|

Universal Asset Owners

The UAO Daily Brief

Volume 1, Issue 57 • Friday, July 10, 2026 • 7:00 am ET / 15:00 GST

|

Watch — today's video briefing  |

|

Japan Bets on Itself. Temasek Goes Maximum AI.

Tokyo is testing whether pension capital can serve the national balance sheet. Temasek is making one of the largest institutional AI bets yet—while keeping a quarter of its portfolio liquid.

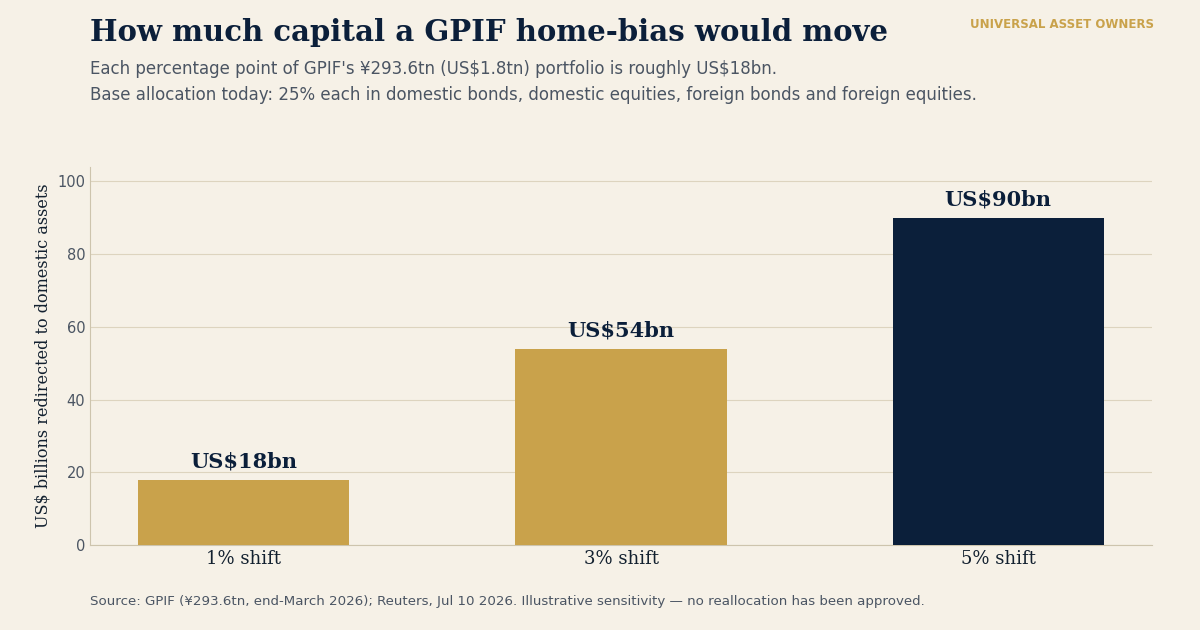

The world's largest pension fund has not changed its portfolio — and that is precisely why Japan's latest signal matters. On Friday, Finance Minister Satsuki Katayama said Tokyo wants pension funds, including the ¥293.6tn (US$1.8tn) GPIF, to make “substantially” greater investments in Japanese financial assets. No target or allocation change was announced, and GPIF restated its long-term risk mandate — yet the yen firmed and Japanese government bonds rallied on the mere possibility that retirement capital could be called home.

Set beside the week's other institutional signals, the message runs wider than Japan. Temasek posted a record S$518bn and set out to lift AI toward 15% of its book — while ring-fencing about a quarter of the portfolio in liquid assets to weather shocks. CPP Investments put US$1.75bn behind the AI grid. New IE University data show sovereign funds writing fewer but far larger strategic cheques. And reserve managers, OMFIF finds, are quietly trimming the dollar and buying gold. Governments and their largest pools are being asked to carry more of the national balance sheet and to finance the AI build-out at scale — even as the physical, liquidity and transparency limits on that build-out come into view. The state is testing the boundaries of the mandate; the systems needed to execute it are lagging. |

|

Listen — The Universal Owner daily briefing

Today's episode: how one ministerial sentence in Tokyo reopened the oldest question in pension governance — whom does the portfolio serve? — and why the smartest state investor is holding a quarter of its book in liquid assets.

|

|

|

Three links

• Japan urges GPIF and pension funds to invest more at home; yen and JGBs rally — The Japan Times / Reuters

• Temasek's net portfolio value grows to S$518bn; AI target lifted toward 15% — Temasek

• For the first time since 2023, more central banks plan to cut dollar holdings than add — OMFIF Global Public Investor 2026 |

|

Today's Intelligence — Top Stories

1. When the pension fund becomes policy.

Japan's finance minister said on July 10 that the government wants pension funds, including GPIF, to make substantially greater investments in Japanese financial assets, alongside plans to expand JGB products for households. GPIF managed ¥293.6tn — about US$1.8tn — at end-March and holds roughly equal strategic weights across domestic bonds, domestic equities, foreign bonds and foreign equities; about half its book sits in foreign assets. Crucially, this is a government objective, not a decided allocation: no target, timetable or mandate change has been approved, and GPIF said its portfolio remains designed to meet its long-term objective with the minimum necessary risk. Markets moved anyway — the yen firmed about 0.6% and 10-year JGB yields fell 11.5 basis points to 2.760%. Japan Times / Reuters, Jul 10.

Implication for owners. The issue is governance before flow. A one-percentage-point shift is roughly US$18bn; a 3–5% move is US$54–90bn (see today's chart). A larger reweighting could support the yen and JGBs while trimming foreign-asset demand — but it blurs the line between beneficiary-first investing and national balance-sheet management. The less obvious risk is not “Japan buys Japan.” It is whether home-bias becomes a quasi-fiscal tool: once a pension reserve is expected to stabilise a currency or a bond market, the portfolio acquires an implicit policy obligation not captured in its strategic asset allocation. Japan's cabinet is expected to approve its final economic blueprint (the “Honebuto” framework) on July 21 — the next hard date to watch.

2. Temasek's barbell: maximum AI, maximum liquidity.

Temasek reported a record mark-to-market net portfolio value of S$518bn (about US$400bn) at end-March, up S$49bn, with a one-year total shareholder return of 10.5%. Management said it will raise AI-related exposure from about 6% to up to 15% by 2031, investing across energy and data centres, semiconductors, cloud, foundation models and software — while adding, tellingly, that most of the value will be captured in the other 85%. Temasek, Jul 8. Its CIO said Temasek keeps about a quarter of the portfolio (~US$100bn) liquid to weather shocks and pivot with trends — and that well over 60% of its current AI exposure is itself liquid. The Star, Jul 9.

Implication for owners. The headline is “AI bet”; the signal is the barbell. The most admired state investor is expressing maximum thematic conviction and maximum optionality at the same time — a portfolio-construction statement about tail risk in the AI trade, and a hedge against exactly the power, valuation and liquidity constraints surfacing elsewhere in this issue. Note the caveats: a 15% weight by 2031 is a target, not deployed capital, and a 25% liquidity band is stated policy, not a same-day change. For funds with long-duration liabilities, the second signal — conviction funded without surrendering liquidity — may be the more instructive of the two.

3. A pension underwrites the AI grid.

CPP Investments said on July 3 it will invest US$1.75bn (C$2.4bn) to support EQT's AI-infrastructure strategy, led by data-centre developer EdgeConneX, whose pipeline exceeds 10 GW across 20-plus countries; the transaction has closed. DCD, Jul 3. This is retirement capital moving upstream from listed equity into the ownership and financing of AI's physical layer.

Implication for owners. The market reads this as a growth allocation; the under-appreciated risk is deliverability. A 10 GW pipeline is an interconnection-and-power problem before it is a returns problem (see story 5). And there is a concentration trap: if pensions increasingly own the equity of data-centre platforms and the private credit that finances them and the utilities that power them, correlation rises inside a single “diversified” book. Distinguish committed from deployed, and pipeline from operational capacity.

4. Hormuz's reopening has stalled again.

Observed tanker traffic through the Strait of Hormuz fell back toward near standstill after renewed US–Iran fighting. Per Lloyd's List Intelligence, no vessel above 10,000 dwt has transited the US-coordinated route with its transponder on since Tuesday; Windward tracked only five crossings on Wednesday and early Thursday, versus 45 on Monday and roughly 130 a day before the war. Several ships are believed to have crossed “AIS-dark.” Al Jazeera, Jul 10. Because AIS darkness obscures true volumes, the collapse in observed transits is a firmer fact than any single flow estimate. Brent, tellingly, held near US$76 — roughly flat on the day.

Implication for owners. The exposure is far broader than oil: LNG, refined products, marine insurance, freight, fertiliser, Gulf fiscal balances and inflation expectations all run through the same narrow waterway, and a universal owner cannot diversify away from a chokepoint that hits both assets and liabilities. Brent is an incomplete dashboard. The economically relevant price may be the reliability discount repricing through insurance terms, charter rates, inventories and working capital — a slow tax on trade that persists even when spot crude normalises.

5. The AI bottleneck is physical — transformers and the grid.

Two data points from the same week make the constraint concrete. US utilities are securing transformers and grid equipment years in advance: generator step-up transformer lead times now exceed 160 weeks (versus ~143 in 2024), with some units quoted as far out as four years and prices set to rise a further 4–10%. Reuters / Wood Mackenzie, via Data Center Knowledge. And on July 2–3, PJM — the largest US grid operator — ran Maximum Generation and Load Management alerts through a heat dome: PJM recorded about 162.7 GW of actual peak load on July 2 after emergency demand-response measures, with a preliminary ~168 GW unrestricted-demand estimate — above the previous record. Two US Department of Energy emergency orders allowed PJM to call on backup generation at data centres and other large-load facilities, and to temporarily operate specified plants beyond certain normal permit constraints. PJM, Jul 3. Utility Dive.

Implication for owners. The AI build-out is turning from a financing problem into a delivery problem, and the scarce asset is shifting from a generic site to an energised site with secured equipment, permits and interconnection. The PJM orders carry a sharper message for underwriters: if large loads can be ordered onto backup generation in emergencies, the firm-power certainty behind data-centre project finance is weaker than headline demand implies. Grid access — not chips, not capital — is becoming the binding constraint, and it should be priced as an ownable scarcity.

6. Private credit: opacity meets a deployment slowdown.

Two pressures are converging on the same asset class. European supervisors seeking borrower, valuation and guarantee data on US-centred private-credit structures have met resistance from US authorities; ECB analysis cited in the reporting puts euro-area bank exposure near €62.5bn, insurers ~€211bn and pension funds ~€52bn, but officials fear these direct figures miss layered transmission through fund finance, CLOs, leveraged lending and asset-intensive reinsurance. ECB FSR. At the same time, US direct-lending volume fell 55% quarter over quarter to US$33.59bn in Q2 even as fundraising rebounded — North America-focused closed-end direct-lending funds raised US$16.25bn in the quarter, the most in two years, into a slowing deployment environment. Reuters, Jul 9.

Implication for owners. Allocators may be managing exposure manager-by-manager while regulators cannot reconstruct the ultimate borrower and collateral risk. The first cost of opacity could arrive before any credit losses: if data-sharing does not improve, supervisors may respond with higher capital charges, liquidity buffers or valuation haircuts — none of it announced policy, but the direction of the pressure. Meanwhile a widening raised-versus-deployed gap pushes managers either to sit on non-earning commitments (return drag) or to loosen terms to deploy (quality erosion). Both are adverse for a long-horizon LP, and both are hard to see because private marks lag.

7. Sovereign funds are becoming strategic ministries with portfolios.

A new IE University study tracked 391 direct sovereign-fund investments over the 18 months to December 2025. Deal count fell 17%, but tracked spending rose 91% to US$404bn; AI represented roughly one-third, the United States attracted US$220.4bn, Temasek led on deal count (71), and the report identified 12 new sovereign or state-backed vehicles. IE University. (The data cover disclosed direct deals only and may be dominated by a few mega-transactions; the full methodology still merits review.)

Implication for owners. The marginal sovereign investor is increasingly pursuing access, resilience and strategic positioning alongside return — a different counterparty in AI, semiconductors, infrastructure and critical supply chains. Strategic capital may sustain valuations through volatility, but it can also change direction abruptly when national priorities or fiscal conditions shift. Read with Japan's pension message and Temasek's barbell, it is one story: large pools of long-horizon capital are being asked to carry more national-policy weight.

|

|

What an owner should test this week

| Pension governance — document where beneficiary-first objectives would conflict with a home-bias or strategic-industry mandate before one is placed on you. |

| The barbell test — if the most admired state investor holds ~25% liquid while chasing AI, re-check your own liquidity buffer against your AI and private-market conviction. |

| Energised-site premium — re-price infrastructure and data-centre exposure for secured equipment, interconnection and curtailment risk, not generic land. |

| Private-credit look-through — map exposure by ultimate borrower and structure, and watch the raised-versus-deployed gap, ahead of any capital-treatment tightening. |

| Chokepoint reliability — test war-risk premiums, charter rates and inventory buffers, not just the Brent print, for Hormuz sensitivity. |

|

|

|

Reserve-manager watch — the quiet re-arming

Gold moves to the centre of reserve strategy

OMFIF's Global Public Investor 2026 — drawing on around 90 central banks, pension and sovereign funds managing over US$10tn — finds that for the first time since 2023, a net share of central banks plan to reduce dollar holdings over the coming decade. 82% now hold physical gold (up from 71%), a net 30% intend to add more over the next one to two years, and 51% cite protection against geopolitical risk. Read alongside Japan and Temasek, it is the same instinct expressed by the world's most conservative investors: lean into the future, but re-arm the balance sheet with insurance while you do it. OMFIF.

|

|

|

Policy & Capital Flow Watch

• Japan's GPIF signal is proposed, not deployed. Treat it as a governance and flow watch item into the July 21 cabinet blueprint, not a completed reallocation.

• Central-bank gold-buying continues. The PBOC added to reserves for a 20th straight month on the latest data — the clearest ongoing example of the OMFIF survey turning into flows.

• Sovereign real assets. Norway's NBIM signed a ~US$500m US open-air-retail real-estate joint venture (49%) with Asana Partners — deepening a US real-asset footprint even as it trims elsewhere.

• New sovereign architecture. Kenya enacted its Sovereign Wealth Fund Act, earmarking 30% of resource revenue for future generations — a frontier template to watch, not yet a funded flow.

• Sovereign-debt discipline. Argentina made a ~US$4.3bn foreign-law bond payment while still short of a full return to global capital markets — a reminder that access, not just solvency, defines EM risk.

|

|

|

Research note — the hidden correlation

Conviction and caution are being expressed at once

Connect the wires. Governments want institutional capital to do more — Japan asks GPIF to buy at home; sovereign funds pour strategic money into AI; CPP underwrites the grid. Yet the same institutions are building the largest liquidity and gold buffers in years, because the build-out's constraints — power delivery, chokepoint risk, private-market liquidity, regulatory look-through — are becoming visible at the same moment. That is the period's real signal: the smartest long-horizon owners are financing the future at scale and quietly re-arming their balance sheets against it. For a universal owner the risk is not any single headline; it is that policy ambition, governance visibility and physical delivery are drifting out of alignment on the same pools of capital.

|

|

|

The Big Picture

Markets stayed calm while the physical and institutional signals worsened

The day's sharpest contradiction is the quiet one. Oil settled comparatively soft even as tanker movements and marine coverage deteriorated; officials urged capital home even as portfolio-governance frameworks stayed formally unchanged; and reinsurance rates kept falling — Guy Carpenter's global property-catastrophe rate-on-line is down about 16% in 2026, the steepest drop since the late 1990s — precisely as climate risk rises. The Bank of England's July Financial Stability Report supplies the system map behind these separate headlines, linking AI-equity concentration, infrastructure financing, private-credit opacity and sovereign-debt risk; UAO covered it earlier and retains it only as backbone. The through-line for owners: the state is seeking a larger claim on long-horizon pools, but the governance, pricing and delivery systems needed to execute that ambition are not keeping pace.

|

|

|

From the research desk — this week's institutional reading

• IE University, Sovereign Wealth Funds 2026 — tracked direct investment up 91% to US$404bn on fewer deals; one-third AI; US$220.4bn to the US. IE.

• OMFIF, Global Public Investor 2026 — first net dollar-trim intent since 2023; 82% hold gold, net 30% adding. OMFIF.

• Guy Carpenter (via Artemis) — global property-cat rate-on-line down ~16% at 2026 renewals, steepest since the late 1990s; abundant capital chasing catastrophe risk. Artemis.

• Bank of England, Financial Stability Report — the system map connecting AI concentration, private markets and sovereign-debt risk. BoE.

|

|

|

Chart of the day

Source: GPIF portfolio (¥293.6tn, end-March 2026); Reuters, July 10 2026. Illustrative sensitivity — no reallocation has been approved. GPIF's basic portfolio is set around its long-term pension objective. |

|

Scenario Lab — today

The Hormuz Shipping Disruption Scenario

Built this morning from live signals: with tracked transits collapsing toward zero and only a 17.4% probability of near-term normalisation, the desk maps how a sustained Hormuz disruption propagates — oil and LNG pricing, shipping costs, war-risk insurance, supply chains — through to universal-owner exposure. Explore the interactive relationship map, the probability, and the desk's reasoning.

|

|

|

Tool of the day

The UAO allocator toolkit

Stress a domestic-versus-foreign sleeve against a home-bias mandate, and a liquidity buffer against your AI and private-market conviction — the Temasek barbell, run on your own book.

|

|

Deep dive — When the benchmark is national resilience

The question. For two decades the largest asset owners were understood as diversified financial investors: maximise risk-adjusted return, hold the market, harvest the premia. Japan's pension message, the IE University data and Temasek's barbell point at a different model taking shape — one in which strategic national objectives sit alongside, and sometimes ahead of, financial return, and in which conviction is deliberately paired with insurance. The question for a universal owner is whether this is a passing feature of a fragmented moment or a durable change in what long-horizon capital is for.

Why it is structural. Three forces push the same way. Fiscal strain makes captive domestic pools attractive to finance government debt. Currency and industrial-policy pressure make home-bias politically useful. And the contest over AI, semiconductors and critical minerals makes strategic ownership — not just financial exposure — a national-security objective. The IE evidence quantifies the drift: fewer deals, far larger cheques, a third of it AI, and 12 new state-backed vehicles created to do this work. Japan supplies the pension analogue; Temasek supplies the sophisticated-investor response. These are not diversifiable preferences; they are a change in the marginal investor's utility function.

The tension. A strategic mandate changes return thresholds, holding periods, concentration and governance. It can be stabilising — patient capital that underwrites compute and resilient infrastructure through volatility. It can also be fragile: a portfolio built around national access can reverse abruptly when fiscal or geopolitical conditions shift, and a pension reserve asked to defend a currency inherits an obligation its beneficiaries never voted for. That is why the barbell matters. Temasek's answer — overweight the theme, but hold a quarter of the book liquid and keep most AI exposure liquid too — is a template for expressing conviction without surrendering the optionality to survive the very constraints (power, chokepoints, private-market liquidity, regulatory look-through) that could throttle the trade. Meanwhile the transparency needed to supervise these larger, more concentrated, more cross-border positions is moving the wrong way, as the private-credit data impasse shows. The mandate is being pulled wider while the instruments to govern it narrow.

Allocator posture. Treat “strategic” sovereign and pension capital as a distinct factor with policy loadings, not as an ordinary co-investor — its time horizon, exit behaviour and mandate can change with an election or a budget. Write down, in advance, where a home-bias or strategic-industry instruction would conflict with beneficiary-first duty, so the governance answer exists before the political request does. Match every unit of AI-build-out conviction with a deliberate liquidity reserve, as the best-run state investors are doing. Price the physical bottleneck — energised sites, secured equipment, interconnection, curtailment risk — as the real constraint on the AI thesis every sovereign is now buying. And demand look-through on private-credit and reinsurance structures now, before regulators impose it through capital charges. When you own the whole market, the job is not to beat it; it is to design for the constraints becoming binding — and the state's growing claim on the mandate is now one of them.

|

Researched and edited by the UAO editorial desk. Figures trace to the named sources above. Where a development is a stated objective rather than an approved decision — as with Japan's GPIF signal and Temasek's AI target — we say so rather than overstate it. Universal Asset Owners · For institutional allocators and the ecosystem that serves them · View online · universalassetowners.com · info@universalassetowners.com |

|

|