|

UNIVERSAL ASSET OWNERS

The UAO Daily Brief

Volume 1, Issue 49 · Wednesday, July 1, 2026 · 7:00am ET / 15:00 GST

PENSION GOVERNANCE WATCH · CALPERS GOES TOTAL-PORTFOLIO TODAY

|

Today is not just an asset-allocation change. It is a governance change. Effective July 1, CalPERS — the largest US defined-benefit public pension, ~$556bn — begins operating under a Total Portfolio Approach. The old model asked how full each bucket of the policy table should be; the new model asks a harder question: does this decision improve the total fund?

The board adopted a single 75/25 reference portfolio to judge what staff build, replacing the 11 asset-class benchmarks used before. It is the operating language of New Zealand Super, GIC, CPP and Australia's Future Fund; what is new is a large, politically governed American public plan adopting it in the open. Which US public pension follows — and which cannot?

1. CalPERS retires the allocation bucket.

The board voted to adopt TPA on November 17, 2025; it now sets total-fund risk through a 75/25 reference portfolio that replaces the 11 asset-class benchmarks used before. CIO Stephen Gilmore targets 50–60 bps; the Thinking Ahead Institute puts the historical TPA-vs-SAA edge at about 1.3% a year over a decade (the study author says ~1.8%; the comparison is imperfect).

Implication for owners: The allocators who win the next decade may not have the best private-equity bucket — they may have the best whole-fund operating system.

| Read the CalPERS announcement → |

2. The real trade is flexibility versus governance risk.

Under TPA the question becomes: did management beat the reference portfolio for the risk it took? That is why the 400-basis-point active-risk limit matters — the guardrail between joined-up management and unbounded discretion. Governance moves from approving buckets to monitoring total-fund risk, liquidity and value-added.

Implication for owners: Weak governance makes TPA look like style drift; strong governance may make SAA look obsolete.

| How the 400bp active-risk limit works → |

Source: CalPERS Investment Committee agenda item 5c (400 bps active-risk limit), Sept 15, 2025; Top1000funds (Dec 2025).

3. The endowment tax takes effect today.

Also effective July 1: the US net investment income tax on the largest private university endowments rises to as much as 8% (from 1.4%), a levy that scales with size. Harvard faces an estimated ~$368m annual bill, Yale ~$280m, Princeton ~$217m — forcing FY2027 budget cuts and accelerating liquidity moves, including Yale's reported ~$6bn private-equity secondary sale.

Implication for owners: A tax on investment income lifts the after-tax hurdle on every illiquid commitment. Expect more endowment secondaries, tighter pacing, and fresh pressure on the illiquidity premium the endowment model was built on.

| The endowment-tax detail → |

Sources: Harvard Financial Administration; Yale Daily News (net investment income tax effective July 1, 2026).

4. Two of the biggest funds change investment leaders — today.

Investment leadership turns over at two major funds effective July 1. At AustralianSuper (~A$410bn / ~$280bn) Shaun Manuell takes the CIO seat as Mark Delaney steps down after roughly 25 years; at Australia's Future Fund (~A$240bn sovereign wealth fund) Richard Brandweiner becomes CIO amid an expanded national-priority mandate spanning housing and the energy transition.

Implication for owners: CIO transitions at this scale are strategy inflection points — internalization, private-market pacing and mandate scope all get re-examined. Watch the first 12 months for shifts in benchmark and risk posture.

Sources: AustralianSuper newsroom; Chief Investment Officer / Bloomberg (both effective July 1, 2026).

Stablecoins Are the Decoy. The Real Sovereign Race Is for the Rails Under Your Portfolio.

The next phase of digital finance is not crypto speculation. It is who controls the programmable rails under sovereign debt, infrastructure, real estate, energy and collateral — the assets the world's largest owners already hold. A UAO investigation into why tokenization is moving from the money layer to the asset layer, and the five risks owners are actually underwriting.

By Naveed Iqbal Contributing Journalist, Digital Assets & Web3 · 8 min read |

About the journalist: Naveed has covered cryptocurrency markets, blockchain infrastructure and tokenization since 2018 — with work across Bitcoinist, NewsBTC, Crypto.news, TechReport and BraveNewCoin. For Universal Asset Owners he covers where digital assets meet the architecture of institutional capital. Full profile →

| Read the full investigation → |

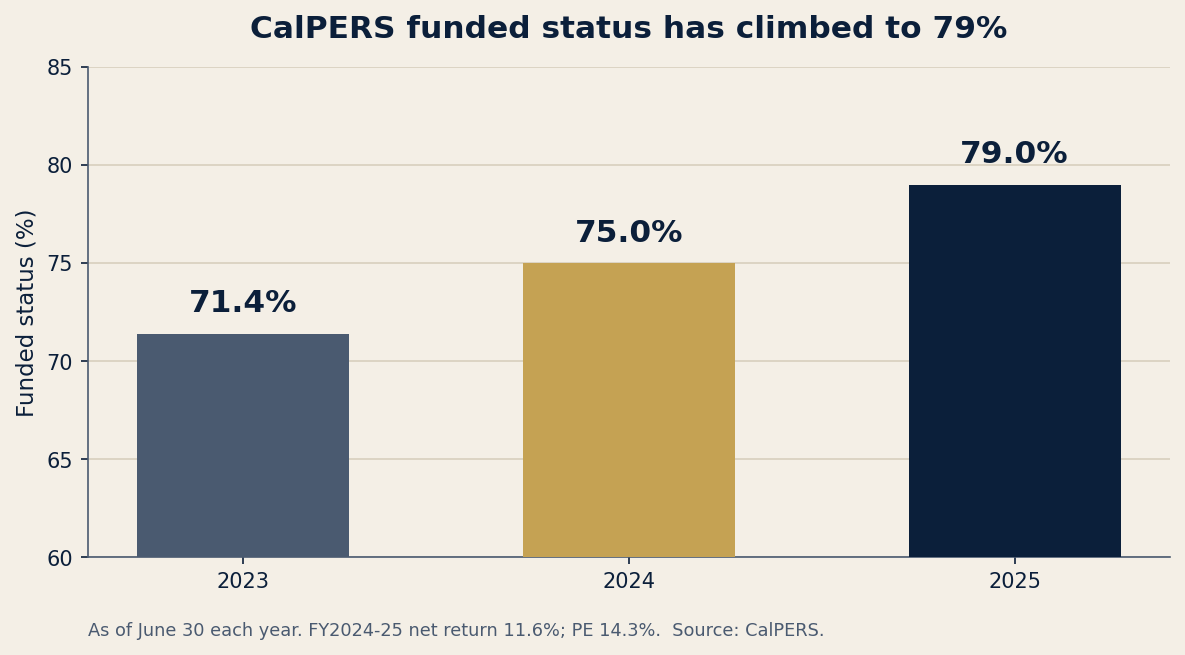

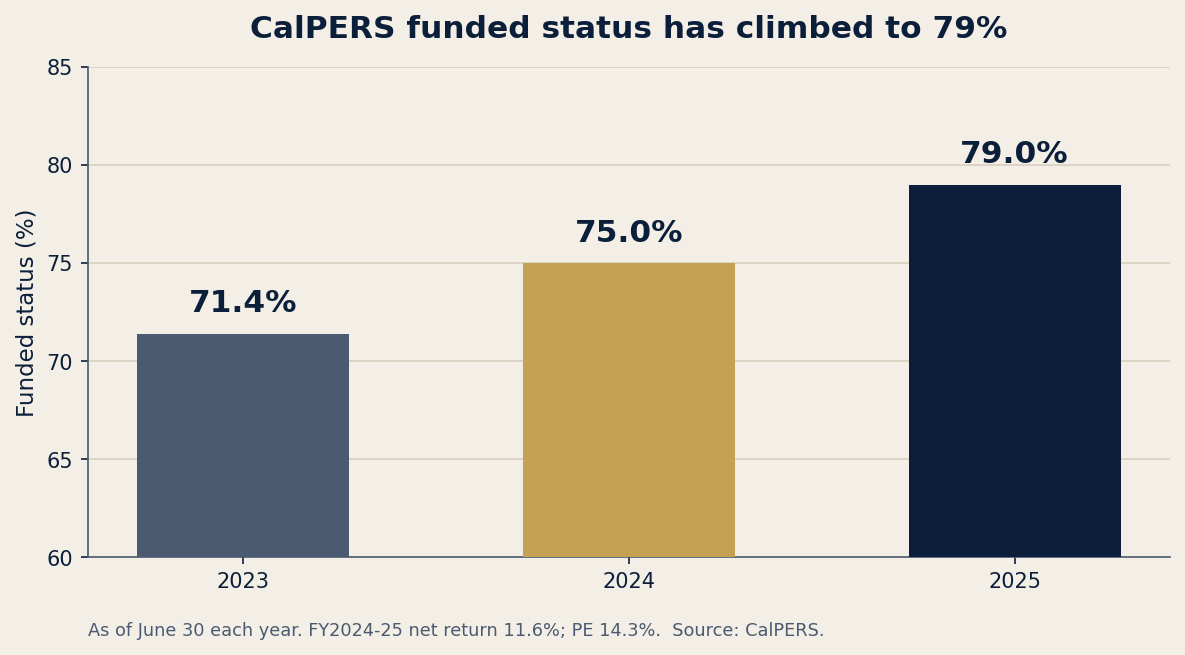

CalPERS enters the total-portfolio era from a stronger base: funded status near 79%.

As of June 30 each year. FY2024-25 preliminary net return 11.6%; PERF AUM ~$556.2bn. Source: CalPERS (July 2025).

Base case: proof point, not immediate domino. Upside: visible value-add makes TPA the top plans' governance language. Downside: one bad year turns the model into a political target. Click any node and ask the desk what happens next.

| Open the live scenario → |

|

WATCH & LISTEN · THE UNIVERSAL OWNER

Today's episode — “The End of the Allocation Bucket” · ~4.5 min (rendered).

|

“The Total Portfolio Approach is not a bet that CalPERS' staff are smarter than an allocation table. It is a bet that the old table was hiding the wrong risks. Without strong board discipline, TPA becomes discretion without memory. With it, it may become the operating system for serious long-horizon capital.”

The second mover. Which large US public pension shifts to a reference-portfolio model next. The near-term candidates are the $367.7bn CalSTRS, already moving to a “one fund approach,” and Maryland State Retirement, reported to be evaluating it. CalSTRS →

CalPERS' first reporting cycle under TPA. With one 75/25 reference portfolio now the yardstick (not 11 asset-class benchmarks), the first performance reports will show whether staff can clearly explain active risk, liquidity and value-add against it. CalPERS investments →

The 400 bps active-risk limit. How far staff actually deviate from the 75/25 reference. Use the room and it is real flexibility; hug the benchmark and TPA is strategic asset allocation with a new name. The board decision →

The Fed, July 28–29. The next FOMC decision (announced July 29), with rates at 3.50–3.75%. A higher-for-longer stance rewards funds that can move capital dynamically — exactly what TPA is built to do. FOMC calendar →

CalPERS' FY2025-26 return, mid-July. CalPERS reports its investment return for the year ended June 30, 2026 — the funded-status backdrop against which this governance shift gets judged. CalPERS newsroom →

Where private money is forming, in near-real time. Every US exempt placement files a Form D within 15 days — this free nowcast reads that volume straight from SEC EDGAR, the pulse of private-capital formation the public indices never see.

| Open the nowcast → |

The End of the Allocation Bucket

The question. Today CalPERS (~$556bn) retires the strategic asset allocation model it has used for decades, replacing 11 asset-class benchmarks with a single 75/25 equity-bond reference portfolio. That, on its own, is not a market event. The consequential question is whether it is the first domino: by 2030, will a majority of the ten largest US public pensions have replaced SAA with a reference-portfolio framework? The answer changes what “the benchmark” means for over $2 trillion of American retirement capital.

What the evidence says. Under SAA a board sets targets by asset class and staff fill each bucket to weight — easy to govern, but its rigid boundaries force capital into an asset class even when the relative opportunity is poor. TPA discards the buckets: every investment, from a private-credit loan to a venture fund, competes against a single reference portfolio, here paired with a 400-basis-point active-risk limit. The intellectual cover is a Thinking Ahead Institute study of 26 TPA asset owners that found them beating SAA peers by roughly 1.3% a year over a decade. Notably, CalPERS' own CIO Stephen Gilmore — a veteran of TPA pioneers the Future Fund and NZ Super — publicly downplayed that number: “130 basis points is based on a small sample… I wouldn't place too much reliance on that,” setting his own target at a more modest 50–60 bps. On a $556bn base, even 50 bps is roughly $2.7bn of annual value-add.

The contested core: governance and accountability. TPA is fundamentally a transfer of fiduciary power — from an elected/appointed board that controls the allocation table to unelected investment staff. For Singapore's GIC that delegation is standard; for a US public pension accountable to taxpayers and politicians it is a profound shift. Critics argue the outperformance of early adopters (CPP, NZ Super, the Future Fund) suffers from survivorship bias — these are exceptionally resourced institutions, and attributing their success to the framework rather than their talent and independence confuses correlation with causation. Timothy Atwill and Jason Malinowski, CIOs of the Tacoma and Seattle plans, argued in early 2026 that TPA “weakens governance” by forcing boards to monitor obscure risk factors instead of clear asset-class limits; Morningstar finds the average tactical-allocation fund has persistently lagged a static balanced index while charging some of the category's highest fees (expense ratios averaging ~1.4%).

The contrarian view: a single point of failure. The deepest irony is timing. CalPERS is anchoring a 75/25 US-equity-heavy reference portfolio just as the pioneers turn cautious: in its 2026 five-yearly review NZ Super — whose active portfolio has added a cumulative NZ$19bn above its reference since 2010 — cut its long-term return expectation, citing overvalued US equities. And where GIC and NZ Super insist their reference portfolios are not benchmarks but expressions of risk appetite, CalPERS has labelled its 75/25 a benchmark to judge staff — risking re-importing the benchmark-hugging TPA was meant to kill. If the ten largest US public pensions all converge on the same 75/25 posture and the same yardstick, the homogenization of the largest pools of patient capital makes correlated behavior in a drawdown more likely. The “American standard” could become a systemic single point of failure.

The domino effect. The industry is already splitting. The $367.7bn CalSTRS is moving toward a “one fund approach,” with CIO Scott Chan reporting that dynamic, cross-asset allocation has begun to generate alpha. Conversely, Monte Tarbox, CIO of the ~$316bn New York City Bureau of Asset Management, flatly rejected it: “I haven't drunk the TPA Kool-Aid,” questioning whether US public funds have the governance to run it safely — or whether it “just makes the job… more fun, more sexy, more interesting.”

What to watch next. Three signals decide whether TPA becomes the American standard or a Californian experiment. The tracking-error test: if CalPERS' active risk stays below ~100 bps in year one, the board has simply renamed SAA. The legislative reaction: California's SB 1319, a private-equity transparency bill CalPERS opposes as impairing its private-market access, tests how politicians treat wider staff discretion. The Maryland decision: Maryland State Retirement is evaluating TPA; if an East Coast fund adopts it, the doctrine has crossed the country.

Sources: CalPERS board (Nov 2025) · Top1000funds (Gilmore, Dec 2025) · CalPERS FY24-25 return · NZ Super (2026) · NYC / Tarbox (2026) · Morningstar · NCPERS (2026).

|

UNIVERSAL ASSET OWNERS

Intelligence for long-horizon capital. Published each weekday at 7:00am ET.

universalassetowners.com |