The sovereign balance sheet becomes the binding constraint

NATO's 5%-of-GDP defense-investment commitment and the OBR's unsustainable-debt warning converge with the Hormuz oil shock on one of a universal owner's least-diversifiable exposures: long-dated government debt.

UAO EditorialJuly 9, 202610 min read

Universal Asset Owners

The UAO Daily Brief

Volume 1, Issue 56 • Thursday, July 9, 2026 • 7:00 am ET / 15:00 GST

Two forces a universal owner cannot diversify away reasserted themselves in the last 48 hours. The physical economy — chokepoints, oil, diesel, grids and power — kept the inflation impulse alive as the Strait of Hormuz remained a severe shipping risk. At the same time, the sovereign balance sheet moved back to the center of the portfolio: NATO's Ankara summit reaffirmed the alliance's 5%-of-GDP defense-investment track and pledged at least €70bn in Ukraine-related military support, while Britain's fiscal watchdog warned that in nearly all of its long-run scenarios, public debt eventually moves onto an unsustainable, ever-rising path. These are not separate stories. They converge on the asset long-horizon owners hold most, hedge with most, and can least avoid: long-dated government debt. Today's question is not whether oil rose, defense spending increased, or power demand hit another record — it is whether the portfolio's traditional risk-free anchor is absorbing fiscal, energy and geopolitical risk at the same time.

• NATO Ankara Summit Declaration — 5%-of-GDP track, €70bn for Ukraine — NATO

• OBR, Fiscal Risks and Sustainability, July 2026 — debt on an unsustainable, ever-rising path — OBR

• US power demand to hit records in 2026–27 as AI surges — Reuters / EIA

Today's Intelligence — Top Stories

1. The sovereign balance sheet becomes the binding constraint.

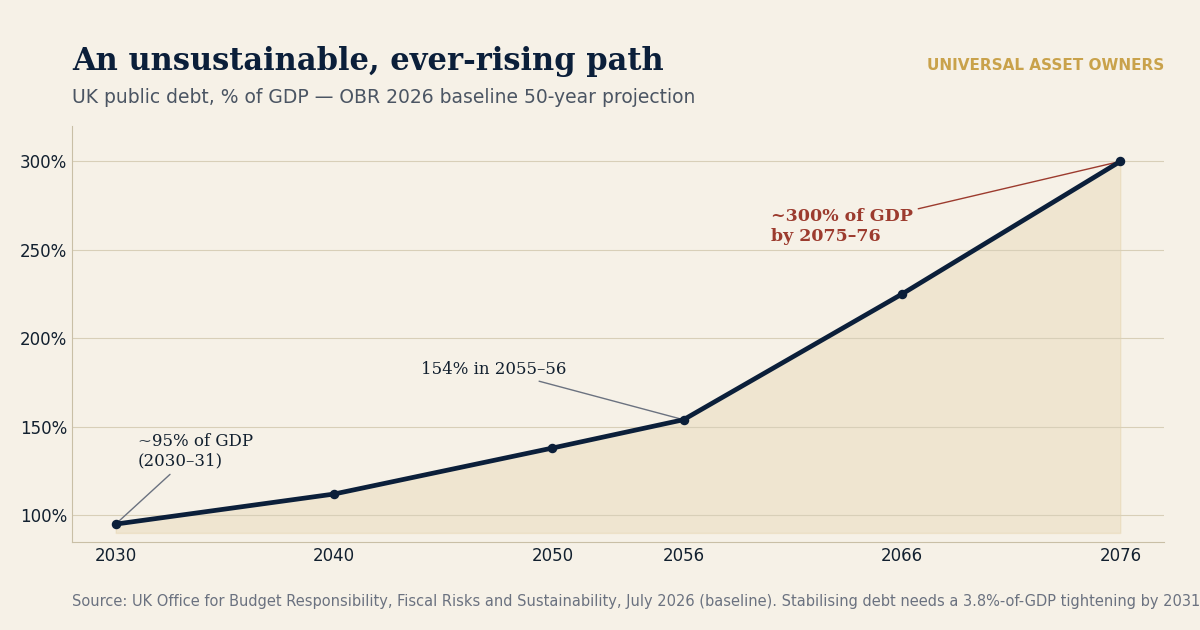

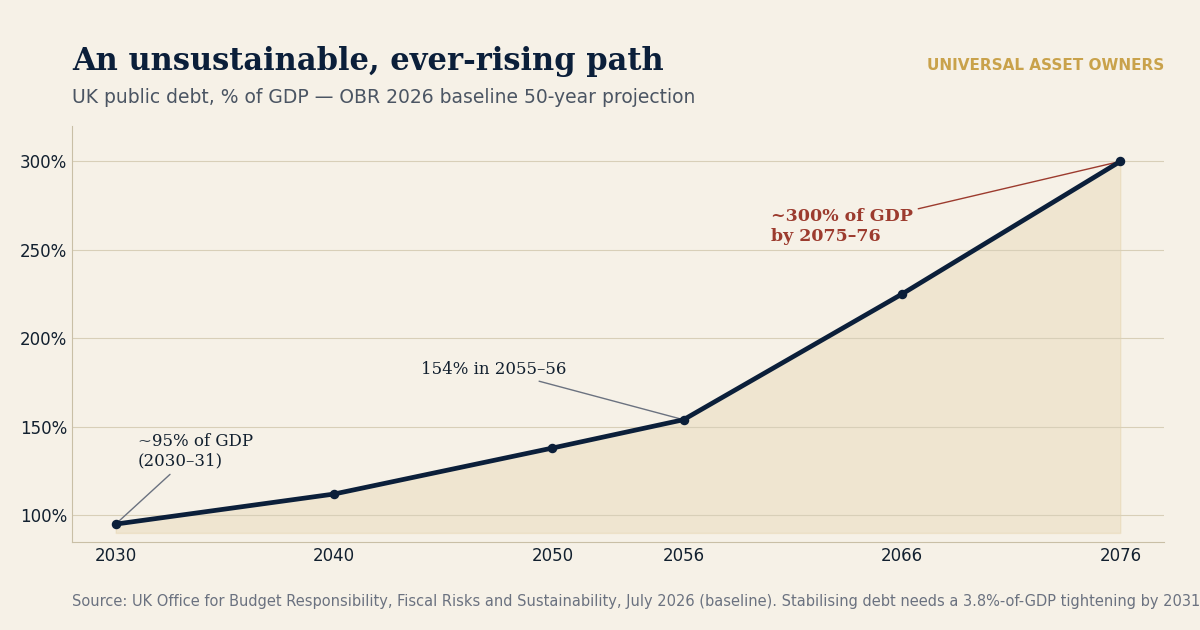

Two of the most consequential documents of the year landed within 24 hours of each other. On July 8 the NATO Ankara Summit Declaration committed allies to at least €70bn in military assistance to Ukraine this year, more than $50bn in new collective procurement, and reaffirmed the 5%-of-GDP defense-investment track by 2035 (3.5% core plus 1.5% resilience). NATO said European allies and Canada increased defense expenditure sharply in 2025, and pledged at least equivalent levels of Ukraine support in 2027. NATO, Jul 8. The day before, the UK's Office for Budget Responsibility published its 2026 Fiscal Risks and Sustainability report, warning that in nearly all of its long-run scenarios UK debt eventually moves onto "an unsustainable and ever-rising path" — from ~95% of GDP in 2030–31, past 154% in 2055–56 and toward ~300% by 2075–76 under the baseline — and that stabilising it would need a permanent 3.8%-of-GDP primary-balance tightening by 2031/32, roughly the entire education budget. (The OBR stresses these are scenarios, not forecasts.) OBR, Jul 7.

Implication for owners. One of a universal owner's largest and least-diversifiable exposures is long-dated government debt. Put a politically and diplomatically anchored 5%-of-GDP defense track on top of aging demographics, health-cost escalation and climate spending, with independent watchdogs already calling debt unsustainable, and the interaction is what matters: it accelerates the timeline to fiscal tipping points and raises the risk of explicit trade-offs among defense, pensions, healthcare, climate adaptation and debt service. The OBR is not a UK curiosity — it is one of the G7's most detailed independent fiscal-watchdog exercises and a template for what independent bodies will eventually say about France, Japan, Italy and the United States. For LDI pension books, insurers holding long paper, and sovereign funds with large fixed-income sleeves, this is a strategic-asset-allocation question, not a headline.

2. Hormuz keeps the inflation impulse alive — which is why the fiscal math bites now.

The Strait of Hormuz stayed contested through July 7–8. After the US said Iran had struck commercial vessels in the Strait, Washington launched retaliatory strikes and revoked Iran's oil-sales permit; transit risk was rated "severe," and traffic through the strait fell to about 16 vessels on Tuesday, versus a pre-conflict norm of roughly 125 a day. Al Jazeera, Jul 8.AP, Jul 9. Brent remained volatile in the high-$70s, and long-dated government bond yields pushed higher as the shock met an already-elevated inflation backdrop. EIA STEO.

Implication for owners. This is the wire that connects story one to the whole portfolio. A fresh energy-inflation impulse — the June NY Fed survey put one-year inflation expectations at 3.7% (three-year 3.3%), among the highest in years — reduces the room for a synchronized global cutting cycle, and some central banks are already moving the other way: on July 8 the Reserve Bank of New Zealand raised its cash rate 25bp to 2.50%, its first hike in three years. Bloomberg, Jul 8. Higher-for-longer long yields are exactly the mechanism that turns the OBR's unsustainable path from a 2070s projection into a present-day discount-rate problem for every long-duration asset an owner holds.

3. The physical economy is now a power-and-grid imperative — inflationary before it is productive.

The EIA's July 7 Short-Term Energy Outlook projected record US electricity demand — 4,269 billion kWh in 2026 and 4,399 in 2027 — with commercial demand expected to exceed residential in 2026, for the first time on record, driven by AI data centers and electrification. Reuters / EIA, Jul 7. The build-out is landing as physical infrastructure: Meta unveiled a C$13bn data center in Alberta, a 1 GW facility scalable to 1.8 GW, tied to new gas-fired generation. Meanwhile Russia's July 8 diesel export ban and Ukraine's refinery-strike campaign tightened refined products — and diesel, the fuel of logistics, agriculture and construction, can transmit into freight, food and industrial costs faster than a move in crude.

Implication for owners. The AI build-out is no longer a software story; it is a power, gas, grid, water and permitting story — and it competes for the same scarce grid capacity as everything else. With interconnection queues running 5+ years, grid access becomes the scarce asset, commanding a premium for behind-the-meter nuclear, contracted gas and stranded sites with existing connections. The uncomfortable corollary for the macro book: AI capex may be inflationary before it is productivity-enhancing, adding demand for power, equipment, land and labour years before measured productivity gains appear — reinforcing exactly the sticky-inflation dynamic in story two.

What an owner should test this week

Long-duration sovereign bonds — run a +100–150bp term-premium shock. Fiscal, defense and inflation risks are loading onto the same instrument.

LDI / liability hedges — stress a higher-for-longer path plus collateral calls. The 2022 UK gilt lesson still applies.

Infrastructure / grid assets — price a grid-connection scarcity premium. Existing power access may outvalue generic data-center exposure.

Energy & logistics — test diesel, LNG and Hormuz-disruption sensitivity. Refined-product stress can hit inflation before crude does.

Private markets — re-check exit and liquidity assumptions under higher discount rates. Duration risk is embedded in infra, real estate, private credit and growth equity.

Policy & Capital Flow Watch

• Sovereign capital architecture is expanding. Kenya's president signed the Sovereign Wealth Fund Bill into law on July 8, creating a three-pillar structure — a future-generations "Urithi" fund, a stabilisation fund and a national-infrastructure fund — with 30% of petroleum and mineral revenues reserved for future generations. Canada announced its C$25bn Canada Strong Fund in April. A new marginal buyer of global infrastructure is forming. Ground News.

• Trade: The US declined on July 1 to renew USMCA in its current form, but the $1.8tn agreement remains in force while the parties negotiate — enough to raise the political-risk premium on North American manufacturing, energy and critical-minerals investment. Reuters.

• Oil: OPEC+ approved a 188,000 bpd August quota increase on July 5 — a plan set before the latest Hormuz re-escalation changed the risk premium.

Research note — the hidden correlation

The sovereign-bond squeeze is one trade, not three

Connect the wires from this week. A Hormuz shock keeps energy costs and inflation expectations elevated; the AI-and-power build-out adds to that demand; central banks therefore have less room to cut; and into that higher-for-longer rate regime, NATO members are committing to a 5%-of-GDP defense track while their own watchdogs call debt unsustainable. Every strand loads the same instrument — long-dated government debt, the universal owner's largest and least-diversifiable holding. The risk is not any single headline; it is that fiscal, energy and geopolitical pressures are correlated on the one asset most portfolios assume is the diversifier. That, not the day's oil print, is the universal-owner story.

Allocator Radar — who moved capital in the last week

• Pension capital is following the infrastructure corridor. AustralianSuper committed a further A$500m to India's National Investment and Infrastructure Fund (now A$3.3bn in India), alongside the first-ever bilateral Australia–India uranium supply agreement, signed July 8, feeding India's 100 GW-by-2047 nuclear plan.

• Public capital is funding the physical layer of AI. CPP Investments committed US$1.75bn (C$2.4bn) to EQT's AI-infrastructure strategy (EdgeConneX; 10+ GW of data-centre capacity) — underwriting power and compute, not just data-centre equity. Bloomberg.

• Gulf capital is buying India's financial rails. Gulf SWFs deployed a record $53.9bn across 108 deals in H1, and ADIA and GIC are anchoring the IPO of India's SBI Funds Management (~$12.1bn valuation, opening July 14) — a sovereign bet on institutionalising India's domestic capital markets, not just picking its stocks. The National.

The Big Picture

The physical economy and the sovereign balance sheet are back as the binding constraints

For most of the past decade, the physical systems underneath portfolios — shipping lanes, gas basins, grids, refineries — were treated as shock absorbers, and government debt as the risk-free anchor. This week reversed both assumptions. The IMF's July update cut global growth to 3.0%, raised its inflation forecast, said disinflation has stalled, and — notably for this audience — flagged "potential corrections in market expectations for AI" as an explicit downside risk in a live forecast. Sovereign investors are responding in kind: Invesco's 2026 study finds infrastructure now 9.0% of sovereign assets (up from 4.9% in 2022), and CPP Investments has built a four-scenario "deglobalisation radar" with Oxford to treat fragmentation as investable rather than merely hedged. The through-line: from generic diversification to explicit geopolitical and fiscal portfolio design.

From the research desk — this week's institutional reading

• OBR, Fiscal Risks and Sustainability (Jul 7) — UK debt on an unsustainable path in nearly all scenarios; 3.8%-of-GDP tightening needed by 2031/32. OBR.

• NATO, Ankara Summit Declaration (Jul 8) — 5%-of-GDP track by 2035; €70bn for Ukraine; resilience and industrial-base commitments. NATO.

• IMF, World Economic Outlook Update (Jul 8) — global growth trimmed to 3.0%, disinflation stalled, and AI-valuation correction flagged as a downside risk. IMF.

• EIA, Short-Term Energy Outlook (Jul 7) — record US power demand through 2027; Hormuz supply-disruption scenarios. EIA.

Chart of the day

Source: UK Office for Budget Responsibility, Fiscal Risks and Sustainability, July 2026 (baseline scenario; OBR notes these are scenarios, not forecasts). Stabilising debt would require a 3.8%-of-GDP primary-balance tightening by 2031/32.

Scenario Lab — today

The Sovereign Debt Squeeze

Trace the chain: a 5%-of-GDP defense track → demographic and health-cost escalation → sticky energy-driven inflation that keeps rates high → higher-for-longer long yields → LDI and pension-book stress → a government forced to choose between defense commitments and pension obligations.

Deep dive — The physical economy reasserts itself, and so does the sovereign balance sheet

The question. For a decade, two things were treated as background: the physical systems beneath the economy, and the government bond as the portfolio's risk-free anchor. The past 48 hours put both in the foreground at once. The question for a universal owner is whether these are temporary shocks to ride out, or a regime change to design around.

Why it is structural. A sovereign fund, pension plan or insurer can rotate between sectors, but it cannot rotate away from energy inflation, grid scarcity, chokepoint risk or an unsustainable sovereign debt path if those forces move through the whole market. Hormuz is a reliability discount on a fifth of the world's oil and gas, not a one-day price move. The AI build-out is a claim on power, gas and grid capacity that competes with everyone else's — inflationary before it is productive. And the fiscal side compounds it: NATO's 5%-of-GDP track is a multi-decade allocation of sovereign balance-sheet capacity at the exact moment the OBR — one of the G7's most detailed independent fiscal-watchdog exercises — says the existing trajectory is unsustainable in nearly all scenarios. These are not diversifiable risks; they are the system.

The convergence. The strands are correlated on one instrument. Sticky energy inflation keeps policy rates from falling; higher-for-longer long yields raise the cost of the defense-and-demographics bill; that bill is being locked in as debt watchdogs flash red; and the discount rate that reprices every long-duration asset an owner holds rises with it. The bond market has not fully priced the interaction of binding defense tracks, demographic pressure and a stalled disinflation. The most under-discussed second-order effect is crowding out — defense commitments and rising debt service compete directly with the fiscal space for pension contributions, climate adaptation and infrastructure maintenance.

Allocator posture. Treat long-dated sovereign debt as a factor with fiscal and geopolitical loadings, not as the neutral anchor. Stress LDI and liability-matching books against a higher-for-longer path and a steeper term premium. Price grid access and existing power connections as scarce, ownable assets. Follow the sovereigns that are already redesigning — cutting generic listed equity toward infrastructure, real assets and explicit fragmentation hedges — rather than the ones still treating the physical economy as a temporary shock absorber. When you own the whole market, the job is not to beat it; it is to design for the constraints that are becoming binding.

Researched and edited by the UAO editorial desk. Figures trace to the named sources above. Where sources disagree — as they do on how fast fiscal pressure will bind — we say so rather than average them.