The instrument the market steers by is getting harder to read at exactly the wrong moment. US payrolls rose just 57,000 in June, April and May were revised down by 74,000 combined, and unemployment fell only because the workforce shrank. For a trader, that changes the next Fed screen. For a universal owner, it raises a larger problem: how do you govern a long-horizon portfolio when the signal arrives soft, gets revised softer, and then feeds into rates, currencies, infrastructure discount rates and benchmark pressure?

Below: revision risk; $29tn of sovereign capital rotating to resilience; a German grid turned into a new ownership model; private credit gating again; and why concentration is forcing a rethink of the benchmark itself.

1. June payrolls missed by half — and the revisions are the story

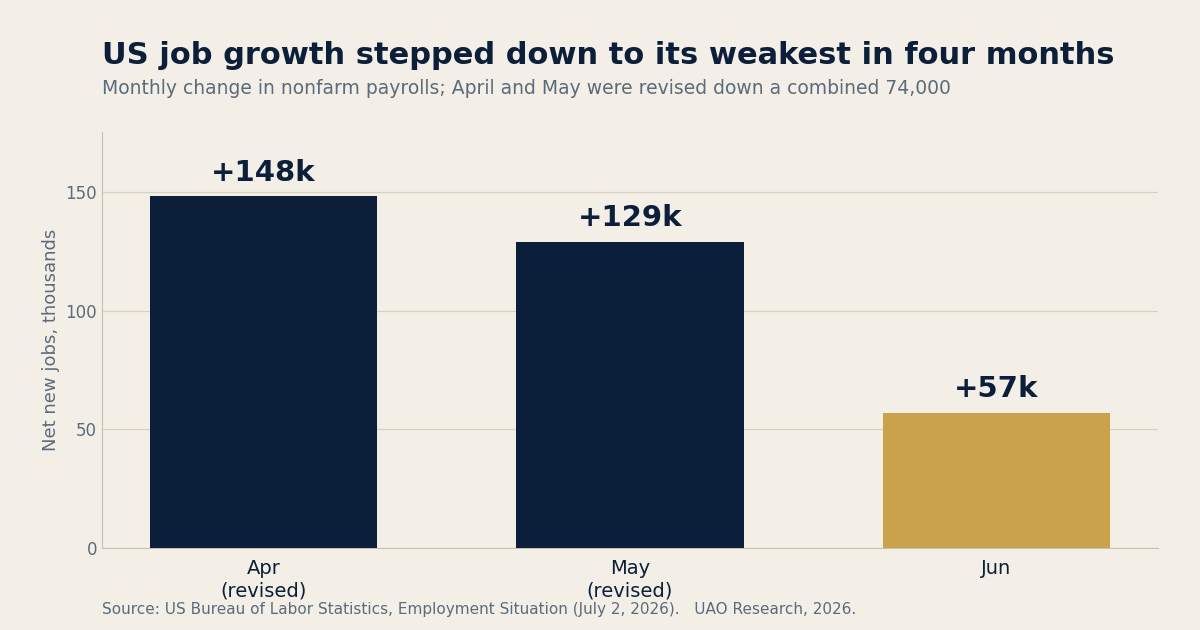

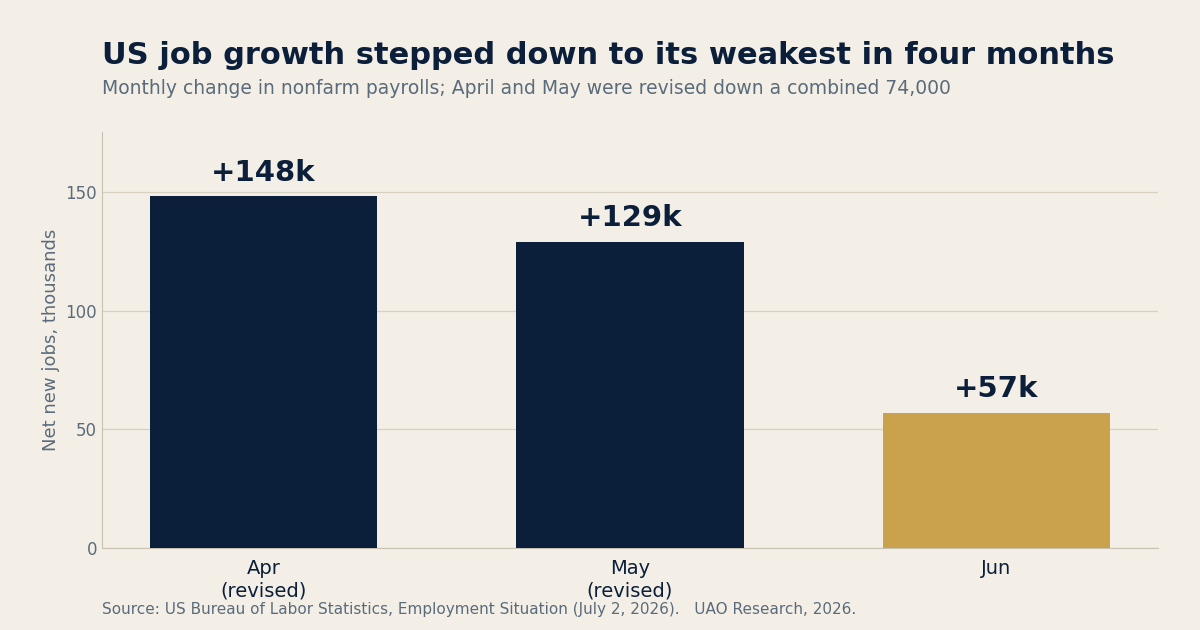

US nonfarm payrolls rose 57,000 in June, less than half the 115,000 consensus and the softest in four months (BLS, July 2, released a day early for the holiday). Unemployment fell to 4.2% only because participation dropped to 61.5% — the lowest since March 2021 — with the household survey showing 507,000 fewer people at work. Leisure and hospitality shed 61,000 jobs, striking with the FIFA World Cup being played on North American soil: that points to structural softness, not a seasonal wobble.

The number to underline is not 57,000 — it is 74,000, the combined downward revision to April (+179k→+148k) and May (+172k→+129k). The signal is not just decelerating; it arrives soft and is marked softer. The 2-year Treasury yield eased to 4.137% as traders priced out a near-term Fed hike. And on August 28 the BLS publishes its preliminary annual benchmark revision — a scheduled event that could restate the whole recent trend.

Implication for owners: You can hedge duration; you cannot hedge the quality of the data the Fed is reading. Position for the regime, not the print — and treat August 28 as a real portfolio date.

| Read the BLS release → |

Sources: BLS Employment Situation, July 2, 2026; CNBC, July 2, 2026.

2. Sovereign capital is rotating toward resilience — $29tn of it

If the signal is degrading, watch what the largest owners do anyway. Invesco’s 2026 Global Sovereign Asset Management Study — 144 institutions (90 sovereign wealth funds, 54 central banks) managing about $29tn — found a net 17% of sovereign funds planning to cut listed-equity exposure, while 28–35% intend to add private equity, private credit and infrastructure, and 65% now call private markets a key return driver.

The tell is infrastructure: now 9.0% of sovereign-fund assets, up from 4.9% in 2022 — the fastest-growing allocation of the past five years — with 80% naming energy security their most credible resilience play. Same instinct as the jobs read: when you cannot trust the short-horizon signal, you buy assets that pay you to wait.

Implication for owners: The marginal sovereign bid is moving from public equities to private markets and real assets. If you underwrite infrastructure or private credit, your co-investors and your competition increasingly answer to a state.

Sources: Invesco Global Sovereign Asset Management Study 2026, via Reuters/SCMP, June 29, 2026.

3. NBIM, GIC and APG are turning the German grid into a new ownership model

NBIM, GIC and APG have committed up to €9.5bn of new equity — staged through 2029 — for roughly 46% of TenneT Germany, operator of the country’s largest high-voltage network. NBIM’s own commitment is €4.5bn for 21.8%. State bank KfW is buying 25.1% for about €3.3bn; TenneT Holding retains at least 28.9%; GIC put the pre-money equity value at €10.4bn. Closing is subject to regulatory clearance, with prior guidance around the end of H1 2026.

The cap table is the template, not the cash flows: no single party holds majority control; the state (KfW) supplies political legitimacy; the sovereigns supply patient capital and governance discipline.

Implication for owners: Regulated transmission earns a return a regulator sets — a political variable, not a market one. The reserved-matter rights against a sovereign co-owner are the real investment; the inflation-linked cash flows are the easy part.

| Read NBIM’s statement → |

Sources: GIC / TenneT Holding, 2025–26; NBIM, 2025.

4. Private credit funds are gating redemptions again — the liquidity canary

While sovereigns rotate into private markets, the retail end is knocking to get out. Three of the largest retail private-credit funds capped withdrawals at the standard 5% after Q2 redemption requests surged: Apollo’s Debt Solutions saw 16.8% of shares (~$2.4bn) requested for exit; Ares’ $22.6bn Strategic Income Fund 14.4%, up from 11.6% in Q1; Morgan Stanley’s North Haven 10.9%.

Implication for owners: Retail is not the universal owner, but it is the canary. Pensions, insurers and sovereign funds are the largest LPs in the same asset class. Liquidity terms and mark discipline, not headline yield, are the covenants to reunderwrite now.

Sources: CNBC, June 23, 2026; Bloomberg, 2026.

5. Concentration — not a crash — is the risk they are hedging

In the Schroders Institutional Investor Study 2026, 39% of North American institutions said they are increasing active-management allocations specifically to reduce concentration risk — the most-cited reason — and 82% said active can help them meet objectives over the next 12–18 months.

Implication for owners: If you own the index, you own its concentration, and you cannot sell your way out without underperforming the benchmark you are judged against. The deeper question, live in the Invesco data too, is whether owners rethink the benchmark itself.

Sources: Schroders Institutional Investor Study 2026, via Benefits and Pensions Monitor, June 2026.

US job growth stepped down to its weakest in four months — and prior months keep getting revised lower.

Source: US Bureau of Labor Statistics, Employment Situation (July 2, 2026).

Why it matters: a labor market that was merely cooling would not keep getting marked down after the fact. The revisions, not the level, are the tell.

“The scariest line in the June jobs report is not 57,000 — it is the 74,000 that April and May lost to revision. A universal owner can survive a slow economy; what it cannot easily survive is a monetary authority forced to act on data that arrives soft and is then marked softer. Position for the regime, not the print — and mark August 28, when the benchmark revision could rewrite the whole picture.”

August 28 — the BLS benchmark revision. A large negative benchmark would validate the noisy-signal thesis with hard numbers.

The Fed’s September meeting. Do 57k payrolls and negative revisions make a cut live — or does 4.2% unemployment hold the Fed?

TenneT closing confirmation. A clean close sets the template for the next wave of European grid privatizations.

Concentration hedging — margin or structural? A 5% tilt or a 20%+ reallocation decides if this is a real shift or a survey answer.

Revision Risk: How Do You Govern a Portfolio on Data That Keeps Getting Revised?

The question. June payrolls rose just 57,000, but April and May were revised down by a combined 74,000, and on August 28 the BLS publishes a preliminary benchmark revision that could restate the whole trend. The live question for a long-horizon allocator is not guessing the next print — it is how to build a governance structure that stays resilient when the data itself cannot be fully trusted.

What the evidence says: a revision mirage, not a rigged system

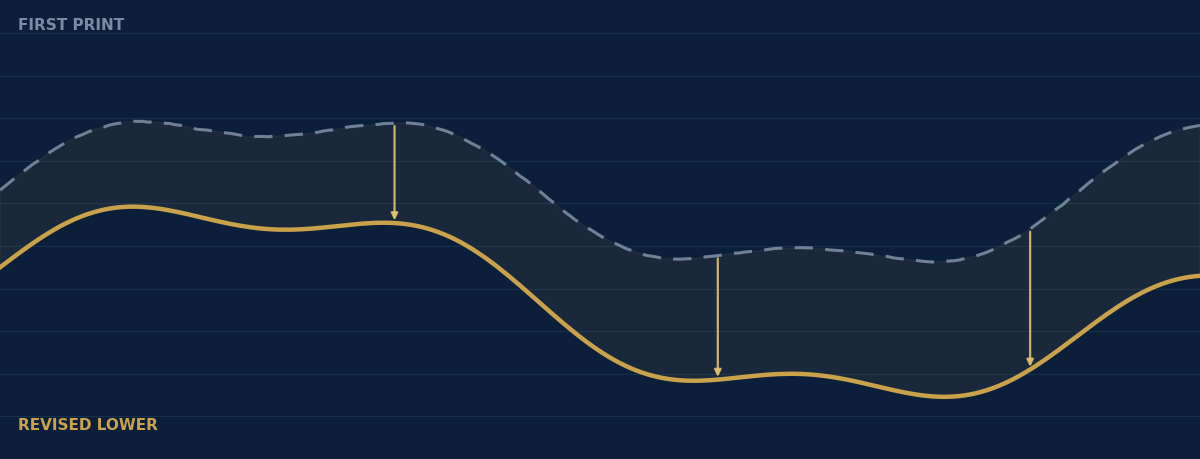

The swings are routine statistical convergence, not manipulation. The monthly establishment survey (CES) is a projection off an incomplete sample; it is later benchmarked to the near-universal administrative tax records of the Quarterly Census of Employment and Wages (QCEW). That is why the annual benchmark can move the count by hundreds of thousands in one stroke. What has changed is the noise: falling survey response rates, tighter agency budgets and a harder-to-measure services-and-tech economy make first prints increasingly revision-prone.

The academic warning is blunt, and it is not one paper. Athanasios Orphanides (Monetary Policy Rules Based on Real-Time Data, American Economic Review, 2001) showed that policy rules run on the data available at the time would have prescribed materially worse decisions than the same rules on revised data. Ghysels, Horan and Moench (Forecasting through the Rearview Mirror, Review of Financial Studies, 2018) showed the investing analogue: much of the documented ability of macro data to predict Treasury returns largely disappears when real-time (vintage) data is used instead of revised data, and the implied countercyclicality of term premia weakens with it. Revisions are serially correlated and make up a large share of the variance in macro series — so a model trained on finalized data is quietly using information no investor actually had. Rear-view-mirror modeling is dangerous for live capital.

Where it is contested

One camp reads genuine softening: three months of deceleration, four-year-low participation, hospitality shedding jobs during a home-soil World Cup. The other reads noise: 4.2% unemployment is low and wages are up 3.5%. Both cannot be fully right, and the data does not yet resolve it — which is why the August 28 benchmark matters more than any single headline. Where credible sources disagree, a universal owner should size for the uncertainty, not silently average it away.

From the allocator’s seat: a governance architecture, not a forecast

Because durable long-horizon macro forecasting is weak, the edge is not a better six-to-eighteen-month growth call — it is the operating system around the uncertainty. Five predefined moves:

1. Pre-commitment. Decide, in advance and in writing, what specific evidence will trigger an allocation change — the benchmark revision, a run of confirmed prints — not a single release. And keep expert human judgment in the loop to flag when a structural shift (manufacturing to services/tech) has made historical leading indicators obsolete.

2. Stress-test rates in both directions. The Fed is steering by the same noisy data, so hedge a policy mistake either way — too tight on a number later revised up, or easing into inflation on one later revised down. Pair long-volatility crisis protection with positive-carry real assets (TIPS, gold) rather than relying on stock-bond correlation that breaks in drawdowns.

3. Defend private marks. When public data whipsaws on revision, it injects noise into infrequently-marked private valuations. Advocate for conservative, slow-moving discount-rate and valuation assumptions that look past temporary statistical noise.

4. Standardize cross-portfolio benchmarking. Do not let short-horizon prints or benchmark pressure force hasty local optimizations. Use uniform evaluation protocols across the whole book so capital flows to the highest-return configuration, not the most persuasive local narrative.

5. Signals over stories — and interrogate the machine. Favor real-time, bottom-up signals (carry, trend, mean-reversion; regime-aware dynamic allocation; nowcasts built on alternative data) over a fragile top-down story — but demand explainability (which indicators drive the nowcast) and honest uncertainty bands. The risk in an algorithmic market is decision convergence: if everyone runs similar data and models, decisions correlate and diversification weakens exactly when it is needed. The durable edge is judgment under uncertainty, and accountability cannot be outsourced to a model.

What to watch next

The August 28 benchmark (and whether the QCEW-anchored count diverges sharply from the survey trend); the September FOMC; whether the 507,000 household-employment drop reverses; and the response-rate and collection notes in coming BLS releases — the mechanical driver of how noisy the first prints stay.

Sources: BLS Employment Situation, June 2026; BLS CES benchmark / QCEW; Orphanides, Monetary Policy Rules Based on Real-Time Data, AER 2001; Ghysels, Horan & Moench, Forecasting through the Rearview Mirror, Review of Financial Studies, 2018; CNBC, July 2, 2026.

Mandates Don’t Move Minerals. Corridors Do.

Colombia and Peru have both moved right — but for a universal owner the Andean turn is not a pro-market rerating. It is a corridor-control event: elections change security alignment, tax policy, permitting tone and diplomatic language, yet they do not automatically reroute the copper, nickel and gas the energy transition runs on. A 15-minute field investigation into who actually controls the routes.

By Nicolás Bohórquez Universal Asset Owners · 15 min read |

| Read the investigation → |

The whole brief, two more ways

A three-minute animated summary and an eight-slide visual deck that walk through everything in today’s issue — the jobs revisions, the $29tn rotation, the grid ownership model, and the allocator’s operating system for a degraded signal.

| Download the deck (PDF) → |