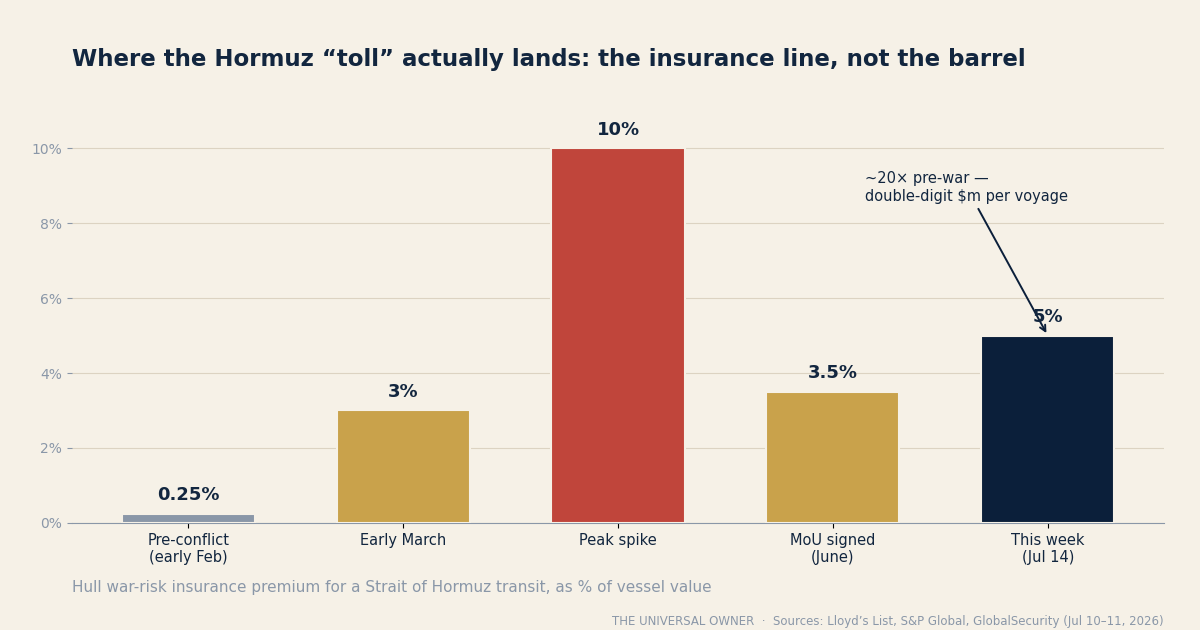

Chart of the day — the toll you're already paying. Hull war-risk premium as % of vessel value. Sources: Lloyd's List, S&P Global, GlobalSecurity, Jul 10–11.

When the chokepoint gets a price: it's paid through the insurance line, not the barrel

Before the war, insuring a hull for a Hormuz transit cost ~0.25% of the vessel's value. This week ~5% is an indicative level for some voyages — published quotes vary sharply by vessel, ownership nexus and cover period. Nobody voted for that rate; it is the truest gauge of what it costs to move energy through the Gulf, and the real channel into your portfolio, through underwriting capacity, freight, inflation and insurer solvency. Read against it, the proposed public charge is a second price on the same passage.

|

Hormuz has two prices · risk vs. access

Price of risk (insurance, real today). A single VLCC, hull ~$100–150m: war-risk at the pre-crisis 0.25% ≈ $250–375k per voyage; at ~5% ≈ $5.0–7.5m — a ~20× jump, before charter uplift or capacity withdrawal.

Price of access (the proposed toll, if applied). That same VLCC carries ~2.2m barrels; at Brent's $83.30 the cargo is worth ~$183m, so a 20% ad valorem charge ≈ $36.7m per transit. A levy that size doesn't tax passage — it ends it. The "toll," if ever collected, is a de facto blockade by arithmetic.

|

Why insurance is the transmission mechanism. For institutional portfolios, the Hormuz risk does not arrive as a barrel of oil. It arrives as a repricing of access that flows through four channels, in roughly this order:

1. Marine underwriting capacity. War-risk cover is written by a finite pool of specialist insurers and reinsurers. As premiums rise and exclusions widen, some underwriters withdraw from the route entirely. Capacity, not price, becomes the binding constraint — and when cover is unavailable at any price, the ship does not sail. That is how a strait that is legally open becomes operationally closed without a single new missile.

2. Freight and charter rates. Owners who will sail demand compensation for the risk and the insurance. Charter rates climb; the cost is embedded in every cargo. This is the "toll" that reaches the real economy, and it does so whether crude is $80 or $120.

3. Inflation and duration. Higher freight and energy costs feed headline inflation at precisely the moment central banks — Warsh's Fed, the Bank of Korea tightening this week — are deciding whether the disinflation of the last year was real or borrowed. A corridor premium that persists is a duration event, not a commodity event.

4. Solvency and claims. Insurers and reinsurers carrying shipping and property books are directly short this volatility. A single serious incident — and this week produced a fatality, aboard one of the two UAE tankers the UAE says were struck — converts a pricing question into a claims question.

The evidence that it is already binding. This is not a forecast; the transit data is turning over now. Ship-tracking and AIS analytics (Kpler-, Windward-style feeds, as reported) show Hormuz tanker traffic at multi-month lows — on one recent day only about 11 vessels against normal run-rates — with owners turning vessels back and AIS transponders switching off near Ras Laffan. When ships go dark and counts collapse, capacity is already the binding constraint. That is the "transit capacity" node lighting up before the toll is ever collected.

The hidden correlation — the positions that share one dependency. A large asset owner may hold, as separate and "diversified" positions, a set that is in fact long the same thing — reliable, cheaply insured passage through one corridor: Gulf sovereign debt; tanker and refiner equities; a marine reinsurer (short the volatility); an Asian LNG importer; inflation-linked pension liabilities (short via the liability side); and infrastructure financed on cheap-energy assumptions.

Under a Hormuz repricing, these do not move independently. They discover their shared factor at the same moment. Diversification across asset classes is not diversification across systemic dependencies. The universal owner's defining problem is that it owns the dependency.

|

The No-Regret Diligence Pack — for the investment committee / CRO

1. Map every position whose cash flows or valuations assume cheap, insurable Hormuz passage — by cargo, route, insurer and counterparty, not by asset class.

2. Stress a one-week and a one-month partial disruption — the grind, not the apocalypse. The one-day and the total closure are both already priced; the two-week impairment is not.

3. Audit war-risk and force-majeure clauses in shipping, trade-finance and infrastructure contracts before an incident triggers them. Know who bears the cost of a route that is available but uninsurable.

4. Decide whether any dollar-hedge unwind was conviction or drift. Pensions taking more FX beta into this shock should be able to tell a board which it was.

5. Run the combined scenario once — chokepoint + physical-climate (Bavi-style) + inflation — not in three silos. The risks compound; the model should too.

|

Both sides of the dispute. The counter-view is real and belongs in the frame. Neutral traffic remains permitted; no collection mechanism exists; mutual economic pain — U.S. consumers, Iranian revenue, global trade — creates strong incentives for a fast off-ramp, and Hormuz tensions have historically de-escalated before full closure. From the other side of the table, Iran's foreign minister Abbas Araghchi framed it not as a closure but a negotiation — Iran as "always the GUARDIAN of the Strait," with "20% … of course too much." For the Gulf producers, meanwhile, the episode cuts two ways: higher oil hands sponsors (PIF, Mubadala, QIA, ADIA) near-term fiscal room, even as it exposes the export-corridor vulnerability that has driven their deployment into resilience, bypass and clean-energy infrastructure through every prior escalation. This episode makes that diversification case louder, not quieter.

The commercial opportunity. Disorder in a corridor is also a capital-formation event. The same repricing that threatens existing holdings creates demand for the assets that route around the chokepoint: alternative export pipelines and ports, storage and strategic inventory, critical-minerals and diversified energy supply, and — pointedly — new insurance and reinsurance capacity for the risks the incumbents are fleeing. For the universal owner, the through-line is the same on both sides of the ledger: the scarce, monetisable asset is no longer the barrel. It is reliable, insurable passage — and the capacity to underwrite it.

Sources: Lloyd's List; S&P Global Commodity Insights; GlobalSecurity.org (war-risk rates, Jul 10–11); Bloomberg, Reuters (Brent, blockade, toll proposal, Jul 13); IMO statement / UNCLOS transit-passage (Jul 13); The National, The Hill, CNN (tanker strike, Jul 13–14); ship-tracking / AIS (Kpler-, Windward-style feeds, as reported, Jul 13–14); OPEC MOMR (Jul 2026). Toll status: PROPOSED — no operative collection mechanism at time of writing.

|

|

The Big Read

Hong Kong's Family Office Moment

Away from the Gulf, the other contest for the world's long-term capital is over where multi-generational money lives. Our feature on how Hong Kong reclaimed a razor-thin lead as a family-office base — and what the league table of capital centres tells allocators about the next decade.

By Universal Asset Owners Research

|

|

The other shock that arrived the same week: Typhoon Bavi

Chokepoint risk and physical-climate risk landed in the same 48 hours, into the same portfolios. Typhoon Bavi made a double landfall in eastern China's Zhejiang, forcing more than 2.68 million relocations there alone, flooding roads under two metres of water in Hebei, disrupting rail in Liaoning, and pushing 46 rivers past warning levels. The point is correlation: a portfolio long Gulf energy logistics and Chinese supply chains holds two "diversified" risks that a bad week fuses into one. Under stress, geopolitics and climate compound — they don't offset.

|

|

The macro collision: an energy shock meets Warsh's first testimony

Timing rarely cooperates this precisely. The shock hits the same morning as June CPI (8:30 ET, expected to ease to ~3.8% from 4.2%) and Fed Chair Kevin Warsh's first congressional testimony 90 minutes later. The disinflation the market is counting on was driven partly by falling energy prices — exactly what Hormuz now threatens to reverse. Markets already price a possible September hike. For long-duration owners, the disinflation glide-path just grew a geopolitical tail.

|

|

Asset-Owner Moves

CalPERS posts 14.8% — the year's first big number, with an asterisk. The largest U.S. public pension reported a preliminary 14.8% one-year return, lifting assets to $637.1bn, powered by a 24.1% public-equity year. It eases funding pressure; it doesn't resolve it. The figure is preliminary and listed-equity-driven — a reminder of how much of a "diversified" pension result still rides on the very assets most exposed to the CPI-and-oil collision above.

The quiet that is itself a signal. Across the strict 48-hour window there were no major new allocation announcements from the largest sovereign funds or pensions. Gulf funds gain near-term fiscal breathing room from higher oil even as their sponsors' export corridor is the one under threat — the diversification case just got louder. In the background, Canadian, Dutch and Danish pensions are unwinding dollar hedges as a hawkish Warsh lifts real rates — taking more FX beta into exactly this shock.

|

|

The CIO View

"The data-centre party is over," warns a A$115bn CIO. UniSuper's chief investment officer John Pearce argues that investors rushing into digital infrastructure risk taking on hidden technology debt and misreading the regulatory signals — a rare contrarian note against the "insatiable" AI-demand consensus — via Investment Magazine. It rhymes with our own read: a book that is simultaneously long hyperscalers, data centres, utilities and grid may be one concentrated theme wearing four labels.

Texas Teachers' Jase Auby makes the mirror-image case — that community pushback on data centres could become an investor advantage — while defending continued fossil-fuel investment and explaining why the total-portfolio approach doesn't fit TRS's culture — via Top1000funds. Two respected CIOs, circling the same question long-horizon owners now have to answer: how much of the AI-infrastructure trade is real capacity, and how much is priced-in faith?

|

|

People & Mandates · the daily leadership check

Korea's Teachers' Pension (₩33tn / ~$21.9bn) has reportedly named Baek Joo-Hyun, former CIO of the Government Employees Pension Service, as its new chief investment officer — decided July 8, start date not yet set. Two smaller moves noted below top-story bar: Norfund's EVP appointment (Naana Winful Fynn) and Campbell Global's promotion of Michael Barbara. No C-suite change surfaced at a top-ten global fund in the window.

|

|

Pensions & Government

The UK sets the clock on its biggest pension consolidation in years. The DWP laid out its reform roadmap — Value-for-Money assessments from 2028 and a £25bn AUM scale threshold from April 2030 (or £10bn with a credible plan to reach £25bn by 2035). Scale is becoming a licence to operate. DWP timeline →

Japan cools the GPIF-reallocation story. Correcting earlier speculation, Japan has not decided to change GPIF's policy portfolio — one minister left the door open if conditions shift, another said current assumptions still hold. A Goldman analyst estimate suggests ~$80bn could migrate from foreign bonds to JGBs if it did. A reminder to separate a genuine mandate change from market chatter. Reuters/CNA →

|

|

Stewardship & the Environment

Development banks put a record number on climate finance. The multilateral development banks reported a record ~$163bn of climate finance in 2025, up 19% — the co-investment channel large owners increasingly partner into for resilience and transition assets. EIB joint MDB report →

India makes grid access forfeitable. Regulators moved to strip grid rights from ~15.7GW of idle renewable projects — turning scarce connectivity from a free reservation into forfeitable option value, and a live test of what a project is worth without a contracted route to market.

|

|

Global Capital & Private Markets

A cross-region private-credit template closes. Churchill Asset Management and Singapore's Seviora closed a ~$400m rated collateralised fund obligation pairing U.S. and Asian private credit — a packaging structure worth watching as the asset class institutionalises. Business Wire →

Bangladesh is negotiating a broad new framework with the IMF to replace its existing arrangement — size and conditions still under discussion, a marker for EM sovereign-risk watchers rather than a done deal. Separately, PIF and I Squared signed a non-binding MoU of up to $2bn in digital infrastructure and district cooling — sovereign capital using third-party operators to accelerate a pipeline.

|

|

Watch · The Next 72 Hours

A cluster of dated catalysts, any of which can confirm or break the lead:

Today, 8:30 ET — U.S. June CPI. The disinflation read the energy shock threatens.

Today, 4:00 ET — U.S. blockade enforcement begins. Are ships actually stopped? Transit counts and war-risk cover after this hour matter more than any speech.

Jul 15 — China Q2 GDP; BIS research on geopolitical risk and EM sovereign premia.

Jul 16 — Bank of Korea: first rate rise in more than three years expected — tightening into an energy shock.

Jul 17 — earliest return-to-service for New York's CHPE line; and the Treasury cutoff after which Iranian-oil sales are no longer authorised.

Also on the radar (dated background): Ukraine's cabinet reshuffle (PM Svyrydenko submitted her resignation after Zelensky proposed replacing her, Jul 12; no successor confirmed by parliament); Japan leaving the door open to a larger domestic role for GPIF; a PIF–I Squared MoU of up to $2bn in digital infrastructure; India moving to strip grid rights from ~15.7GW of idle renewables; and an IMO warning of renewed Black Sea / Sea of Azov attacks.

|

|

|

|

Today's scenario · The Chokepoint With a Price

The desk assigns ~55% probability (+13pp vs base) that Hormuz operates as an administered corridor through Q3 — with the toll contested and the repricing running through insurance, not the barrel.

|

|

Listen · The Universal Owner

Today's episode (~9 min): why the Hormuz story just changed category — and why the toll is paid through the insurance line, not the barrel. Plus Typhoon Bavi, CalPERS's 14.8%, and a 72-hour watchlist built around one hour: 4 p.m. ET. Sponsored by AssetOps Chicago, by Corinium.

|

|

Universal Asset Owners — Institutional Membership

For investment teams that need a continuous research relationship. Premium research, probability-weighted scenario analysis, weekly research calls, reasonable-use editorial Q&A and board-ready briefings for sovereign funds, pensions, endowments, family offices and institutional allocators.

|

|

|

The Back Page

with The Allocator

A lighter look at the institutional week, from the desk of a man who owns a slice of everything and is pitched by everyone.

The Allocator · "The Toll Booth" — cash, card, or a strongly-worded IMO statement?

Follow The Allocator — launching this week.

|

|

The proposed 20% Hormuz toll is labelled throughout as proposed, not operative — no collection mechanism has been published, and the IMO rejects any legal basis. Federal Reserve references reflect Kevin Warsh, chair since May 2026. Every figure in today's brief carries a named, dated source.

|

|