Private Capital • Family Governance • Asian Financial Centres

The scoreboard says Hong Kong is winning. The real contest is only beginning.

What the new rules mean for Asia's private-capital race — and how families, fund managers and policymakers should read a moment that is easier to announce than to bank.

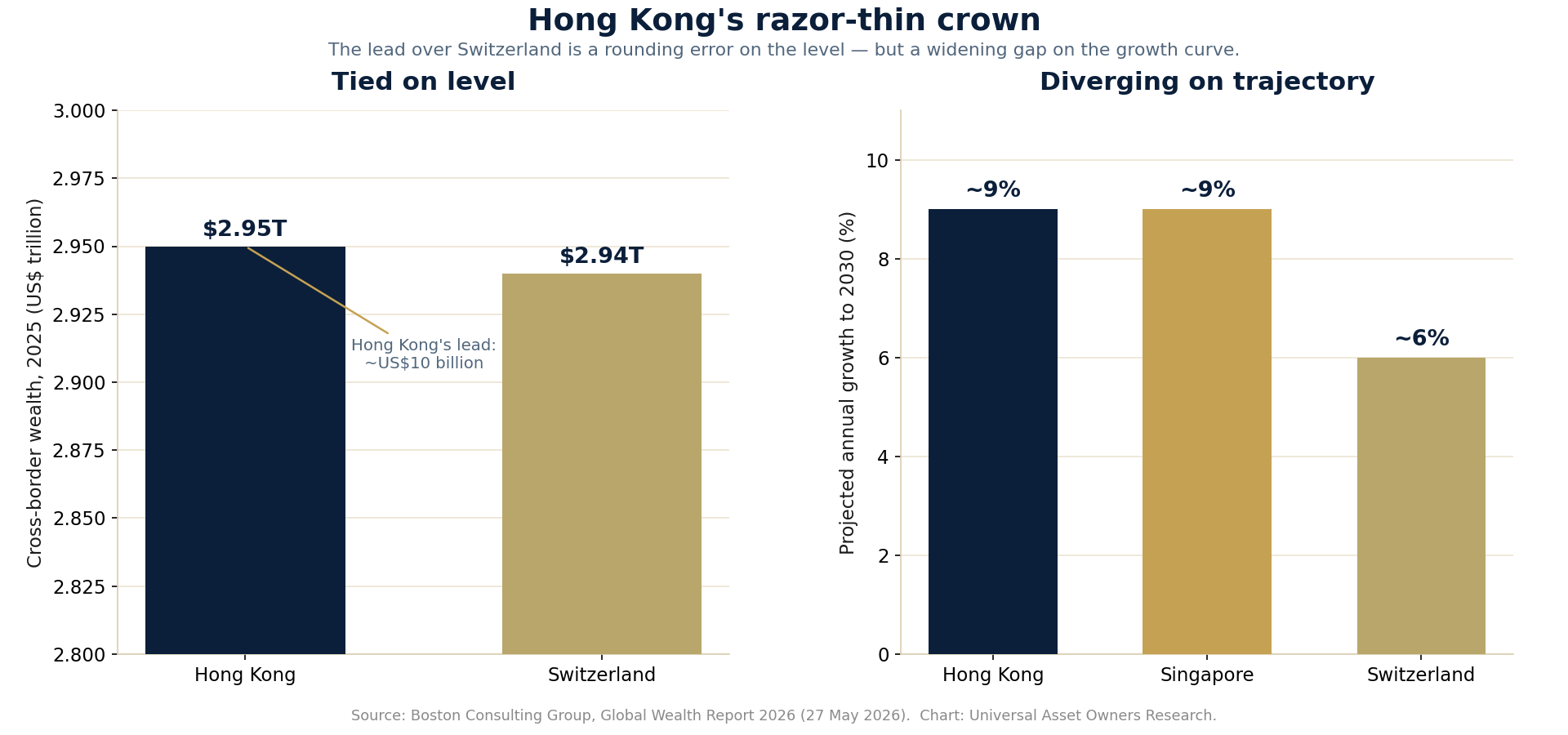

Hong Kong spent four years engineering a single sentence: the world's largest cross-border wealth hub. In May 2026 it finally earned the phrase. Boston Consulting Group's annual wealth report put Hong Kong's cross-border booked assets at roughly US$2.95 trillion, narrowly ahead of Switzerland's US$2.94 trillion — the first time the Swiss have been displaced from a franchise they had held since the phrase itself was coined. Six weeks later the city's Securities and Futures Commission reported that Hong Kong's entire asset- and wealth-management industry had reached HK$42.2 trillion, about US$5.38 trillion, a 20 percent jump powered by HK$2.1 trillion of net inflows — a figure that surged 193 percent on the prior year and marked a third consecutive annual increase.

Two records, arriving together, produced a triumphant headline and a slightly misleading one. The two numbers do not measure the same thing, the lead over Switzerland is thinner than a rounding convention, and the most consequential development of the season did not come from Hong Kong at all. It came from Singapore, which on 15 June quietly rewrote the rules of engagement.

This is not a story about which city is "ahead." It is a story about what the scoreboard actually counts, what it cannot count, and why the families and managers who read it literally will make expensive mistakes. Hong Kong's moment is real. Whether it becomes Hong Kong's era depends on a harder question than any league table can answer: can a booking centre convert assets it holds into decisions it makes?

Four numbers, four questions

Begin with discipline, because the public debate has abandoned it. At least four statistics now circulate as if interchangeable, and each answers a different question.

The first is cross-border wealth — assets that residents of one jurisdiction book in another. On this measure BCG has Hong Kong at US$2.95 trillion, up 10.7 percent in 2025, against a Swiss figure of US$2.94 trillion that grew 7.6 percent. The lead is about ten billion dollars on a base three thousand times larger; the two centres are, for practical purposes, tied on level. Hong Kong's claim rests not on scale but on trajectory. BCG projects both Hong Kong and Singapore compounding at roughly 9 percent a year through 2030, against about 6 percent for Switzerland — which is why the report frames the moment less as a Hong Kong victory than as a structural reordering. Global private wealth reached US$333 trillion in 2025, and BCG argues it is fracturing into two networks: a Hong Kong–Singapore axis serving Mainland Chinese, Indian and Southeast Asian capital, and a Switzerland–United States–United Kingdom axis serving European, Middle Eastern and Latin American money. Hong Kong did not simply overtake Switzerland. It won the larger share of a world that is splitting in two.

Hong Kong did not simply overtake Switzerland. It won the larger share of a world that is splitting in two.

The second number is total assets under management — the SFC's HK$42.2 trillion. This is a domestic industry gauge, not a cross-border one, and it includes asset management, fund advisory and private banking booked in Hong Kong regardless of origin. It is the right figure for the size of the financial-services economy and the wrong figure for the cross-border crown. Merging the two produces a bigger number and a weaker argument.

The third is the SFC's origin and destination data, and here two figures are routinely conflated. Investors domiciled outside Mainland China and Hong Kong supplied more than 54 percent of total AUM — evidence of genuine international reach. A separate 56 percent of assets were invested outside the Mainland and Hong Kong. The first speaks to where the money comes from; the second to where it goes. Neither, on its own, substantiates the more romantic claim that Middle Eastern and European family fortunes are relocating to Hong Kong at pace. The origin share is a stock, not a flow, and the cited releases contain no time series to prove acceleration. It is a strong fact that does not need embellishment to do its work.

The fourth number is the one everyone quotes: 3,384 single-family offices. Deloitte and InvestHK put that figure on Hong Kong at the end of 2025, 681 more than two years earlier — growth of better than a quarter. It is the headline of the season, and it is not a census. Hong Kong keeps no single-family-office registry, so the number is modelled: Deloitte estimates the city's population of wealthy individuals, applies the observed probability that families above given wealth tiers establish an office, and extrapolates, corroborating the result with surveys and interviews. Deloitte says so plainly, flagging sample bias and the assumption that formation rates hold across places and times. The underlying primary research surveyed 136 market participants — 121 family offices, of which 85 were single-family and 36 multi-family, plus banks and service providers — with 21 interviews, collected between October and December 2025 through professional networks. It is an informed estimate and a useful signal. It is not a roster, and it cannot bear the weight of a precise side-by-side ranking.

The first rule of this market, then, is unglamorous: name the unit, the perimeter, the source and the date every time a number is used. Do that, and Hong Kong's position looks strong and specific rather than vast and vague — which is the more durable form of leadership.

Why the momentum is real

Discipline about the numbers is not skepticism about the substance. Hong Kong's advantage is not a single tax rule; it is a stack that is genuinely hard to replicate.

The city offers deep and liquid equity and bond markets, a banking sector that includes more than 70 of the world's 100 largest banks — the government prefers "nearly 80" — layered over 150-plus licensed banks, the world's largest pool of offshore renminbi, direct connectivity to Mainland markets through the Connect schemes, a territorial tax system that does not reach foreign-sourced income, a capital-linked residency route, and an increasingly complete professional-services ecosystem of lawyers, auditors, trustees and administrators. No competitor combines Mainland proximity with international market infrastructure in quite the same way.

That stack was assembled deliberately. The 2023 Policy Statement on Developing Family Office Businesses launched eight measures at once: a zero-percent profits-tax concession for qualifying family-owned investment holding vehicles, a dedicated InvestHK service network, a new investment-migration route, an art-and-philanthropy push, and a market-entry design that skips regulator pre-approval. The 2024–25 budget cycle promised to widen the list of qualifying assets to include digital assets, private credit and precious metals. In 2025 the government hit its target of attracting 200 family offices ahead of schedule, and the Chief Executive's Policy Address set a fresh goal of helping more than 220 offices establish or expand between 2026 and 2028.

The economic footprint is now measurable rather than aspirational. Deloitte estimates that Hong Kong's single-family offices directly employ more than 10,000 professionals and contribute about HK$12.6 billion a year to the local economy through operating expenditure alone. Sentiment points the same way: 74 percent of surveyed single-family offices and 94 percent of multi-family offices planned to expand; 60 percent of single-family respondents intended to increase their Hong Kong position over three years and 40 percent to maintain it, with none planning a reduction. These are survey estimates from a non-random sample, and should be read as direction rather than measurement — but the direction is unambiguous.

The most important line in the Deloitte study is also its most demanding. Anthony Lau, its lead partner, observed that the ecosystem has evolved "beyond simply increasing the number of family offices." That is precisely the right test. The policy question is no longer how many entities Hong Kong can attract, but whether it can integrate family capital, operating companies and the next generation into a long-term local economy. Formation is the easy part.

The dependency inside the franchise

Every franchise has a concentration, and Hong Kong's is Mainland China. BCG estimates that Mainland flows represent more than 60 percent of the city's cross-border assets. This is the core of the business, not a flaw in it — but it changes the risk model, because it means Hong Kong's booking-centre growth is partly a policy variable set in Beijing.

The point stopped being theoretical this year. In late May, Chinese regulators penalised three online brokers — Futu, Tiger and Longbridge — for onboarding Mainland clients without onshore licences. All three halted new positions and fund transfers from Mainland investors on 12 June. Reuters reported that the clampdown had unsettled Hong Kong's banks and insurers, whose Mainland business had become central: Mainland deposits in Hong Kong have risen roughly 50 percent since 2023 to around US$237 billion, and the value of new insurance business written for Mainland visitors at AIA's Hong Kong unit grew 35 percent in 2025, approaching half of the unit's new business. Analysts at J.P. Morgan raised the prospect that scrutiny could widen to the overseas income of Mainland residents.

The same Mainland flows that lifted Hong Kong past Switzerland are the flows now being tightened.

Here is the uncomfortable symmetry: the same Mainland flows that lifted Hong Kong past Switzerland are the flows now being tightened. A booking centre that grows because capital wants a familiar, discreet offshore base is exposed to any change in how tolerantly that capital is allowed to travel. Diversifying beyond Mainland money is therefore not a marketing slogan for Hong Kong; it is a resilience requirement. The 54-percent non-Mainland origin figure is the beginning of that diversification, not proof it is complete.

The June bill: commercially important, legally unfinished

The centrepiece of Hong Kong's 2026 pitch is a tax bill — and it is essential to be precise about its status, because the marketing has run ahead of the legislature.

The Inland Revenue (Amendment) (Preferential Tax Regimes for Funds, Family-owned Investment Holding Vehicles and Carried Interest) Bill 2026 was gazetted on 12 June and received its first reading, with the second-reading debate commenced, on 24 June. It has since been referred to committee scrutiny. As of mid-July it had not been enacted. Subject to enactment, its enhanced provisions for family-owned investment holding vehicles are intended to apply retrospectively from the 2025/26 year of assessment. The Inland Revenue Department has offered a pragmatic bridge: eligible taxpayers may file their 2025/26 returns on the proposed basis while the bill proceeds, with the understanding that returns may need revision if the enacted law differs. That is administrative accommodation, not legislative certainty, and advisers should treat the distinction as material.

What the bill would change is substantive. It broadens the Schedule 16C list of qualifying assets to include digital assets, loans and private credit, immovable property situated outside Hong Kong, insurance-linked securities, certain commodity derivatives, emissions allowances and carbon credits, and precious metals — the last with an important nuance that the shorthand usually omits. The oft-repeated claim that "physical gold now qualifies up to 20 percent of the portfolio" is not quite right. The 20-percent cap applies to precious metals other than gold or silver traded on the Hong Kong Gold Exchange; Exchange-traded gold and silver are not subject to that limit, while a separate cap of around 15 percent governs specified commodities. The distinction matters for portfolio construction, and it dovetails with a piece of physical-market infrastructure that arrived on 7 July, when Hong Kong's new gold central clearing and settlement system began trial operation — a reminder that the city is building the plumbing behind the tax perimeter, not merely the perimeter.

The bill also fixes a genuine irritant in how the HK$240 million asset threshold is measured. The old test turned on an undefined notion of net asset value, under which a shareholder loan was subtracted before checking whether a vehicle qualified. Consider a vehicle holding HK$300 million of Schedule 16C assets, funded with HK$100 million of debt. Under the reworked "value of assets" test, the treatment depends on the lender. A loan from a holder of direct beneficial interest — a participating family member — is no longer deducted, so the vehicle clears the threshold on its HK$300 million of assets. A bank or unrelated third-party loan continues to be deducted. The rule makes ordinary family capitalisation workable while blocking leverage manufactured solely to cross the line. A companion limb extends favourable treatment to eligible carried interest, and the bill broadens the definition of "fund" to reach pension funds, charitable endowments and single-investor sovereign and central-bank vehicles — a detail that should interest the largest institutional owners, not only families.

The deeper design choice is Hong Kong's reliance on self-assessment. Because the concession is claimed by election in the annual return rather than granted by a regulator, set-up friction is low. But self-assessment does not eliminate risk; it relocates it. The burden of getting classification, valuation, substance and anti-avoidance right sits with the family and its advisers, to be tested only if the Department later inquires. Fast to establish is not the same as safe to defend. An optional advance-ruling route exists for families that want certainty on a difficult structure, and more will need it than the marketing implies.

Singapore has already answered

The tempting story is that Hong Kong's speed has left Singapore flat-footed and pre-clearance-bound. That story is now out of date.

On 15 June, the Monetary Authority of Singapore replaced its case-by-case licensing exemptions with a single, structure-agnostic class exemption for qualifying single-family offices from licensing under the Securities and Futures Act. The change is more consequential than it sounds, because it removes exactly the bottleneck critics used to cite. A qualifying office no longer applies for a bespoke exemption; it simply notifies MAS. A new office files a commencement notice within 14 days of starting operations; existing offices have until 15 June 2027 to comply. The office must be Singapore-incorporated, maintain a qualifying bank account, designate a Singapore-resident employee as contact, and serve a defined family — lineal descendants of a common ancestor across up to five generations, plus spouses and related beneficiaries — with non-family key employees permitted a non-controlling stake of up to 10 percent. The initial filing is a notification accompanied by a signed declaration, not an approval application, and it requires no legal opinion. Thereafter the office files an annual return within four months of its financial year-end, with no extensions expected.

Singapore, in other words, has not merely sped up. It has changed the nature of the exchange: bespoke pre-clearance traded for codified eligibility, bank-mediated diligence and continuing regulatory visibility. Ocorian frames the objective as stronger "regulatory visibility and accountability." The move is philosophically the opposite of Hong Kong's — Singapore is codifying the licensing perimeter while Hong Kong broadens the tax perimeter — but its practical effect is to erase the single clearest advantage Hong Kong's promoters had claimed.

Crucially, the new class exemption does not touch Singapore's tax incentives, which remain approval-based. Sections 13O and 13U of the Income Tax Act, administered by MAS alongside the tax authority, continue to require a minimum of S$20 million and S$50 million respectively in designated investments, along with conditions on investment professionals, local spending and capital deployment. So the correct way to read the contest is not "approval versus no approval." It is a three-layer comparison. Establishment — incorporating the vehicle — is straightforward in both cities. Licensing is now notification-based in Singapore and generally not required for a Hong Kong single-family office operating within the intra-group carve-out. Tax is self-assessed in Hong Kong and approval-based in Singapore. Collapse those three layers into one process and every comparison that follows is wrong.

The office-count contrast makes the point vividly. Hong Kong's 3,384 is a modelled estimate of all single-family offices at the end of 2025. Singapore's "over 2,000" is the number of offices awarded tax incentives as of the end of 2024 — a firm administrative count, of a different thing, from a different year. One is broader but inferred; the other is narrower but exact. A chart that sets them side by side without that footnote is numerically tidy and analytically false.

Which framework is superior? Neither, in the abstract. Hong Kong reduces front-end friction and places more proof burden on the taxpayer; Singapore makes the licensing route clearer while retaining tax approval and recurring reporting. The right choice depends on the family's assets, structure, risk tolerance and appetite for disclosure — not on a universal ranking that does not exist.

What the evidence actually says about family capital

A durable piece of marketing folklore holds that Hong Kong money is cautious and Singapore money is adventurous — that portfolios can be read off a postcode. The evidence is thinner than the story.

The strongest Hong Kong-specific data show that public equities remain the core allocation and private equity leads the alternatives, with rising interest in digital assets and a thematic tilt toward technology and media, healthcare and artificial intelligence, alongside renewed Hong Kong and Mainland exposure and some retreat from the United States. UBS's Global Family Office Report 2026 — its most authoritative regional read, drawn from 307 offices across more than 30 markets, surveyed between late January and late March, representing families worth an average US$2.7 billion and offices running an average US$1.3 billion — offers a broader signal. In its current strategic allocations, North Asia offices held 68 percent in traditional asset classes, 18 percent in cash and 9 percent in private equity, while Southeast Asia offices held 62 percent traditional, 14 percent cash and 20 percent private equity. That is directionally consistent with the folklore. But UBS flags the Southeast Asia sample as low-base, and neither region maps onto Hong Kong or Singapore domicile. Regional allocation is not the same as domicile behaviour, and a plausible pattern is not a proven cause. Segment the allocator — the family's mandate, liquidity and governance — not the postcode.

The more arresting findings in the 2026 reports are not regional at all; they are about a global reappraisal of risk. UBS records that 60 percent of family offices plan to change their strategic asset allocation in the coming year — the highest share it has ever measured — and that 65 percent expect confidence in the US dollar's reserve status to weaken, with plans emerging to trim dollar exposure in favour of the euro, the Swiss franc and gold. Real estate allocations are being cut from 11 to 8 percent, infrastructure doubled off a low base from 1 to 2 percent, and hedge-fund weightings lifted. For universal owners watching the same de-dollarisation debate, this is the family-office channel of a much larger conversation.

And there is a conviction-implementation gap that should temper any thematic exuberance. J.P. Morgan's 2026 survey of 333 offices — average family net worth US$1.6 billion — found 65 percent prioritising artificial intelligence as a theme, yet 79 percent holding no infrastructure allocation at all and 57 percent with no exposure to growth or venture capital. Families are convinced of the AI story and largely unbuilt to express it, because the compute, power and physical infrastructure that AI runs on sit in asset classes their portfolios do not yet touch. The lesson for anyone raising capital from this audience is that thematic agreement is cheap and portfolio architecture is scarce.

Governance is the scarce asset

Strip away the tax rates and the league tables and the strongest reason to build a family office remains unglamorous: to create an institution capable of making decisions across generations. On that measure the industry is underbuilt, and the data are sobering.

UBS found that among its 307 offices — sophisticated, well-advised, averaging US$1.3 billion in assets — only 49 percent had a governance framework, 41 percent had cybersecurity controls, 35 percent had a succession plan for the office itself, and just 27 percent ran an organised process to prepare the next generation. These are not fringe operators; they are the market's core, and roughly half of it lacks the basic institutional scaffolding.

This governance deficit is not a soft concern adjacent to Hong Kong's policy success. It is central to it. A hub that attracts entities faster than families professionalise accumulates operational, reputational and succession risk on its own balance sheet of reputation. Tax and residency incentives are worth most when they function as entry points to better institutions and least when they substitute for them. The scoreboard rewards formation; the risk register is written in governance.

The scoreboard rewards formation; the risk register is written in governance.

Families themselves increasingly ask for more than returns. The Hong Kong Institute for Monetary and Financial Research, the research arm of the city's Academy of Finance, surveyed 101 respondents with 35 in-depth interviews for its March 2026 study, Beyond Wealth. It found that 91 percent were already invested in Hong Kong, and projected participation in philanthropy rising from 45 to 64 percent and in impact investing from 30 to 43 percent, alongside growing demand for risk-management services. These are expectations rather than committed flows, but they describe a service model migrating beyond portfolio management toward stewardship — the ground on which the next phase of competition will actually be fought.

The winning structure may have more than one city

For a sophisticated family, "Hong Kong or Singapore?" is often the wrong opening question. It presumes a single jurisdiction must house every function, when in practice a family can place its principal residence, its investment committee, its holding vehicle, its funds, its banking, its operating company, its philanthropy and its backup administration in different places. The task is not to pick a city; it is to assign functions, and then to choose the jurisdictions that fit them.

A dual-hub architecture — Hong Kong for Mainland access and renminbi capability, Singapore for Southeast Asian reach and codified stability — can be genuinely resilient. It can also be theatre. Its defensibility comes entirely from real functions, real people and real decisions. A second hub that exists only on an organisation chart adds cost and audit exposure without adding resilience, and it invites precisely the substance challenge that both tax authorities are learning to press. The discipline is to match decision rights, tax residence, banking relationships and reporting to economic reality — and to remember that complexity is not the same as sophistication. If the structure cannot survive a regulator asking where the decisions are actually made, it is a liability wearing the costume of an asset.

What each stakeholder should do now

For principals and chief investment officers. Draw six separate maps — of people, ownership, control, assets, decision-making and banking — on a single page each. Most tax, regulatory and governance failures live in the gaps between them. Run a pre-mortem on any Hong Kong, Singapore or dual-hub plan by assuming it has failed in three years, and test the causes: a bank exit, an adverse tax interpretation, the loss of a key person, tightening capital controls, a family dispute, a cyber fraud. Model the portfolio against the actual eligible-asset perimeter rather than inferring eligibility from asset-class labels. Approve governance — an investment-committee charter, reserved matters, a conflicts policy, a delegation matrix, emergency authority and a next-generation plan — before the first trade, not after the first dispute. And treat privacy as controlled confidentiality: minimise unnecessary disclosure, but keep a complete, current, bank-ready file, because privacy without documented provenance is fragility, not protection.

For private-equity, venture, private-credit and hedge-fund managers. Build separate Hong Kong and Singapore coverage theses, but do not assume domicile determines risk appetite or ticket size. Ask, early, whether the family can actually commit through the proposed vehicle and whether income, leverage, digital assets or co-investment create tax or perimeter problems. Offer institutional transparency — portfolio look-through, valuation policy, liquidity and commitment pacing, side-letter governance, cybersecurity and sanctions controls — as a matter of course. Engage the next generation and the operating company without letting educational access curdle into conflicted deal allocation. And measure the funnel from first meeting to funded capital: entity announcements are top-of-funnel intelligence, not results.

For banks, lawyers, tax advisers and administrators. Produce one integrated eligibility opinion spanning licensing, tax, beneficial ownership, assets, financing, substance and reporting, rather than siloed memos that leave gaps between disciplines. Maintain a legislative-change protocol for Hong Kong's pending bill and a transition plan for Singapore's 15 June 2027 deadline. Sell the recurring capabilities families actually lack — independent valuation, consolidated reporting, payment and cyber controls, succession operations — not only formation and tax work. And say so plainly when a second hub has no real people, mandate or decisions behind it.

For Hong Kong's policymakers. Publish the office-count methodology and its confidence range consistently, distinguishing modelled offices, assisted cases, tax-concession users and locally substantive operations. Report conversion outcomes — senior jobs, payroll, operating spend, local mandates, capital deployed, next-generation programmes, philanthropy — because those, not entity tallies, are the real measure of success. After enactment, issue asset-by-asset guidance on valuation, digital assets, private credit, shareholder loans and foreign property. Preserve the speed of self-assessment while opening optional advance-ruling or anonymised-precedent channels for hard structures. And treat diversification beyond Mainland capital as a resilience priority, not a promotional line.

Twenty-four-month scenarios

The probabilities below are Universal Asset Owners' analytical judgments for the period to 13 July 2028. They are not statistical estimates or market-implied odds; they are a disciplined way to hold competing possibilities in view, and they should be revised as the signals beneath them move.

Durable Hong Kong lead — 35 percent. The bill is enacted substantially intact, Inland Revenue guidance resolves the valuation and loan questions cleanly, inflows stay broad-based rather than narrowly Mainland, and diversification of origin continues. Hong Kong converts its booking crown into local substance.

Two-hub equilibrium — 30 percent. Singapore's notification regime materially shortens set-up while its 13O and 13U approvals keep flowing, and Hong Kong's family-vehicle claims keep rising. The two cities specialise rather than one dominating, and sophisticated families run both. This is the modal outcome.

Shallow substance — 20 percent. Formation continues but official reporting cannot show senior jobs, locally made decisions, recurring spend or genuine concession use behind the entity count. Hong Kong holds the headline and loses the argument about permanence.

Policy or market setback — 15 percent. Mainland enforcement widens toward ordinary compliant channels, major custodians tighten risk appetite, or the tax bill is materially delayed or narrowed. The concentration risk inside the franchise expresses itself, and growth stalls.

Raise the durable-lead case on clean enactment, resolved guidance and broad inflows; raise the two-hub case if Singapore's regime cuts set-up time while both cities' approvals grow; raise the shallow-substance case if reporting emphasises counts over conversion; raise the setback case if enforcement widens, custodians retrench or the bill stalls.

Twelve signals worth watching

Track these, in roughly this order of importance: the enactment date and final scope of Hong Kong's bill; the substance of Inland Revenue guidance on valuation, digital assets and shareholder loans; the breadth of 2026 inflows by investor origin; the pace of Singapore commencement notices ahead of June 2027; 13O and 13U approval volumes; any widening of Mainland enforcement beyond unlicensed brokers; custodian and private-bank risk appetite for family-office onboarding; senior-hiring and payroll data from official reporting; next-generation and philanthropy programme launches; digital-asset and private-credit adoption under the new perimeter; the health of offshore-renminbi and Connect flows; and the trajectory of non-Mainland origin as a share of assets. The first two are process questions Hong Kong controls. The last is the one that decides whether it becomes a global hub or remains a very efficient regional one.

A jurisdiction scorecard

For families weighing the decision, a weighted scorecard is less useful for the ranking it produces than for the argument it forces. Score each candidate jurisdiction from one to five on the dimensions that matter — market access and infrastructure; tax treatment of the actual portfolio; licensing and reporting burden; banking and onboarding reality; substance and talent availability; succession and governance support; privacy and disclosure fit; and geopolitical and concentration risk — weight them to the family's priorities, and the exercise will surface disagreements about red lines before advisers optimise a structure around unstated assumptions.

Five of those red lines are non-negotiable, and each is a reason to stop rather than proceed. Stop if there is no bankable source-of-wealth file, because a structure that cannot pass institutional onboarding is not operational. Stop if the family has no agreement on control and succession, because formation will only harden conflict into legal structure. Stop if the tax thesis depends on labels rather than assets and activity, because "family office" is not itself an exemption. Stop if there are no real local decision-makers, because the arrangement may fail tax, governance and resilience objectives at once. And stop if there is no integrated view of the family enterprise alongside the portfolio, because concentration and liquidity risk cannot be managed from half a balance sheet.

The first ninety days, done well, are unglamorous: assemble the six maps and the source-of-wealth file; take independent tax and licensing advice structured as a single integrated opinion; adopt the governance documents; model the portfolio against the real eligible-asset perimeter; and only then incorporate. Formation should be the consequence of the decisions, not a substitute for making them.

The moment is a test of conversion

Hong Kong has earned its headline. It has a credible claim to global leadership in cross-border wealth booking, a record domestic industry, a large and growing family-office population, financial infrastructure that few cities can match, and a tax bill built for the way modern private capital actually invests. Those advantages are substantive, and the moment is genuinely important.

But the contest has changed shape. Singapore has removed the licensing uncertainty that once defined the comparison while formalising notification and annual oversight; Hong Kong is using self-assessment and a broader tax perimeter to maximise flexibility. The two cities are not converging on one model. They are becoming more clearly different, and the sophisticated answer increasingly involves both.

The families who benefit will not be the ones who chase the newest concession. They will be the ones who make the legal structure match where people live, where decisions are made, where banks will transact, what assets are held, and how the institution survives its founder. The providers who win will sell governance, data and execution rather than a place in a ranking. And the policymakers who win will report conversion and permanence rather than counting entities. Hong Kong's moment is real. Its era will be decided by how much of what it now holds it can teach itself to actually do.

Methodology and source notes

This analysis draws on public information available through 13 July 2026, giving priority to regulators, legislation, government releases and full research reports, supplemented by Reuters reporting and specialist legal analysis. The cutoff matters: Hong Kong's bill remains under scrutiny and Singapore's revised framework took effect only on 15 June. Statements attached to a named source rest on that source; statements without one are analytical interpretation or explicit Universal Asset Owners judgment. Cross-border wealth, total assets under management, modelled single-family-office estimates and tax-incentivised office counts are treated as distinct measures and are not combined. The 24-month probabilities sum to 100 percent but are analytical judgments, not the output of a statistical model, and should be revised as the listed signals change. Short quotations are used for analysis and commentary. Qualified legal, tax, regulatory, immigration and investment advice is required before any action.

Selected sources. Boston Consulting Group, Global Wealth Report 2026 and press release, "Hong Kong Surpasses Switzerland as the World's Largest Cross-Border Wealth Hub" (27 May 2026). Hong Kong Securities and Futures Commission, 2025 Survey on Asset and Wealth Management (2 July 2026); Reuters, "Hong Kong's assets under management grow to record $5.38 trillion" (2 July 2026). Deloitte China and InvestHK, Market Study on the Family Office Landscape in Hong Kong (10 February 2026); HKSAR Government, "Hong Kong's single-family offices total surpasses 3,380" (10 February 2026). HKSAR Government, Policy Statement on Developing Family Office Businesses in Hong Kong (24 March 2023). Inland Revenue (Amendment) (Preferential Tax Regimes for Funds, Family-owned Investment Holding Vehicles and Carried Interest) Bill 2026, gazetted 12 June 2026; Legislative Council bill and brief; Inland Revenue Department transitional measure (12 June 2026); KPMG China, "Hong Kong SAR unveils draft law to make its family office tax regime more attractive" (12 June 2026); Sidley Austin (26 June 2026). Monetary Authority of Singapore, "Revised Framework for Single Family Offices to take effect on 15 June 2026" and FAQs; Baker McKenzie (18 June 2026); Ocorian (30 June and 7 July 2026); MAS, Fund Tax Incentive Scheme for Family Offices. Reuters, "Beijing's investment clampdown clouds outlook for Hong Kong banks, insurers" (11 June 2026). UBS, Global Family Office Report 2026 (28 May 2026). J.P. Morgan Private Bank, 2026 Global Family Office Report (28 January 2026). Hong Kong Institute for Monetary and Financial Research / HKMA, Beyond Wealth: Advancing Hong Kong's Family Office Ecosystem (10 March 2026). New Capital Investment Entrant Scheme enhancements (1 March 2026); HKSAR Government, gold central clearing system trial (7 July 2026).

Universal Asset Owners Research. Prepared for institutional discussion. Not investment, legal, tax or regulatory advice. © 2026.