For two years the AI build-out has been an equity story — a thing universal owners owned, through their Nvidia and hyperscaler weights, and mostly enjoyed. This week it changed shape. The same build-out is now a credit story: a thing allocators finance, through investment-grade bonds, private credit and a thickening layer of special-purpose vehicles and lease-backs. On June 15, Nvidia sold its largest bond deal ever. Days earlier, the Bank for International Settlements and the Bank of England independently flagged the debt behind the build-out as a top-tier risk to the financial system. The denominator of the AI trade didn't change. The liability side did — and it landed on the universal owner's balance sheet.

1. The AI build-out has become a credit story — and central banks just called it systemic.

On June 15, Nvidia priced $25 billion of investment-grade bonds — its largest debt sale ever and its first since 2021 — drawing roughly $85 billion of orders (about 3.4× the deal) across seven tranches stretching to 2056. A company that has never needed to borrow now wants three decades of fixed-rate funding against the build-out.

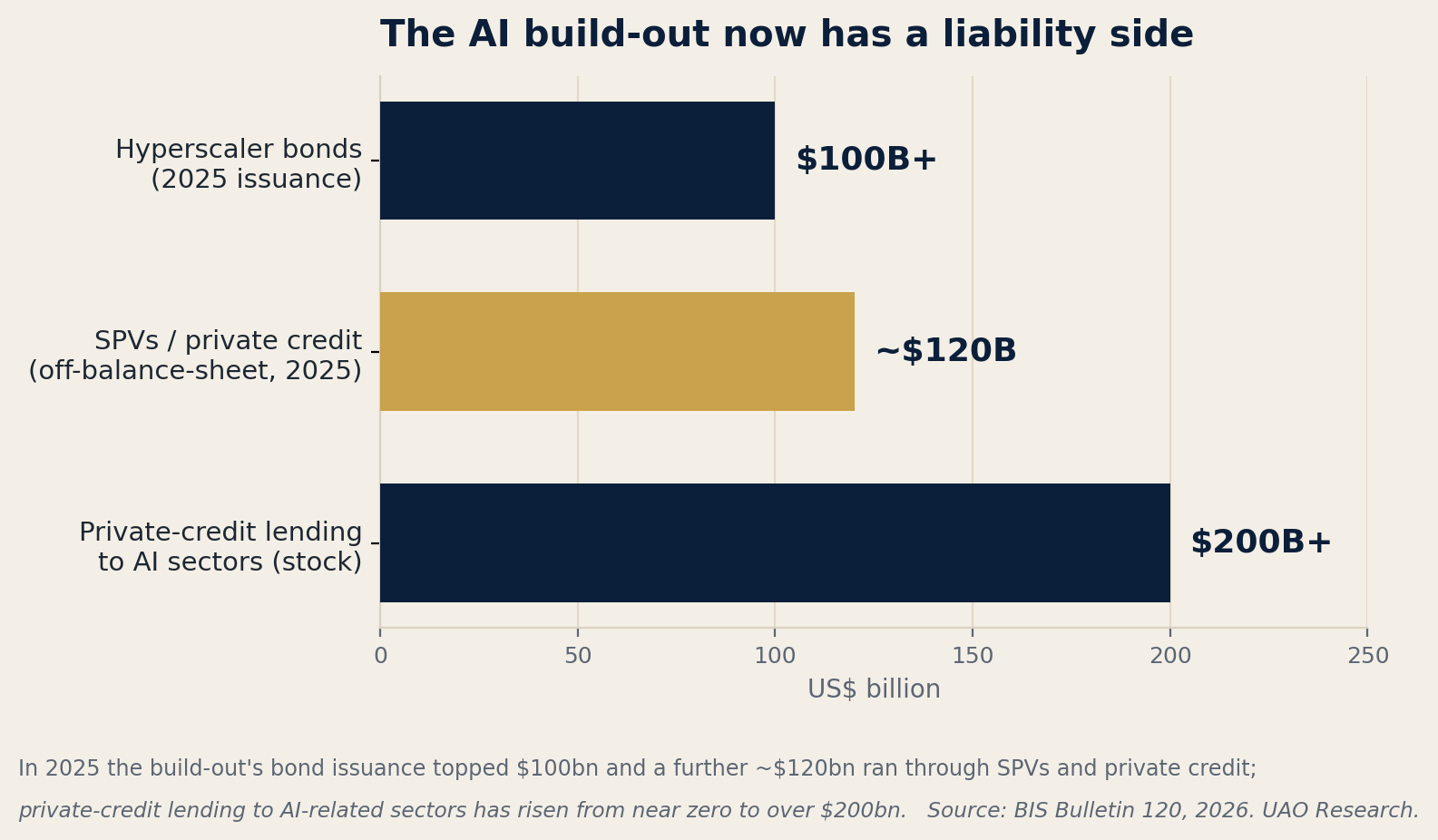

That deal is the visible tip. In Bulletin 120, "Financing the AI boom: from cash flows to debt," the BIS documents the shift: hyperscalers' bond issuance topped $100 billion in 2025, with roughly another $120 billion routed through SPVs and private-credit structures, while private-credit lending to AI-related sectors has gone from near zero to more than $200 billion. The Bank of England's Financial Policy Committee now names AI-equity valuations, private credit and sovereign debt as the three main sources of stability risk, noting that AI accounted for more than a third of private-credit deals in 2025, up from about 17% over the prior five years.

For a universal owner the point is not whether the AI thesis is right. It is that the exposure has migrated. You no longer only hold the build-out in your equity sleeve, where a drawdown is marked and survivable; you increasingly fund it in your fixed-income and private-credit sleeves, where the promise is a contractual cash flow and the failure mode is a default, a downgrade or a frozen vehicle. The fiduciary question for the next allocation meeting is blunt: are your credit managers underwriting AI cash flows, or AI hope?

Source: BIS Bulletin 120, 2026; Bloomberg / SEC Form 424B5 (Nvidia), June 15, 2026; Bank of England Financial Policy Committee via Central Banking and Reuters, 2026.

2. The same build-out has a second front — minerals — and China just restricted it again.

On Monday, June 22, China's Commerce Ministry added MP Materials and USA Rare Earth — alongside eight US entities it described as military-linked — to its export-control list, halting Chinese dual-use exports to the two companies Washington has funded specifically to break American dependence on Chinese rare earths. China controls roughly 90% of global rare-earth processing; MP operates the only active rare-earth mine in the United States. The magnets these firms make are not a niche: they sit inside the motors, grid equipment and data-center cooling that the AI build-out physically depends on.

The owner's read is not "buy rare-earth miners." It is that supply-chain concentration is a fiduciary-relevant systemic risk, not a sector trade — a single-country dependency that can be switched off by decree, simultaneously, across defense, semiconductors, grids and data centers. The actionable lever is stewardship: press portfolio companies to disclose single-country input dependency and credible substitution plans, the way you would press them on leverage or refinancing walls.

Source: Reuters (via Investing.com) and Bloomberg, June 22, 2026.

3. Meanwhile the energy tail is deflating — don't chase the round-trip.

Oil opened the week near $78, up about 1.5% on lingering uncertainty over the Strait of Hormuz, but only after round-tripping the entire war premium — down roughly 8–10% on the week — as on-again, off-again US–Iran talks in Switzerland continued and Hormuz traffic recovered (US CENTCOM reported 55 merchant vessels and more than 17 million barrels transiting on Saturday alone).

A fading energy shock is disinflationary at the margin — welcome for liability discount rates. But it also removes a convenient hawkish excuse precisely as the AI-debt wave from item one has to be refinanced into what markets now price as a higher-for-longer regime: the ECB has hiked, the Bank of Japan has moved to 1.0%, and markets are pricing no Fed cuts in 2026. The disciplined posture is to treat the oil round-trip as regime-contingent, not as the all-clear — and to keep a modest chokepoint hedge until the technical talks actually conclude.

Source: CNBC, Al Jazeera and NPR, June 19–22, 2026; ECB and Bank of Japan policy statements, June 2026.

Capital Flow Watch — the sovereign-debt risk just went live in a G7 market

This morning UK Prime Minister Keir Starmer announced his resignation, triggering a Labour leadership contest (nominations open July 9; a new leader before Parliament returns in September), with Andy Burnham the frontrunner after his Makerfield by-election win. For universal owners this is not Westminster theatre — it is the sovereign-debt risk from the lead going live in a developed market: 30-year gilt yields sit near 5.54% and the 10-year near 4.845%, already elevated versus peers, while sterling slipped to about $1.319 (down roughly 3% since February). Political risk is repricing a G7 curve in real time — and it leaves the UK’s stewardship and pension-reform agenda (see Duty Watch) under a new and uncertain hand.

Sources: CNN; CBS News; PA/Yahoo Finance; CNBC, June 22, 2026.

Stewardship & Duty Watch. London Climate Action Week (June 22–28) opens with the PRI convening about 100 large asset owners for an Investor Day on June 23 built around system-level stewardship — climate engagement reframed not as values investing but as fiduciary risk management over a portfolio you cannot diversify out of. It lands on a widening trans-Atlantic fault line. In the US, 2026 Department of Labor guidance and a "financial-factors-only" posture have narrowed the latitude for ESG-motivated proxy voting inside ERISA plans; in the UK, the FRC's Stewardship Code 2026 builds stewardship into the definition of fiduciary duty. The universal owner — who by definition operates in both jurisdictions — now has to discharge a single duty under two incompatible legal readings of what that duty is — including whether pressing the AI-borrowers it lends to, to disclose refinancing risk, counts as fiduciary stewardship or off-limits ESG. (Sources: PRI; LSE Grantham Institute; Morgan Lewis and Mayer Brown on DOL guidance; FRC.)

Asset-Owner Moves. Northern LGPS completed its C-suite — John Dewey as CIO (from West Yorkshire Pension Fund; previously HSBC Alternatives), Sera Sadrettin as COO/CFO and Lorraine Solway as CRO — as the roughly £70bn UK pool stands up an FCA-regulated investment company, the consolidation-and-in-housing template in miniature (Professional Pensions, 12 June). In the Gulf, the template holds: PIF-backed Humain's framework for up to $1.2bn from the Saudi National Infrastructure Fund (around 250MW of AI data-center capacity), agreed at Davos in January, is sovereign capital underwriting sovereign AI infrastructure (Arab News). And Norway's NBIM remains barred from new ethics-based exclusions under temporary guidelines, with a framework-review committee due to report October 15 — the largest universal owner on earth with its stewardship machinery paused (NBIM; Chief Investment Officer).

What to watch. PRI Investor Day tomorrow (does collective climate stewardship survive as a fiduciary discipline?) · US–Iran technical talks and any OFAC sanctions-relief steps this week — don't front-run them · whether the AI-debt wave can refinance into a hawkish global cycle without spreads gapping · NBIM's ethics review (Oct 15).

Take (UAO Research). When you finance the future, you also underwrite it. The universal owner spent two years celebrating the AI build-out as an equity story it owned. The exposure has now moved onto the credit book, where a disappointment is no longer just a markdown — and that migration is already done.

Listen & watch

▶️ Today’s video brief — watch the presenter read the day → · 📄 Deep-dive — the universal owner is now the lender of the AI build-out →