The next phase of digital finance is not about crypto speculation. It is about who controls the programmable rails under sovereign debt, infrastructure, real estate, energy and collateral — the assets the world’s largest owners already hold.

In late June 2026, the architecture of digital capital stopped looking like a crypto story and started looking like statecraft.

On 18 June, U.S. financial agencies proposed customer-identification rules for permitted payment stablecoin issuers under the GENIUS Act, pulling dollar stablecoins deeper inside the Bank Secrecy Act perimeter. Five days later, the Bank for International Settlements (BIS) published a chapter of its Annual Economic Report warning that stablecoins, as currently designed, fall short of the foundational properties of money.

At first glance these look like opposing signals — Washington integrating stablecoins, Basel warning against them. That is the surface story.

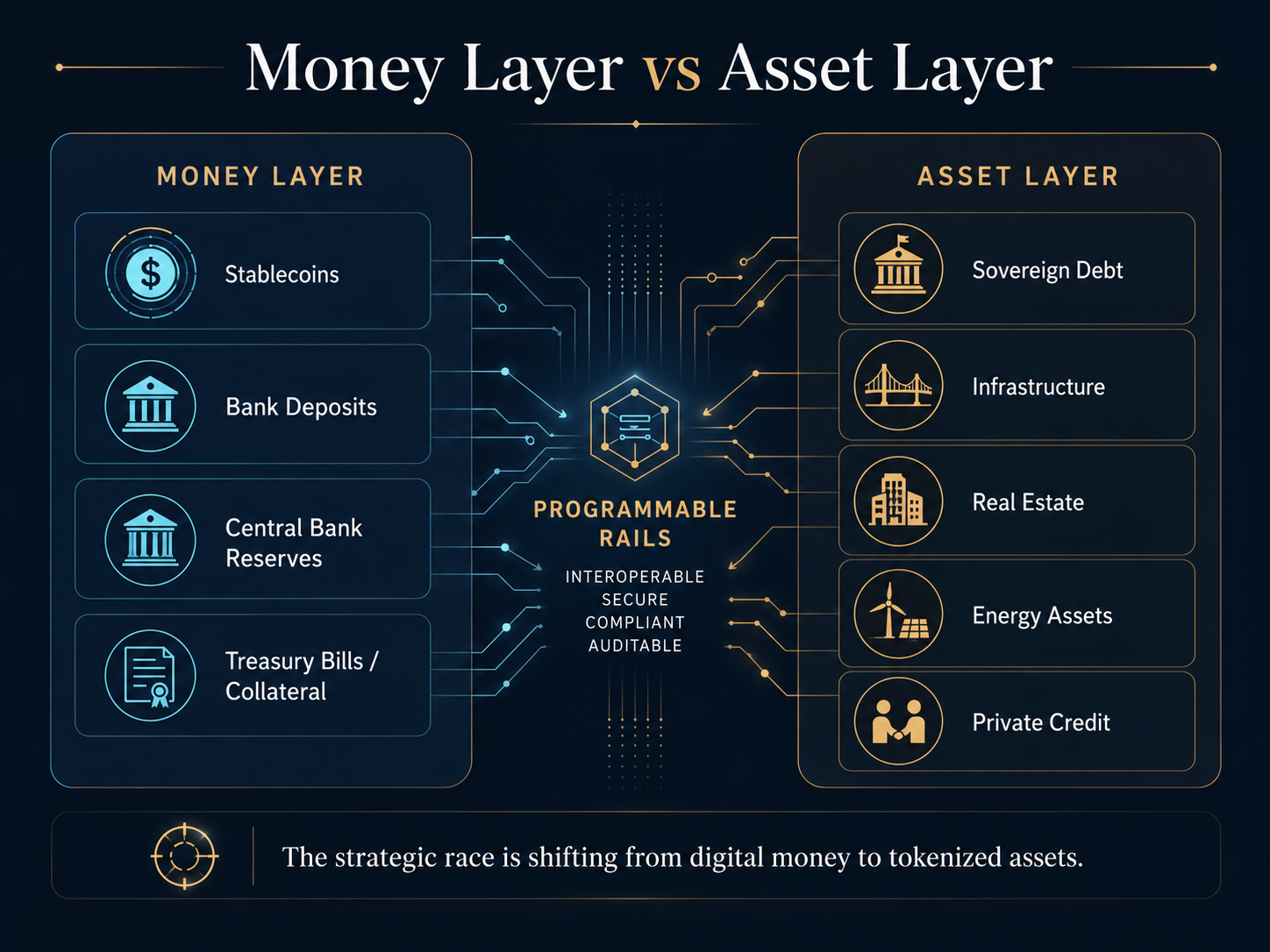

The more important shift is that tokenization is moving from the liability side of the system to the asset side. The fight over stablecoins is about who may issue digital claims on dollars. The strategic fight now beginning is about who will control the programmable infrastructure underneath sovereign debt, infrastructure, real estate, energy, private credit and collateral.

For sovereign wealth funds, public pensions, insurers and endowments, that is the real story. The risk is not that a fund buys the wrong stablecoin. It is that assets already in the portfolio may soon be financed, transferred, priced, collateralized and marked on rails the owner did not design, govern or fully understand.

The market is still debating the coin. The states are moving to the rails.

The money layer: what the central banks are defending

The BIS argument is not anti-technology; it is anti-unsound-money. Its core claim is “singleness” — that every form of the dollar must redeem at par into central bank money, even under stress. Stablecoins strain that because they are privately issued, bearer-like instruments on fragmented public ledgers; small deviations from par can turn systemic when confidence breaks.

The BIS put stablecoin market value at roughly $320 billion at end-May 2026 — modest beside bank deposits, but already large enough to matter at the margin of Treasury markets and dollar plumbing. Its answer is a “unified ledger”: tokenized central-bank reserves, commercial-bank money and tokenized assets in one regulated venue. Project Agorá — eight central banks (now including the Bank of Canada) spanning five reserve currencies, and more than 40 private institutions — is the live test case, and in May 2026 it advanced to real-value testing. This is not a rejection of tokenization. It is an attempt to domesticate it.

The U.S. layer: stablecoins as dollar infrastructure

Washington is not trying to stop dollar stablecoins; it is regulating them into the dollar system. The June rule treats issuers as financial institutions under the Bank Secrecy Act; an April FinCEN/OFAC rule adds anti-money-laundering and sanctions obligations. Together they convert stablecoins from a crypto workaround into a regulated dollar-distribution channel.

The investment consequence is mechanical, not ideological. Dollar stablecoins are backed by short-dated dollar assets, so issuance growth means structural demand for Treasury bills and repo. Tether alone reported about $141 billion of U.S. Treasury exposure in the first quarter of 2026 — which would rank it near the 17th-largest holder of U.S. Treasuries in the world, ahead of Germany, the UAE and Australia.

The non-obvious point for allocators: stablecoins may never become money, but they are already becoming a new class of structural Treasury buyer — and a lever of dollar reach. The same mechanism runs in reverse for everyone else. The BIS warns that stablecoin dollarization can destabilize capital flows and erode monetary sovereignty in weaker economies. The U.S. exports dollar reach; others may import dollarization.

The Gulf layer: tokenize the asset, not the money

The most interesting posture is neither the U.S. money play nor the BIS defense. It is the asset-layer play — and the Gulf is its clearest expression. The signal here is regulatory, not promotional. Saudi Arabia’s central bank (SAMA) is running a blockchain sandbox whose early pilots include tokenizing Riyadh commercial real estate, and the Capital Market Authority has moved to define tokenization rules. In the UAE, a multi-regulator framework is already live: Dubai’s VARA licenses tokenized real-world assets, the DFSA has opened a tokenization sandbox in the DIFC for tokenized equities, sukuk and fund units, and Abu Dhabi’s ADGM is maturing rules for tokenized securities. Private vendors are circling the opportunity too — Open World, a blockchain firm merging into a Nasdaq-listed shell, announced a “tokenization center of excellence” in Al Khobar in January — but the durable signal is the regulators, not the press releases.

Why this matters for universal owners: a dollar stablecoin is a liability claim; a tokenized infrastructure asset is a claim on cash flows; a tokenized sovereign bond is a claim on state credit. The money layer decides settlement. The asset layer decides what gets financed, who owns it, how collateral moves and which investors get access. The Gulf’s edge is not a better coin — it is that it owns or influences vast pools of strategic assets that global capital wants exposure to. Saudi Arabia’s Public Investment Fund, whose 2026–2030 strategy tilts to roughly 80% domestic investment across tourism, urban development, advanced manufacturing, logistics, clean energy and NEOM, sits squarely on the asset classes most likely to be financed on programmable rails. Tokenization may not begin with the most liquid assets. It may begin where claims are complex, capital formation is strategic, and the sovereign wants to control distribution.

Four blocs, four sovereignty strategies

Tokenization is fragmenting into geopolitical blocs, and the mistake is to read them as competing crypto policies. They are competing financial-sovereignty strategies. The U.S. wants the world to use tokenized dollars. The BIS wants tokenization without monetary fragmentation. The Gulf wants to convert strategic physical assets into globally distributable claims. China wants the technology without surrendering control — the e-CNY for domestic reach and Project mBridge for cross-border settlement that routes around Western infrastructure; tellingly, the BIS stepped back from mBridge in late 2024, leaving a China-anchored consortium to carry it. The universal owner is invested across all four regimes at once.

The repricing risk is in the wrapper, not the token

The live question is not whether tokenization is real. Tokenized U.S. Treasuries passed $10 billion in January 2026, and Circle’s USYC edged past BlackRock’s BUIDL as the largest product — not because Circle is the stronger brand, but because distribution, minimum-investment thresholds, collateral utility and exchange integration mattered more than the name on the door.

That is the lesson: in tokenized markets the wrapper is not administrative. The wrapper determines distribution, liquidity, collateral eligibility, access, transferability, reporting — and therefore price. Which creates a new diligence problem: the phantom liquidity premium. When a private-credit, real-estate or infrastructure asset is tokenized, owners are told they are receiving liquidity. But is it real liquidity — broad demand, enforceable transfer rights, reliable settlement — or wrapper liquidity, a thin venue subject to gating, oracle and smart-contract risk, and platform dependency? A tokenized asset can trade around the clock and still be economically illiquid. The token does not remove the underlying risk; it changes how that risk is distributed, financed and observed.

The five risks owners are actually underwriting

Tokenization will not erase the illiquidity premium. It will itemize it. Owners who can price these five layers separately will be paid; owners who treat “tokenized” as a generic liquidity upgrade will overpay.

- Monetary risk (par & finality). Does the rail settle with true finality, and does the money leg redeem at par under stress?

- Wrapper risk (legal rights). Is the token enforceable title — redemption, transfer, governing law, bankruptcy-remoteness — or merely a pointer to a claim?

- Liquidity illusion (real depth). Is there genuine two-sided demand, or a thin venue dressed up as liquidity?

- Platform dependency (control of the rail). How concentrated is the issuer or venue, and what are the smart-contract, oracle and custody failure modes?

- Sovereign alignment (alignment of interests). Whose jurisdiction governs the rail, and do its incentives align with the owner’s — or with the state that controls it?

What this means in the boardroom

The questions differ by owner. For sovereign funds the question is offensive — should we own the rails that distribute claims on our own national assets? If tokenization becomes the distribution layer for sovereign assets, platform governance becomes an arm of financial sovereignty. For public pensions it is defensive — which assets in the book get re-priced against tokenized comparables trading around the clock, even when that pricing is shallow? The accounting lag that protected private marks becomes harder to defend. For insurers it is collateral and duration — admissibility, custody, capital treatment, liquidity recognition. For endowments and family offices it is access versus governance, because access without governance is not sophistication.

The non-consensus call

Consensus says the next 12 to 18 months are about whether tokenization is legal. That question is mostly answered. The real sequence is different: first, which tokenized claims qualify as institutional collateral; then, which sovereigns and platforms control the distribution of strategic assets. The money-layer fight — the GENIUS Act, the BIS unified ledger, Project Agorá — is loud and nearly settled. The asset-layer fight is quiet and wide open. That is where the next institutional advantage sits.

So the owner’s move is not to size a speculative crypto bucket. Before the next investment-committee meeting, the more useful exercise is to map which assets already in the portfolio could be financed, collateralized or marked on someone else’s rails within three years — and to decide, asset by asset, whether to be a price-taker on those rails or a part-owner of them.

Stablecoins are the decoy. They are the visible fight because they look like money. The larger prize is the programmable asset layer — the rails through which sovereign debt, infrastructure, private credit, real estate, energy and collateral will be issued, financed and moved. Whoever controls that layer will not merely process transactions; they will shape access, liquidity, pricing and control. That is why this belongs in the boardroom, not the crypto allocation memo. The rate sheet does not price it yet. The owners who act before it does will set the terms for those who wait.

Sources: BIS, Annual Economic Report 2026, Chapter III and accompanying release; BIS, Project Agorá advances to real-value testing; Bank of Canada joins Project Agorá; FinCEN, GENIUS Act customer-identification proposed rule; U.S. Treasury, FinCEN/OFAC AML & sanctions proposed rule; PIF 2026–2030 strategy; Tether Q1 2026 attestation; CoinDesk on tokenized Treasuries.

Naveed Iqbal is a Contributing Journalist at Universal Asset Owners covering digital assets, Web3 infrastructure and the intersection of crypto markets with institutional capital.