When the gatekeeper for Sweden's premium pension system said this week that private credit was "long into the future, if that's possible at all," he did not reach for default rates or credit losses. He reached for plumbing: "Private market structures with daily liquidity are usually a recipe for difficulties." Sweden's Top Pension Gatekeeper Wants to Keep Private Credit Out, Bloomberg, June 10, 2026. That is the right place to look. The question a universal owner has to answer is not whether private credit borrowers will default — some always will — but whether the liquidity terms wrapped around those loans are a manageable product feature or a systemic fault line that lands hardest on the long-horizon balance sheet.

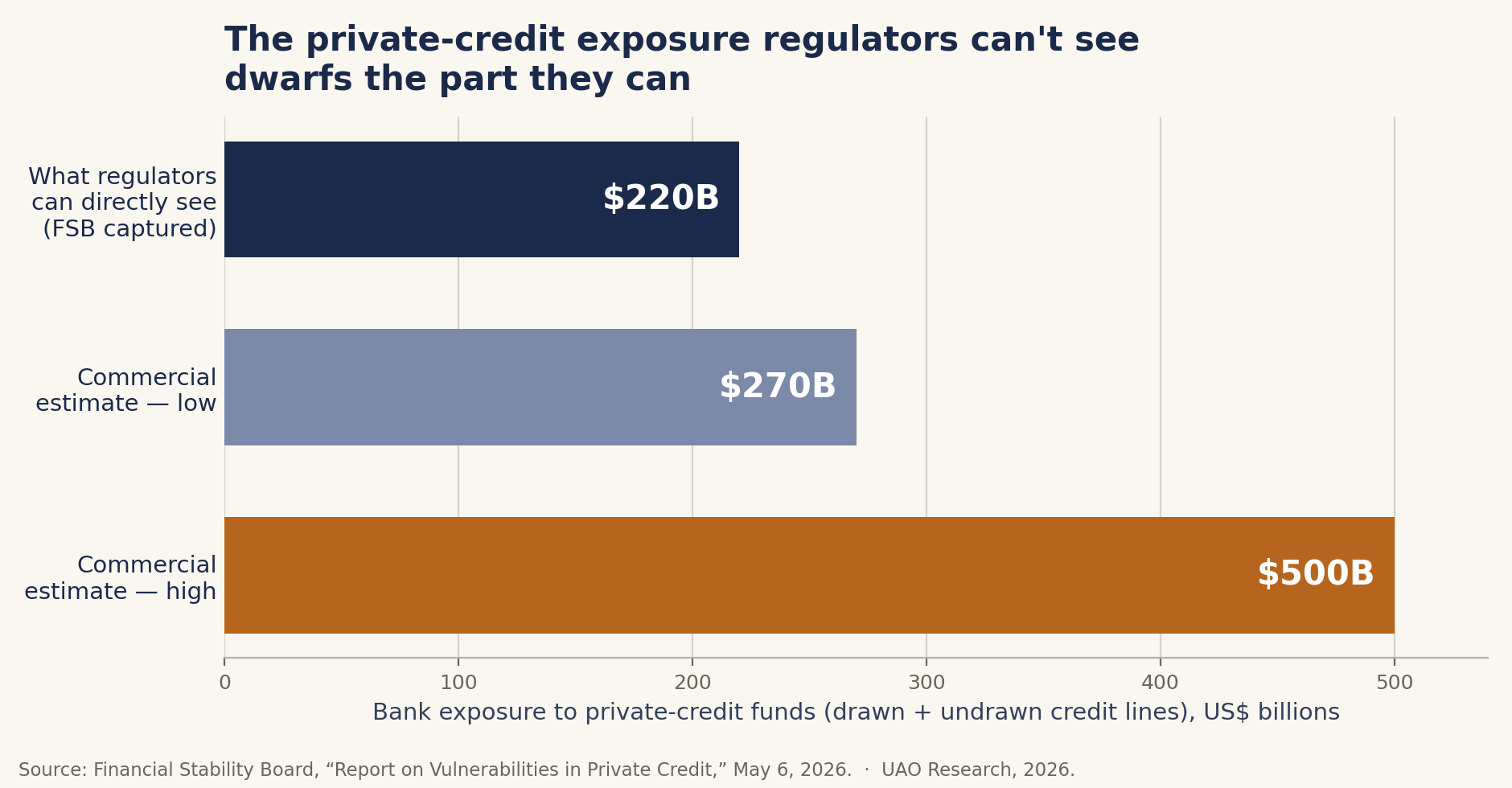

What the evidence says. Start with size and opacity. The Financial Stability Board, in its May 6 report, put the private credit market at $1.5–2 trillion and warned that borrowers "typically have lower credit quality and higher leverage" than comparable public-market borrowers, with rising use of payment-in-kind arrangements — a sign that some borrowers are servicing debt with more debt rather than cash. Report on Vulnerabilities in Private Credit, FSB, May 6, 2026. Crucially, the FSB could directly account for only about $220 billion of bank credit lines to private credit funds, against commercial estimates running to $270–500 billion. The supervisor's honest answer to "how big are the linkages?" is: bigger than we can see.

The mechanism that worries regulators is not the loans themselves but the vehicles increasingly used to hold them. The ECB's Financial Stability Review, published in late May, documented that semi-liquid structures — business development companies and the new wave of partly retail-oriented "evergreen" funds — have faced sizeable redemption requests since the start of 2026, with some funds capping withdrawals at the contractual gates written into their terms. Stress in global private credit markets and its implications for euro area financial stability, ECB Financial Stability Review, May 2026. These vehicles offer redemptions at a regular frequency while holding assets that do not trade. The ECB's language is precise: a deterioration in sentiment "can spur investors to withdraw their capital from funds offering redemptions at a regular frequency, despite their portfolio holdings being less liquid." That is the daily-liquidity trap Stockholm named, observed in the data rather than theorized.

Now the part that should change how an allocator reads this. The ECB ran a stress exercise tracing a severe shock through private credit — direct losses, then losses on correlated leveraged-loan and high-yield exposures, then broader second-round revaluation of public assets. Its finding is the one that matters for universal owners: the direct hit to banks is small, but the loss is "larger for insurance corporations and pension funds," and "by far the largest impact comes from the third stage" — the second-round revaluation of the public securities everyone holds. In other words, the diversified long-horizon owner is most exposed not through its private credit sleeve but through the public-market spillover that a private credit stress would set off. Pension and insurance investors are not bystanders here: the ECB notes they accounted for roughly 70% of private credit fund investments between January 2017 and May 2026, with direct euro-area exposures of about €211 billion (insurers) and €52 billion (pension funds).

The disagreement is real, and it is happening on the same calendar. Sweden's gatekeeper keeps the asset class away from savers; on Monday, June 15, the CalPERS Investment Committee — roughly $598 billion — takes a scheduled program-strategy review of a private-debt book it has deliberately built up. CalPERS Investment Committee agenda, June 15, 2026. Both are competent fiduciaries; both have read the same FSB and ECB work. The bull case is that closed-end, lock-up private credit — the institutional version, without the daily-redemption wrapper — is a genuinely different and more durable product than the semi-liquid retail vehicles the regulators flagged, and that a large plan with a long horizon and no forced-seller liabilities is precisely the holder that should own illiquidity and harvest its premium. The bear case is that the asset class has never been tested through a full default cycle at this size, that "true" leverage in the underlying borrowers can run to several turns of debt-to-EBITDA beneath fund-level figures, and that correlations the models treat as low are correlations that have simply not been observed under stress.

What it means from the allocator's seat. The universal owner cannot resolve that debate from the outside, but it can stop asking the wrong question. The exposure that matters is not "how much private credit do we hold?" but "how much of our private credit sits in vehicles that promise a liquidity we would have to provide by selling something else?" An institution with permanent capital and closed-end commitments is in a structurally different position from one holding evergreen funds with quarterly gates — even if the underlying loans are identical. The second-round-loss finding argues for treating private credit as a correlated public-market exposure for risk purposes, not a diversifier sitting quietly in an illiquid bucket. And it raises a governance point the Stockholm decision makes vivid: a gatekeeper's job is sometimes to refuse a premium that cannot be safely delivered to the end saver, and the same discipline applies inside a large plan deciding how much of its own book to put in redeemable form.

What to watch next. Three things. First, the CalPERS agenda materials on June 15 — specifically whether the private-debt review distinguishes lock-up structures from any semi-liquid exposure, which is the distinction that now carries the risk. Second, redemption-gate activity in US BDCs through the summer; the ECB's "since the start of 2026" framing means this is a live series, not a historical one. Third, whether other national pension gatekeepers follow Sweden's lead — because if the refusal to put private credit in front of retail savers spreads, it will reprice the asset class's assumed terminal demand long before any default cycle does.

Sources

- Bloomberg — "Sweden's Top Pension Gatekeeper Wants to Keep Private Credit Out," June 10, 2026.

- Financial Stability Board — "Report on Vulnerabilities in Private Credit," May 6, 2026.

- European Central Bank — "Stress in global private credit markets and its implications for euro area financial stability," Financial Stability Review, May 2026.

- CalPERS — Investment Committee meeting agenda, June 15, 2026.

- S&P Global Market Intelligence — "Sovereign wealth fund private market deals soar, pension fund activity slows," January 2026.