Editorial analysis for institutional readers — not investment, legal or financial advice.

Private credit's first serious test may not come from office towers, consumer lenders, or an obvious recession trade.

It may come from software.

For much of the past decade, software looked like one of the safest places to lend to growth. Recurring revenue. High gross margins. Low capital intensity. Sticky enterprise customers. Private-equity sponsors with playbooks for pricing, cross-selling and cost discipline. For direct lenders it was close to ideal: a borrower base that could carry leverage, a sector that appeared less cyclical than industrials or consumer credit, and a story that fit the post-2008 retreat of the banks.

That trade has become far larger than most asset owners appreciate. The Bank for International Settlements estimates outstanding private-credit loans to software-as-a-service (SaaS) companies rose from about $8 billion in 2015 to more than $500 billion by the end of 2025 — roughly 19% of all direct loans. About a third of private-credit funds now hold SaaS exposure (BIS, 2026).

That is no longer a niche sector bet. It is a systemically important underwriting assumption sitting inside the asset class. And it is being tested at the exact moment AI is forcing a repricing of software business models. Public markets have already moved: the BIS notes software stocks fell almost 30% between October 2025 and February 2026, while business development company (BDC) share prices fell about 10% on average — and BDCs with heavier SaaS exposure underperformed lower-exposure peers by roughly five percentage points.

The question is not whether AI destroys software. It will not. The question is whether a large slice of private credit was underwritten against assumptions — durable pricing power, predictable renewals, high EBITDA conversion, attractive sponsor exits — that may no longer hold.

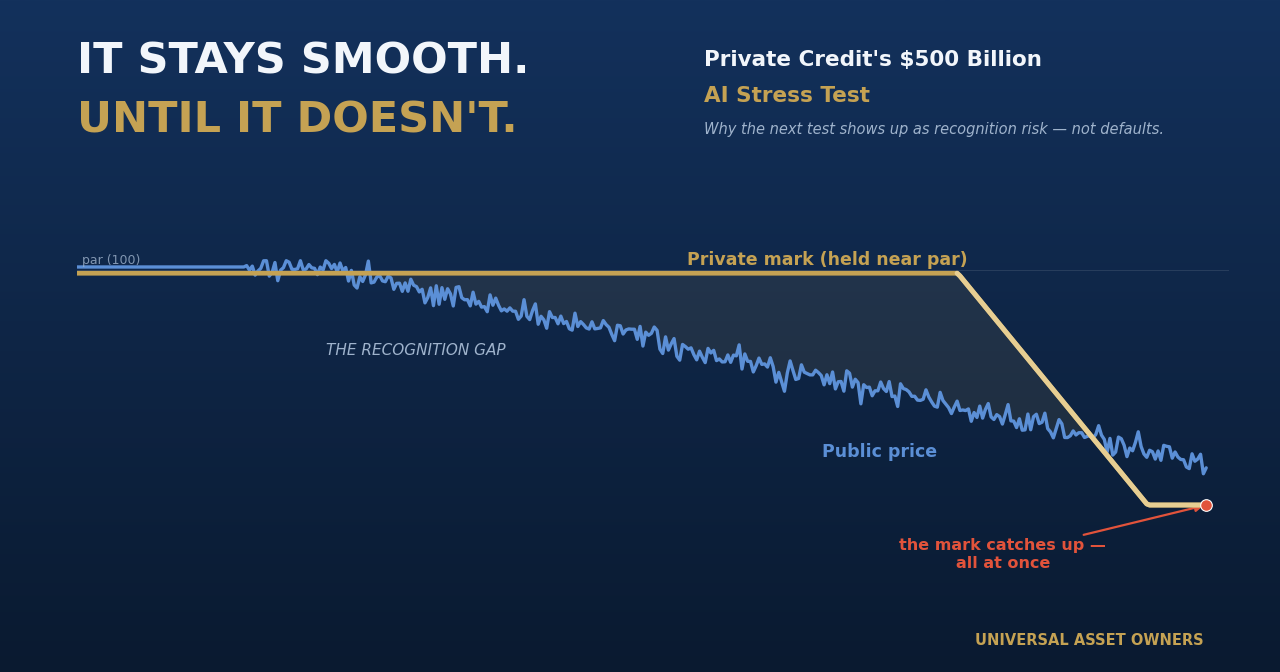

If those assumptions weaken, the risk will not show up first as a clean default statistic. It will show up as a lag. A borrower moves from cash interest to payment-in-kind (PIK). A lender holds a loan near par because the company has not technically defaulted. A fund reports a smooth net asset value (NAV) because no public price is forcing daily recognition. Investors keep receiving an attractive yield — until a restructuring, a redemption request, or a valuation review drags the mark into the open.

That is the real private-credit story now.

Not collapse. Not contagion. Not 2008.

Recognition risk.

Smooth Returns Can Hide a Business-Model Shock

Private credit became a core institutional allocation because it solved a real problem. Pensions, sovereign wealth funds, insurers, endowments and family offices needed yield. Banks were retreating from parts of middle-market lending. Public fixed income offered less income, more duration risk and more mark-to-market noise. Private credit offered floating-rate exposure, negotiated covenants, senior-secured structures, manager access and an illiquidity premium that looked attractive for patient capital.

But the same features that make private credit attractive can delay the recognition of stress. Public credit reprices in minutes. Private credit reprices through manager marks, valuation committees, amendments, restructurings and eventual exits. That is not wrong — illiquid assets should not be marked as if they trade every second. But it means the reported number is partly an economic judgment and partly a governance process.

Software is where that distinction now bites. A public SaaS company can be repriced in a day if investors believe AI will compress margins or erode seat-based demand. A private SaaS borrower moves far more slowly through the system. Its debt may still pay. Its sponsor may still support it. Its lender may still believe it has value. Its mark may not move much until a transaction, a refinancing, a covenant breach or a sale forces the question.

That is why software is a sharper lens than "private credit" as a generic debate. The issue is not whether direct lending is good or bad. It is whether portfolios have concentrated exposure to a sector whose core economics are being re-underwritten in real time.

Defaults Are Not Yet the Story — and That Is the Point

The strongest argument against alarm is simple: default rates remain contained. Proskauer's Private Credit Default Index reported a default rate of 2.73% in Q1 2026, up from 2.46% in Q4 2025 and 1.84% in Q3 2025 — a deterioration, not a crisis, and one in which software and technology defaults stayed relatively stable despite the market noise (Proskauer, 2026).

A credible analysis should not pretend the asset class is breaking when the evidence does not show it. The subtler truth is that defaults are a lagging indicator in a market where many of the important risks are designed to lag. A loan paying interest in kind is not in default. An amended loan is not necessarily impaired. A loan held near par is not visibly distressed. A fund meeting redemptions up to its cap is not failing.

But for a universal owner, "it has not defaulted" is not the same as "the original underwriting case is intact." In software, if revenue growth slows, gross retention weakens, acquisition costs rise, or AI-native competitors force price compression, the capital structure can become fragile well before a default appears. The first signals are amendments, PIK toggles, covenant relief, delayed refinancings, widening discounts to NAV, and a growing gap between public valuations and private marks. That is the warning system to watch.

The Public Market Is Already Voting

BDCs are not the whole private-credit market, but they are one of the few places where private-credit assets get repriced by public investors. According to the BIS, BDCs extended more than 15% of their loans to SaaS firms in 2025, and higher-SaaS-exposure BDCs have already traded worse than their peers.

The lesson is not that public BDC prices are always right and private marks always wrong. It is that public investors are applying a software discount faster than private portfolios are likely to recognize it. That gap can persist, and can even be rational — a lender with security, covenants and sponsor support should not mark a loan like a public equity. But if the equity repricing reflects a genuine change in business quality rather than sentiment, the private mark eventually has to catch up.

The timing is the risk.

How Quickly the Lag Can Collapse

The market has already seen what a recognition event looks like. In January 2026, BlackRock TCP Capital disclosed a roughly 19% quarter-over-quarter decline in NAV per share, with management attributing about two-thirds of the drop to a small group of long-standing challenged companies and the rest to broader markdowns; non-accruals were set to rise and leverage moved above target (BlackRock TCP Capital, Form 8-K, 2026).

One fund does not define an asset class — TCP had its own portfolio issues, many in vintages underwritten in 2021 or earlier. But it is a clean case study in how stress becomes visible. The reported decline did not mean the economic deterioration happened in one quarter. It meant the accounting recognition happened in one quarter. Private credit can look stable until it does not. The absence of volatility is not always the absence of risk; sometimes it is the accumulation of risk behind a valuation process that moves in steps rather than ticks.

The Semi-Liquid Wrapper Changes the Risk

Traditional institutional private credit is often closed-end — which is precisely why managers argue it is less prone to forced selling than open-ended public funds. If investors cannot redeem tomorrow, managers are not forced to sell tomorrow. But private credit is no longer only a closed-end institutional product. It has been pushed into non-traded BDCs, interval funds, perpetual-life vehicles and wealth channels offering periodic liquidity, usually with quarterly redemption caps.

In Q1 2026 that bridge came under pressure. Stanger reported that quarterly redemptions exceeded fundraising for the first time in the non-listed BDC market: sponsors met about $6.9 billion of redemption requests while publicly registered BDCs raised $4.9 billion in new capital, and several funds filled requests only up to their caps and prorated the rest (Stanger, 2026).

Stanger was explicit that the structures functioned as designed. But from an asset-owner seat, that is the point. "Functioning as designed" can still mean investors do not get all their money back when they ask — and that realized asset sales become the first real market test of NAV marks. The danger is not that every semi-liquid fund gates. It is that investors begin to treat capped liquidity as uncertain liquidity, and that uncertainty changes behavior across the sector.

Insurers Are the Balance-Sheet Transmission Channel

For sovereign funds and pensions, private credit is a portfolio allocation. For insurers, it can become a balance-sheet and capital-regime issue — and that distinction is now central. Moody's warned that US life insurers' private and illiquid fixed-income holdings grew to roughly $807 billion by year-end 2025, about 20% of the industry's fixed-income portfolio. The top 10 insurers held 44% of that exposure — about $352 billion — despite accounting for only ~24% of total industry fixed income, with a weaker credit-quality profile and PIK flagged as a warning signal (Moody's, via Bloomberg, June 2026).

Regulators are responding. Beginning with 2026 reporting, the NAIC is requiring more granular disclosure on private placements and complex investments — fair value, Level 2 and Level 3 exposure, PIK interest and private-letter ratings — and is increasing scrutiny of assets whose economic substance may not match their regulatory treatment.

This should matter to universal owners even if they are not insurers. Many sovereign funds, pensions and family offices have exposure to the same managers, sponsors, borrowers, private placements, asset-backed structures and reinsurance channels; some allocate to insurance-linked platforms or to asset managers that own insurers. The FSB has warned that the links among private-credit funds, banks, insurers and private equity are deepening. The risk is not sealed inside a single sleeve called "private credit." It can travel through insurers, asset-backed finance, NAV lending, subscription lines, sponsors and bank financing lines.

The Skeptics Are Partly Right

There is a lazy version of the private-credit critique — that the whole market is shadow banking waiting to blow up. The evidence does not support it. Senior direct lending can be safer than many public alternatives when it is conservatively structured, properly covenanted and run by disciplined lenders. Private managers often know borrowers better than public bondholders. Many loans are floating-rate, senior-secured and closely monitored. Closed-end structures reduce forced selling. Institutional LPs are more patient than retail.

Recent high-profile failures such as First Brands and Tricolor need care, too. They exposed real governance and underwriting problems — off-balance-sheet financing, complex intercreditor exposures, allegations of fraud — but they are warnings about opacity and diligence, not proof of universal impairment. The strongest managers may emerge from this cycle stronger: lending at wider spreads, demanding better covenants, avoiding crowded software credits and buying from forced sellers.

That is exactly why the answer is not a blanket rejection of private credit. It is discrimination. The asset-class average is becoming less useful; the dispersion between managers, structures, vintages, sectors and investor bases now matters more than the headline default rate.

What Boards and Investment Committees Should Ask Now

The most important diligence questions in 2026 are no longer mainly about yield, spread and loss history. They are about recognition:

- PIK and amendments: How much portfolio income is cash interest versus PIK, and how has that changed over six quarters? Which borrowers moved from cash-pay to PIK, and why? What share has been amended, extended or restructured without moving to non-accrual?

- Hidden software exposure: How much sits in software, SaaS, IT services, digital infrastructure, data-center-adjacent and AI-exposed models — and not just by industry label? A "business services" or "healthcare technology" borrower may still sell software-like recurring contracts.

- Stress sensitivity: What happens to debt-service coverage if EBITDA falls 10%, 20% or 30% — and does that scenario assume margin pressure, churn, slower bookings, lower exit multiples, or all four?

- Who sets the marks: How often do independent valuation firms challenge them, how many positions are Level 3, and how much NAV change comes from assumption changes rather than actual transactions?

- Liquidity company you keep: Does the fund have redemption features, who else is in the vehicle, what share of the base is retail or wealth-channel capital, and are you structurally exposed to liquidity decisions made because other investors want out?

- Cross-wrapper overlap: Has the manager or sponsor lent to the same borrower through multiple vehicles? Do affiliated insurers hold related exposures? Are banks financing the fund, the borrower, or other investors in the same credit?

Where This Goes Next

The base case is not a crisis. Defaults keep rising gradually but stay contained. AI disrupts some software borrowers without destroying the sector. Stronger managers amend, restructure and work through challenged credits. Semi-liquid vehicles use caps as intended. Regulators tighten disclosure without forcing a disorderly repricing. In that world private credit keeps its place — but the return premium narrows and manager selection matters far more.

The downside case begins with software: a larger group of SaaS borrowers misses plan, sponsors stop supporting weaker companies, PIK rises, NAV discounts widen, redemptions persist in non-traded vehicles, managers grow reluctant to realize losses, and asset sales then become valuation events for the whole market. The problem there is not a wave of defaults. It is a repricing of confidence.

The insurance case is slower but potentially more consequential: if regulators conclude that private placements, private ratings or asset-backed structures are getting too favorable a capital treatment, the economics of holding private credit on insurance balance sheets can change — reducing marginal demand from one of the market's most important buyers.

The tail case is a cross-wrapper recognition event: a major sponsor-backed borrower fails, several lenders discover less collateral protection than assumed, related exposures surface across BDCs, private funds, insurers and bank lines, and managers with no direct exposure are forced to defend their marks because investors no longer trust the valuation process. That is the event the market is not priced for — not credit loss alone, but valuation contagion.

The Bottom Line for Universal Owners

Private credit is not broken. But the easy version of the story is over. For years it was sold as extra yield without public-market volatility. That was never the full truth: private credit reduces visible volatility. It does not eliminate economic volatility. It delays it, smooths it, and then recognizes it through discrete valuation events.

That matters more now because the market is larger, more interconnected, more exposed to retail liquidity, more important to insurers and more concentrated in business models being repriced by AI. The most important fact in private credit today is not the default rate. It is the $500 billion-plus of SaaS exposure sitting inside a market whose valuation process was built for private negotiation, not rapid technological disruption.

Universal owners do not need to flee the asset class. They need to underwrite it differently. The question is no longer "Does private credit deliver yield?" It does. The question is whether that yield is being earned for true illiquidity — or whether part of it is compensation for delayed recognition, hidden sector concentration and governance complexity that will only become visible when capital is hardest to move.

That is the first real test. And software is where to look first.

Source notes

- Bank for International Settlements, Private credit's software lending meets AI disruption, BIS Quarterly Review, March 2026: SaaS private-credit loans up from ~$8bn (2015) to >$500bn (end-2025), ~19% of direct loans; software equities -30% and BDCs -10% Oct 2025-Feb 2026. bis.org

- Proskauer, Private Credit Default Index, Q1 2026: default rate 2.73% (vs 2.46% Q4 2025, 1.84% Q3 2025); software/tech defaults relatively stable. proskauer.com

- BlackRock TCP Capital, Form 8-K / NAV disclosure, January 2026: ~19% QoQ NAV decline; ~two-thirds from a small group of challenged credits; rising non-accruals. sec.gov

- Moody's, US life insurers' private/illiquid fixed income, reported June 2026: ~$807bn at year-end 2025 (~20% of fixed income); top 10 insurers 44% (~$352bn); PIK flagged. Bloomberg

- Stanger, non-listed BDC flows, Q1 2026: redemptions (~$6.9bn) exceeded fundraising (~$4.9bn) for the first time; several funds prorated at caps. rastanger.com

- NAIC: 2026 reporting changes requiring granular disclosure on private placements, Level 2/3 exposure, PIK interest and private-letter ratings; KBRA and FSB commentary on interconnections referenced throughout.