UNIVERSAL ASSET OWNERS The UAO Daily Brief Volume 1, Issue 54 · Tuesday, July 7, 2026 · 7:00am ET / 15:00 GST SOVEREIGN WEALTH MONITOR · OIL CASH DOWN, AI BETS UP |

|

LISTEN · THE UNIVERSAL OWNER |

We got something wrong yesterday, and we would rather fix it loudly than quietly. Monday’s brief said “roughly 50,000 customers near Lake Tahoe were told to find a new power provider amid data-center-driven demand.” That framing was misleading, and a reader kindly and rightly flagged it.

The accurate picture: the ~50,000 are customers of Liberty Utilities, and it is Liberty, not its customers, that must line up a new wholesale supplier after NV Energy declined to renew (announced March 2026, extended to end-2027; transition around 2028). Liberty says customers keep their service, and NV Energy cited data-center load among several factors. We drew the line from a July 3 Al Jazeera report, but that does not excuse us — we should have checked the utility’s and regulator’s own statements. We’ve corrected the online version and tightened our process.

Our thanks to the reader, K.N., who raised it — we’re grateful for the scrutiny. If you ever see something off, tell us: info@universalassetowners.com.

The lab tracks whether a softer oil bid forces smaller, more-syndicated Gulf cheques — and where non-Gulf owners get better entry terms. Full editorial decomposition in today’s deep dive below.

| Open the live Scenario Lab → |

The oil revenue that ultimately backs the Gulf’s largest sovereign investors softened this week — even as their deployment ambitions kept rising. Saudi Aramco set its August crude to Asia at a discount, the first since 2020 and the deepest one-month cut in over two decades, and OPEC+ approved a fifth straight increase into a softening market. Today: what a softer oil complex means for the funds now among the most active buyers of global infrastructure; the $49bn AI counter-track; India’s savings rails; and two signals from the governance layer.

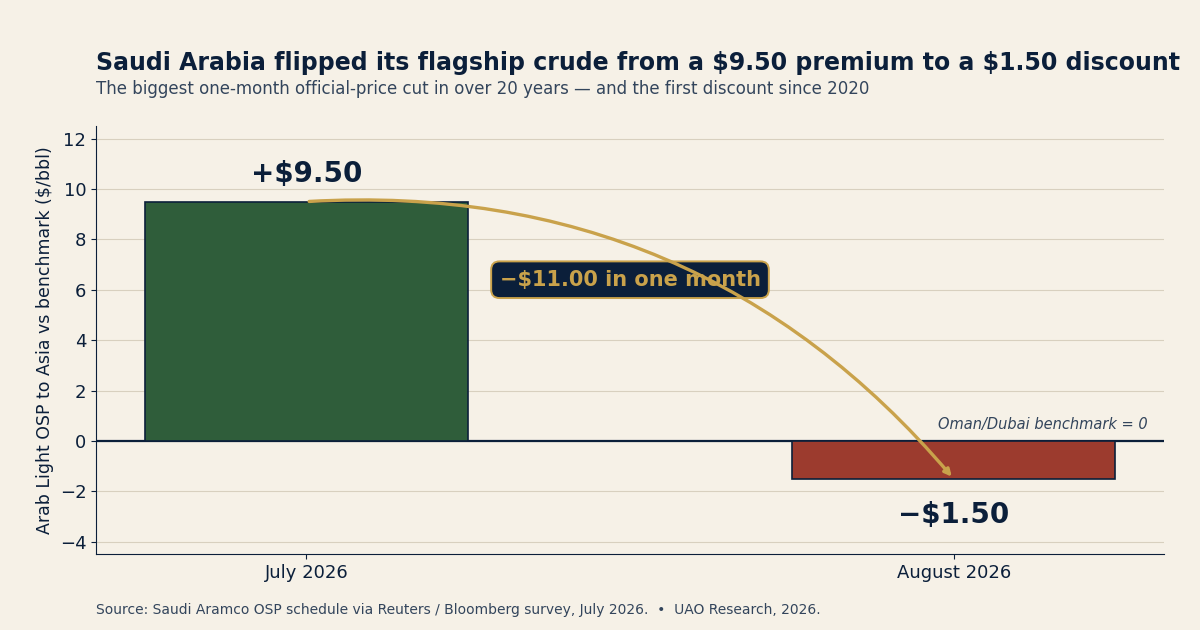

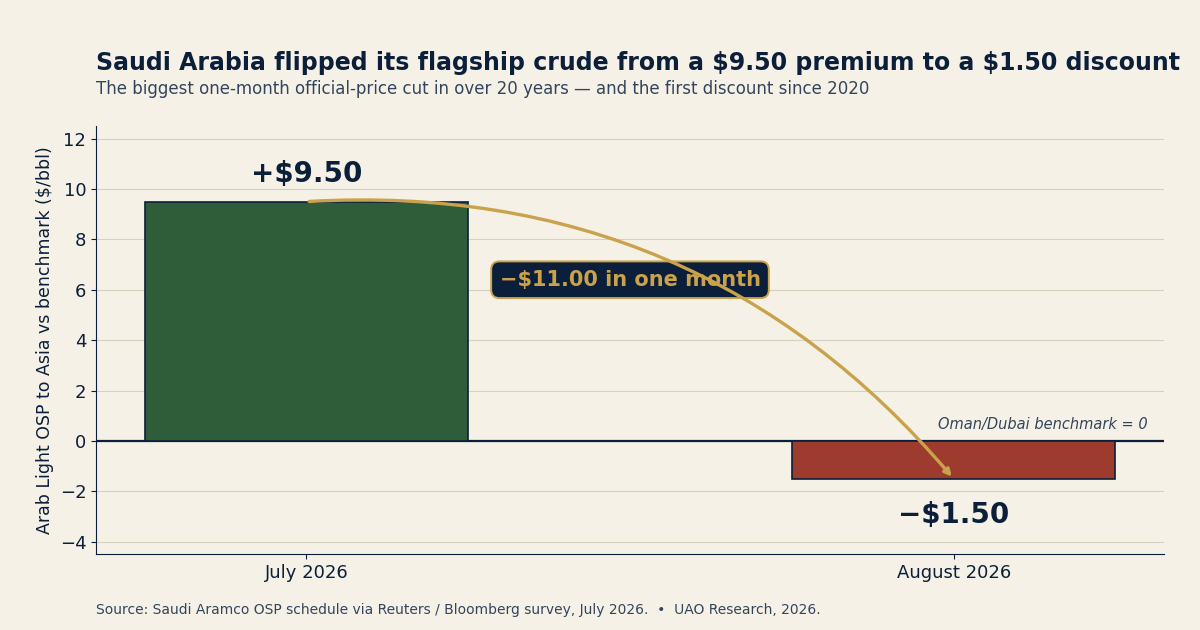

1. Saudi Arabia cut the official price of its flagship Asian crude by the most in over 20 years.

Saudi Aramco set the August official selling price (OSP) for Arab Light to Asia at $1.50 a barrel below the Oman/Dubai benchmark — down from a $9.50 premium in July. The $11 single-month cut is the largest in more than two decades, and the resulting discount is the lowest since June 2020. The OSP is a sovereign pricing decision, not a market price; a cut this size — even with Brent bouncing to around $73 but down more than a fifth on the month — signals Riyadh is reading soft demand and choosing to keep barrels moving.

Implication for owners: The receipt this OSP touches directly is Saudi Arabia’s, and PIF is most exposed; for Abu Dhabi’s ADIA and Mubadala and Qatar’s QIA the read is indirect. Saudi fiscal-breakeven estimates have generally sat above spot Brent, so a lower-for-longer path tightens the room between the budget, Vision 2030 spending and sovereign deployment.

| Read the full story → |

Sources: Reuters, July 6, 2026.

2. OPEC+ is defending market share, not price — a fifth straight hike.

On July 5, OPEC+ approved a fifth consecutive monthly increase of 188,000 b/d for next month, with Saudi Arabia taking the largest single share, about 62,000 b/d. The market has swung from wartime scarcity toward post-war oversupply anxiety. Riyadh has chosen volume over price — a defensible long-horizon call that nonetheless front-loads fiscal pressure onto the budgets that seed the region’s sovereign funds.

Sources: CNBC, July 6, 2026.

3. The other track hasn’t blinked: Gulf capital is still scaling the AI build-out.

Abu Dhabi’s MGX closed its first fund at $49 billion — above a $45 billion target (announced July 1; dated background). MGX, formed by Mubadala (whose assets rose 17% in 2025 to about $385bn) and G42, holds positions across the AI stack. Invesco’s 2026 sovereign study — 144 institutions — finds infrastructure now 9.0% of SWF assets (from 4.9% in 2022) with 77% calling AI transformative. The paradox: revenue compressing, deployment ambition expanding.

Sources: The National, Jul 1, 2026; Invesco IGSAMS 2026.

4. Sovereign capital is buying India’s savings rails, not just its companies.

ADIA and Singapore’s GIC are drawing into the ~$1.2 billion IPO of SBI Funds Management, India’s largest asset manager (₹12.5 trillion / ~$131bn AUM; ~$12.3bn valuation). The offer is expected to open the week of July 13. This is a position in the toll road for Indian savings — own the rails, not the riders.

Sources: Reuters, Jul 2026.

5. The committee is now a risk factor.

ADIA’s Bernd Scherer argues in a 2026 CFA Institute Research Foundation monograph that traditional investment committees can amplify group bias — drifting toward “the salient story of the day.” His fix: anonymous portfolio-vector averaging. When oil cash, AI capex, inflation and liquidity all reprice at once, the process that locks in yesterday’s consensus is the exposure.

Sources: CFA Institute Research Foundation, 2026.

6. Liquidity is back as a governance asset.

Ohio STRS puts 12-month U.S. recession odds at an average 23% and its FY27 plan leans into liquidity against ~$4bn/yr of negative cash flow — cutting domestic-equity target 26%→19.25%, international 22%→15.75%, adding a 7% liquid-alternatives sleeve. The Gulf is the source-of-capital side; Ohio STRS is the liability-owner side of the same regime shift.

Sources: Pensions & Investments, 2026.

Previ forces out Vale’s chairman. Brazil’s Previ (Banco do Brasil pension, 7% of Vale) pushed a vote to remove chairman Daniel Stieler; he resigned July 6 ahead of a July 22 meeting. Reuters/Mining.com

Bank of Israel cuts to 3.5%. A 25bp cut on July 6 — second straight, lowest since 2022 — inflation 1.9%, 2026 GDP seen +4.0%. Bloomberg

In one month, Saudi Arabia flipped its flagship crude from a $9.50 premium to a $1.50 discount — the biggest swing in over 20 years.

Source: Saudi Aramco OSP schedule, via Reuters, July 2026. UAO Research, 2026.

“The Gulf’s funds have spent a decade being called patient, permanent capital. The next few years test a subtler claim: that they are counter-cyclical capital. Watch whether outbound deals get smaller, slower or more heavily syndicated — that is where compression shows up first, not in the rhetoric, in the cheque size.”

Aramco’s September OSP (early August) — a second cut would confirm lower-for-longer.

Gulf fund deal cadence through Q3 — cheque size and syndication are the tell.

SBI Funds Management pricing (mid-July) — how much ADIA and GIC actually take.

Samsung & hyperscaler capex prints — the demand-side test of the AI build-out.

Sovereign oil revenue, pension liabilities and the AI build-out all bend to the same underlying force: demographics. The Demographic Overlay maps population, workforce and dependency trends onto long-horizon portfolios — free on UAO.

| Open the Demographic Overlay → |

Issue No. 05 · “The New Cap Table.” Read the flip-book on the site.

| Read the flip-book → |

The Sovereign Paradox: Less Oil Margin, More AI Ambition

The question. Two things happened in the Gulf within seventy-two hours, and they pointed in opposite directions. Saudi Aramco cut the official price of its flagship crude to Asia by the most in more than two decades — an $11 swing that took the August Arab Light OSP from a $9.50 premium to a $1.50 discount, the first discount since 2020 — and OPEC+ approved a fifth consecutive monthly production increase into a market that has swung from wartime scarcity toward post-war oversupply. That is the revenue track, compressing. In the same window, Abu Dhabi’s MGX closed a $49 billion AI fund (announced July 1), and Invesco’s 2026 sovereign study confirmed infrastructure as the fastest-growing asset class across sovereign portfolios. That is the deployment track, expanding. The question a universal owner must answer, before co-investing another dollar alongside these funds, is not merely whether both tracks can run at once — it is who provides the liquidity when the Gulf’s sovereign anchor becomes more selective.

What the evidence says

Start with the cash. The OSP is not a market price; it is a sovereign pricing decision, made monthly, that sets what Asian refiners pay Saudi Arabia directly. A cut of this size — the largest one-month move in over twenty years, to the lowest official price since June 2020 — is a deliberate choice to defend volume over margin. Layered on top is the fifth OPEC+ quota increase of 188,000 b/d, with Saudi Arabia taking the largest single share (about 62,000 b/d), and a Brent price that, even after a small bounce to around $73, is down more than a fifth over the past month, with the Strait of Hormuz war premium largely unwound. For at least the coming quarter, the Gulf’s hydrocarbon pricing power is weaker, and Saudi’s marginal barrel is being repriced in a buyer’s market.

Now the deployment. MGX — formed by Mubadala (whose assets rose 17% in 2025 to about $385 billion) and G42 — closed Fund I at $49 billion, above its $45 billion target, with positions spanning the AI stack from semiconductors to frontier labs. That is not an outlier. Invesco’s 14th annual Global Sovereign Asset Management Study — 144 institutions, 90 sovereign funds and 54 central banks — finds infrastructure has risen to 9.0% of SWF assets from 4.9% in 2022, that 65% of SWFs now name private markets a key return driver, and that 77% regard AI as a transformative, multi-decade force, with energy security and transition infrastructure rated the most credible resilience theme by 80%. The deployment ambition is structural and rising even as the funding is cyclical and falling.

Where it is contested

The counterargument is scale, and it is a serious one: ADIA, QIA, Mubadala and PIF are not pass-through oil accounts. They hold financial assets, recycle distributions, issue debt, co-invest and stagger commitments — so a soft oil quarter does not force a sovereign retreat. Mubadala’s own 2025 results, a 17% rise in assets even amid record deployment, are exhibit A. But that comfort papers over three things the evidence does not resolve. First, timing: AI infrastructure commitments are front-loaded and contractual — a data-centre or compute deal does not flex with the oil tape — while the offsetting revenue is the part that moves. Second, the fiscal claim on the funds: Saudi fiscal-breakeven estimates have generally sat above spot Brent in recent years, so lower realized prices tighten the room between the state budget, Vision 2030 spending and sovereign deployment, and a state that needs the oil money competes with its own fund for those receipts. Third, concentration: the same funds are pivoting into a single macro bet — AI and its power and data infrastructure — precisely as one demand-side signal after another shows how correlated that exposure has become. Whether that is prudent diversification into real assets or a crowded trade dressed as infrastructure is genuinely unsettled.

From the allocator’s seat

For a CIO co-investing alongside Gulf capital, the read is not “the Gulf is retreating” — it isn’t — but “the Gulf’s cost of patience just went up.” Expect the compression to show up in the terms, not the thesis: cheque sizes that syndicate more widely, more co-investment offered to spread the funding load, slower drawdown pacing, and harder negotiation on fees and governance rights as the anchor demands more for its capital. That is the opportunity, and it is a specific one. The play for non-Gulf universal owners is not to bet against the Gulf; it is to underwrite when Gulf capital becomes more price-sensitive, more syndication-friendly and more demanding on governance — stepping into deals fully-funded by a single Gulf sponsor a year ago, on better entry terms.

It also raises the diligence bar. Model the scenario where your Gulf co-investor becomes a seller of liquidity, not just a provider, and price the correlation between your energy exposure, your AI-infrastructure exposure, and your co-investor’s balance sheet — three things that used to be independent and are now, quietly, the same trade. And take Bernd Scherer’s recent research on investment committees seriously on your own board: in a regime moving this fast, the committee process that averages toward the consensus of the last meeting is itself a risk to underwrite.

What to watch next

Four signals will resolve the question. Aramco’s September OSP (early August): a second monthly cut would confirm a lower-for-longer posture. Gulf fund deal cadence through Q3: cheque size and syndication are the tell. SBI Funds Management pricing and the sovereign anchor allocations (mid-July): how much ADIA and GIC actually take is a real-time read on sovereign appetite for owning emerging-market savings infrastructure. And Samsung and hyperscaler capex prints: the demand-side test of whether the AI build-out the Gulf is financing is still accelerating.

Sources: Reuters; CNBC; The National; Invesco IGSAMS 2026; CFA Institute RF.

UNIVERSAL ASSET OWNERS Intelligence for long-horizon capital. Published each weekday at 7:00am ET. universalassetowners.com · info@universalassetowners.com Not investment advice. © 2026 Universal Asset Owners. |