Volume 1, Issue 41. Sunday, June 21, 2026. Sent 7:00 am ET / 15:00 GST.

The Fed spent this week telling the world's longest-duration investors something they did not want to hear: the discount rate has stopped falling. On Wednesday, June 17, the committee held its target range but lifted its own 2026 median projection above the current policy midpoint and put nine of eighteen officials on record for at least one hike this year. The front end and the dollar repriced immediately and held the move into Thursday's close. Below: what the dots actually say, where the repricing landed, and why new Chair Kevin Warsh's first act was to put the Fed's own operations under review — plus a chart of the committee's forecast flipping from down to up.

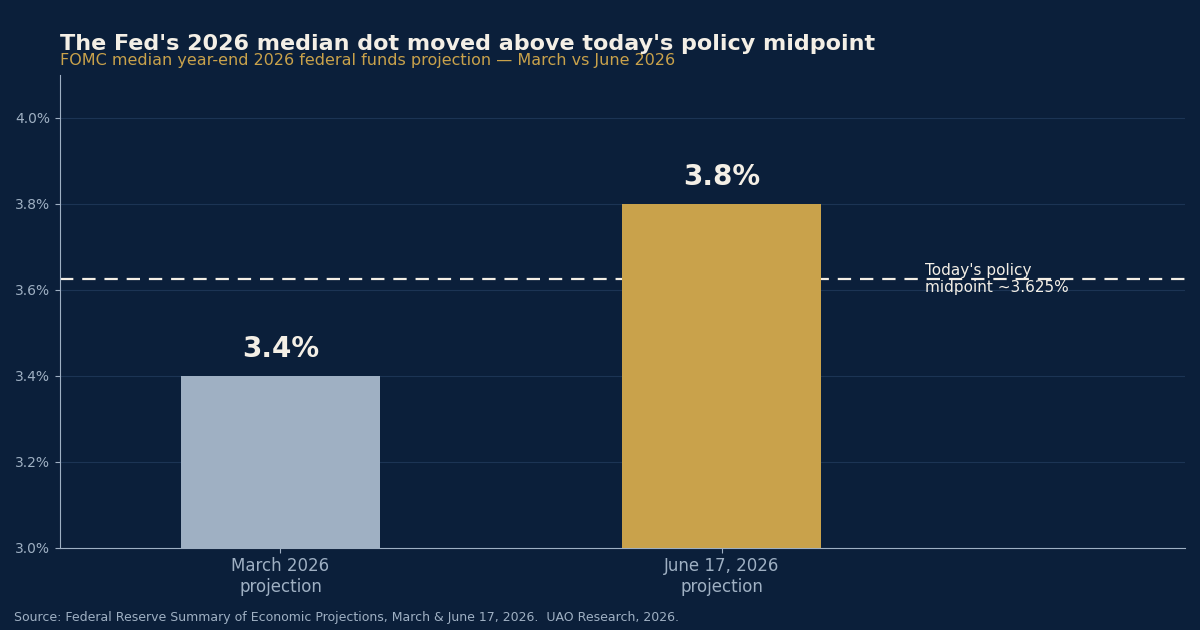

1. The Fed moved its own forecast above today's policy rate — the first time this cycle it points up.

On Wednesday the FOMC held the federal funds target range at 3.50%–3.75% but published a Summary of Economic Projections with a 2026 median dot of 3.8%, up from 3.4% in March. Because the current range midpoint sits near 3.625%, the committee's central forecast moved from implying a cut this year to implying a level above where policy is now. Nine of the eighteen participants placed their 2026 dot above the midpoint, the full range ran from 3.4% to 4.4%, and the easing bias that had framed the March projections was gone.

For a universal owner this is not a trading headline; it is the single input that reprices the entire book at once. Public equity multiples, the bond ladder, the marks on private portfolios, and the modelled cash flows on infrastructure all discount against the same curve. When the body that sets the short rate forecasts the path turning up rather than down, every one of those valuations is being told its tailwind has reversed.

The open question for allocation teams is whether to treat this as a one-meeting recalibration or as confirmation of a regime in which the policy rate has a higher floor than the post-2008 portfolio was built around. The deep-dive takes that question apart.

Source: Federal Reserve issues FOMC statement, June 17, 2026. | Coverage: AI and the Long-Term Portfolio → discount-rate regime, this week.

2. The repricing showed up in the front end and the dollar, not just the dots.

Markets did not wait for an explanation. On the decision the 2-year Treasury yield rose to 4.21%, its highest level in more than a year; the 10-year rose to 4.469%; and the dollar index gained about 1% for its best single day in nearly a year. Equities fell, and traders moved to price a possible hike as early as the autumn. With US markets closed Friday for Juneteenth, Thursday's close is the freshest print — and it held the move.

The front-end and currency reaction is where this matters most for cross-border allocators. A higher short rate plus a stronger dollar raises the cost of carry on every unhedged foreign asset and tightens the arithmetic on FX hedging programmes that reserve managers, Gulf sovereign funds and Asian institutions run at scale. A dollar that is both higher-yielding and stronger pulls marginal capital toward US cash and short paper — the opposite of the reach-for-yield posture that defined the last decade.

The read-across to peers: funds that lengthened duration into the expected easing cycle now carry mark-to-market losses on that bet, while those that stayed short are being paid to wait.

Source: Warsh Hawkish Shock: 9 Fed Officials Signal 2026 Rate Hike, Yahoo Finance, June 17, 2026.

3. Warsh opened his chairmanship by putting the Fed's own plumbing under review.

At his first meeting as chair, Kevin Warsh announced task forces to overhaul major Federal Reserve operations and, notably, did not submit his own dot to the projection set — while encouraging colleagues to submit theirs. The substance of the review is still to come, but the signal is not trivial: a new chair is choosing to reopen questions about how the institution operates rather than simply inheriting its machinery.

For the central-bank-adjacent investors in this audience — reserve managers, sovereign funds with monetary-authority lineage, large insurers — the credibility and predictability of the policy anchor is itself an asset they price. A chair who signals institutional change at the same meeting the committee turns hawkish introduces a second variable: not just where rates go, but how legible the reaction function stays while the plumbing is rebuilt. That is a governance question, and governance questions compound over a multi-decade horizon.

— Chart of the day —

The Fed's 2026 median dot moved above today's policy midpoint — its first up-pointing forecast this cycle.

Source: Federal Reserve Summary of Economic Projections, March 2026 and June 17, 2026. UAO Research, 2026.

— Take of the day —

"The denominator just changed for every long-horizon portfolio at once. A higher policy floor plus a term premium that has been rising for a year is not a tactical headwind you trade around — it is a re-rating of the rate at which all future cash flows are valued, and it lands hardest on the books with the longest duration and the slowest-marking assets. The disciplined response is not to flee duration but to re-underwrite pacing: assume distributions stay slow, assume marks catch down, and size new private commitments to a world where the discount rate has a floor it did not have in 2021."

— UAO Research.

— Three links worth your time —

- Federal Reserve — FOMC statement and Summary of Economic Projections, June 17, 2026. The primary document; read the dots and the statement language yourself before you read anyone's take on them.

- Goldman Sachs — How US Fiscal Concerns Are Affecting Bonds, Currencies, and Stocks. The fiscal half of the story: why a ~6%-of-GDP deficit keeps upward pressure on the long end regardless of what the front end does.

- BIS Quarterly Review — Term premia: models and some stylised facts. The methodology for thinking about the premium investors demand to hold duration — the variable doing the quiet work underneath this week's headlines.

The UAO Daily Brief is researched and edited by the Universal Asset Owners editorial desk for the world's largest long-horizon investors. Forwarded this? Subscribe. Reply to this email with what your team is watching.

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Universal Owner · view the chart of the day.

Produced and edited by the UAO editorial desk. Not investment advice.