Research & Commercial Insight — Monday, July 14, 2026.

Watch: The Insurance Gate at Hormuz

Listen: Audio Overview

The geography of the Strait of Hormuz is fixed; its commerce, however, is fluid—and currently evaporating. While the waterway remains legally open, the physical reality shifted violently on July 13 when Iranian cruise missiles struck two UAE-flagged tankers. Yet, for the sophisticated observer, the more ominous signal appeared days earlier. Over the weekend of July 11–12, LNG carrier traffic through the Strait dropped to zero. By the morning of July 14, total tanker movement had hit its lowest level since May.As the United States prepares to enforce a maritime blockade of Iran at 20:00 GMT today, institutional investors must look past the missile batteries. A "Second Chokepoint" is emerging: an "Insurance Gate" that can shutter a global trade artery through contractual friction long before a naval blockade is fully realized.

The Concept of the Financial Gate

The Strait is currently governed by two distinct "gates" moving on different clocks. The first is navigational: the physical ability of a hull to pass without seizure or destruction. The second is contractual: the ability of owners, lenders, and charterers to assemble a compliant stack of insurance and operational consent.History shows these gates rarely synchronize. A naval escort can provide physical security almost instantly, but insurance wordings, reinsurance treaties, and lender requirements are notoriously stubborn. Conversely, insurers may continue to offer quotes even as shipowners—citing crew safety or board-level risk appetite—unilaterally withdraw their tonnage. For the universal owner, the financial gate is often the binding constraint.

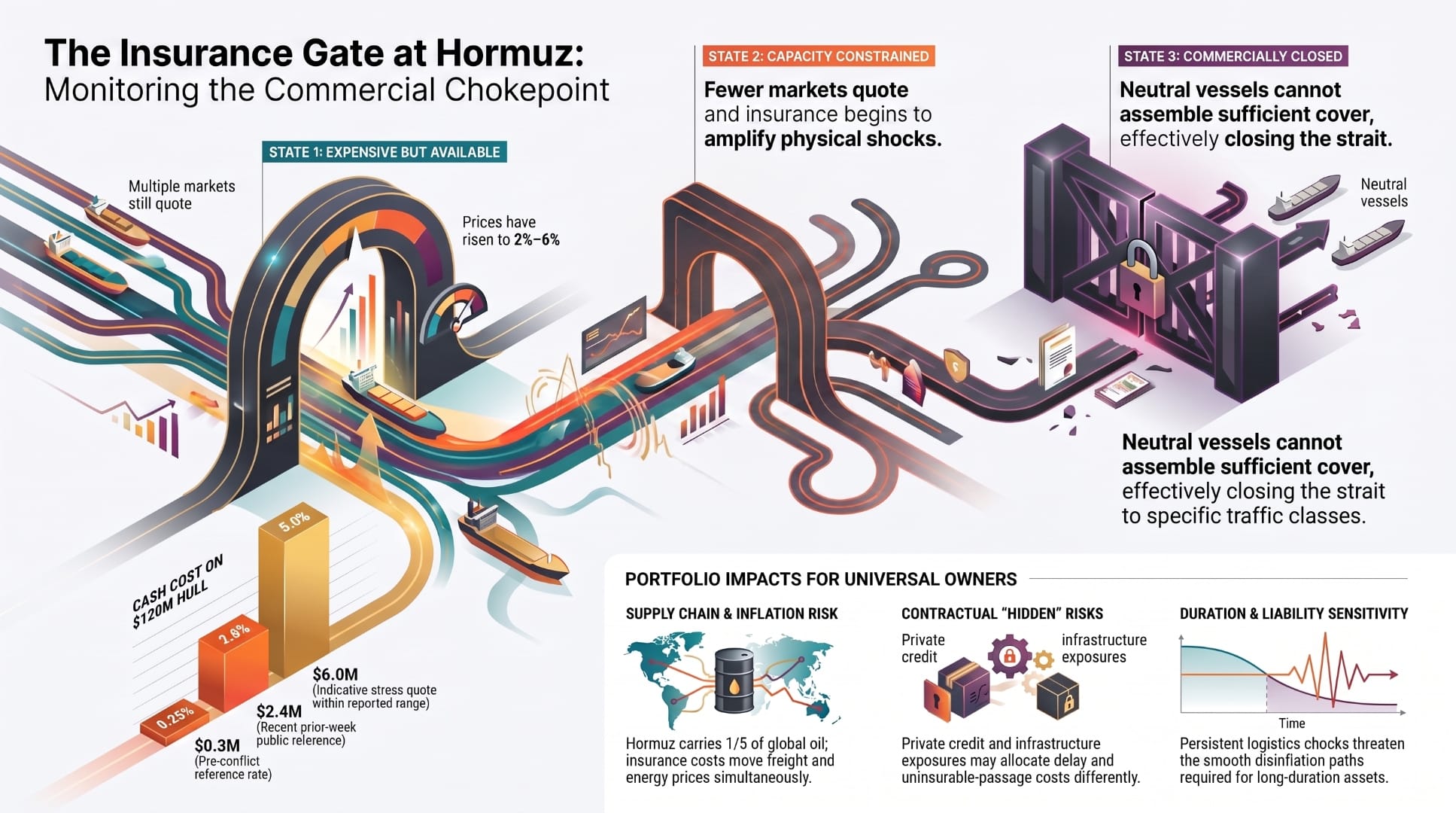

The Market Shift: From "Expensive" to "Constrained"

The Insurance Gate typically evolves through three states:

- Expensive but Available: Multiple markets quote; terms reset, but volume persists.

- Capacity Constrained: Quotes dwindle, limits fall, and dedicated facilities become the only viable option.

- Commercially Closed: Neutral vessels cannot assemble sufficient cover on workable terms.We are currently in State 1, but the "gate" is tightening. Tellingly, the market is already attempting to ring-fence risk. On June 19, a Chubb-led consortium announced $200 million in dedicated capacity for hull/P&I and another $200 million for cargo. This is not a sign of market health, but a defensive repackaging of capacity as broader appetite wanes. As one briefing concluded: "The insurance gate at Hormuz is tightening, not shut."

The "Silent Withdrawal" Feedback Loop

Standard analysis treats insurance inquiry volume as a proxy for market activity. In high-risk environments, however, a drop in inquiries is a bearish leading indicator. Recent data reveals that shipowners are requesting fewer quotes for Hormuz transits—a "silent withdrawal" where tonnage is pulled before a price is even discussed.This creates a dangerous feedback loop. As owners withdraw, the premium pool required by insurers to spread risk evaporates. This lack of volume forces insurers toward State 2 (Capacity Constrained), driving rates higher for the remaining few and eventually making coverage fundamentally unavailable for the volume of traffic required to stabilize global energy markets.

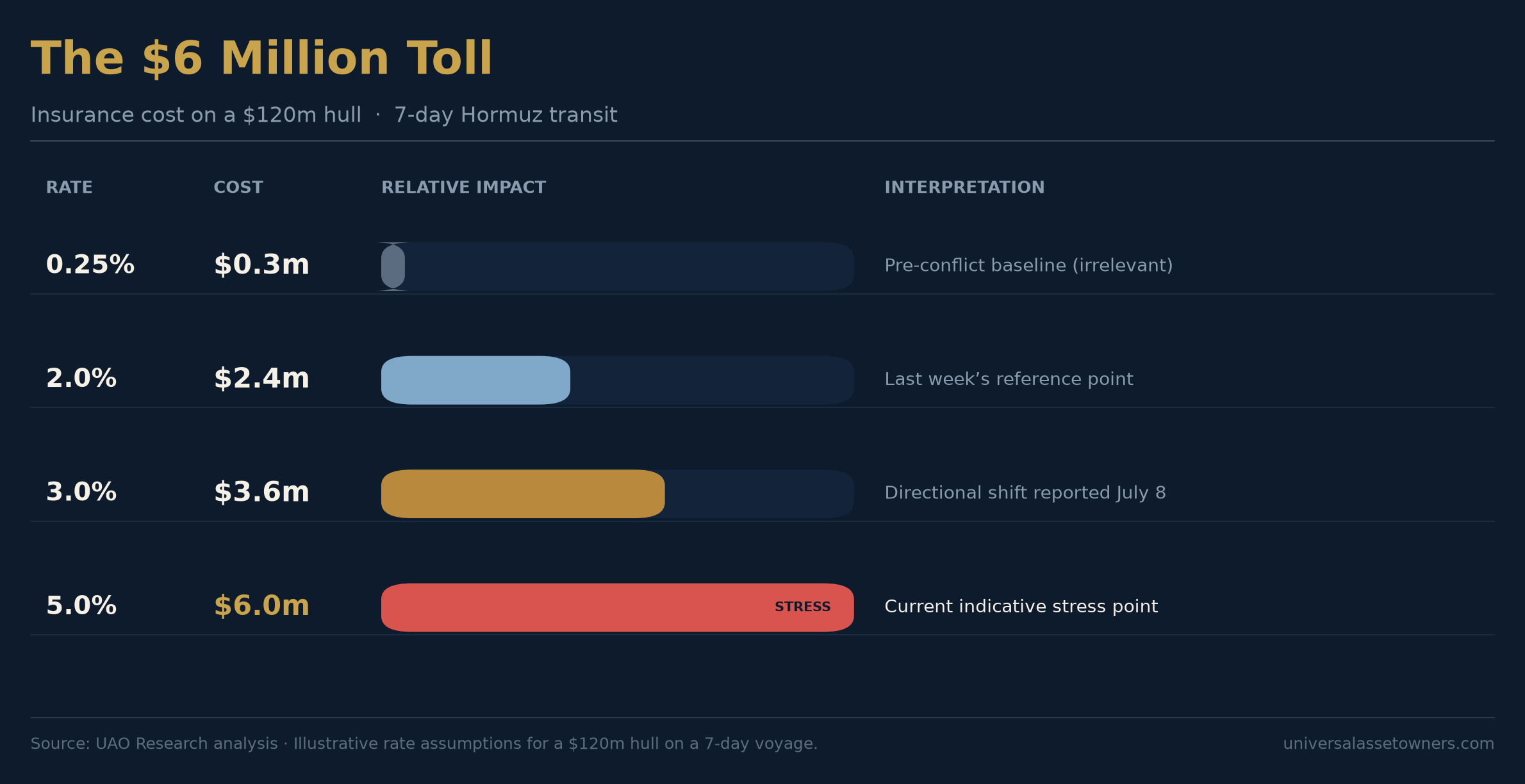

The $6 Million Toll: When Insurance Eclipses Freight

The economic viability of energy transport is collapsing under the weight of escalating premiums. For an illustrative vessel with a $120 million hull value, the cost of a simple seven-day voyage has moved from a negligible expense to a primary line item.

When a one-week transit costs $6 million in insurance alone, the fundamental arithmetic of global energy trade breaks. These costs are immediately exported via freight rates and energy prices, hitting long-duration portfolios and inflation-linked liabilities simultaneously.

The 20% "Shadow Toll" and Legal Friction

Compounding private costs is a proposed U.S. public policy: a cargo reimbursement charge equal to 20% of the cargo value. Based on a Brent crude price of $83.30 per barrel, the scale is unprecedented:

- 2.0 million barrel cargo: $33.3 million charge

- 2.2 million barrel cargo: $36.7 million chargeThis is not insurance; it is a geopolitical toll. The International Maritime Organization (IMO) has already signaled its opposition, maintaining that passage through the Strait must remain free of charges under international law. This legal friction adds a layer of "contractual uninsurability" that may prevent voyages even if the physical risk is deemed manageable.

Debunking the Solvency Myth: Trapped Capital vs. Insolvency

A common analytical error suggests that a few major tanker losses would bankrupt Lloyd’s of London. This misses the point. With £49.8 billion in total capital and a 200% solvency ratio at year-end 2025, Lloyd’s is structurally resilient.The real threat is not insolvency, but liquidity and willingness. The danger lies in "trapped capital" or "retrocession freezes," where reinsurers narrow terms so drastically that primary insurers—while solvent—simply refuse to deploy capacity. Investors should watch for the moment when cover is not just expensive, but unavailable at any price.

Strategic Implications for Asset Owners

Investment committees must move beyond monitoring oil futures to assessing their exposure to these invisible chokepoints:

- Sovereign Wealth Funds: Must separate the temporary upside of higher oil prices from the long-term risk to export volumes and domestic liquidity. Strategic "bypass" infrastructure (like the reported DP World talks in Fujairah) must be vetted for actual return, not just strategic need.

- Pension Funds: Stress-test inflation-linked liabilities and duration risk. If the "Insurance Gate" closes, the resulting logistics shock will disrupt the disinflationary path that many long-duration assets depend upon.

- Investment Managers: Identify who bears the cost if passage becomes uninsurable. Is it the owner, the charterer, or the end consumer?

Conclusion: The Ticking Clock

As the 20:00 GMT deadline for the U.S. blockade approaches, the question is no longer whether missiles will fly, but whether the insurance market will preemptively "blockade" the Strait. Even if the physical guns remain silent, a "contractual blockade" triggered by narrowing limits and voyage refusals can effectively sever the global energy supply.The critical indicator to watch is not the premium rate, but the transition from "expensive" to "constrained"—the moment when the volume of trade required for global stability simply cannot be covered.

The Insurance Gate at Hormuz — Slide Deck

25-slide flipbook below, or download the PowerPoint.

Watch: How the Insurance Gate Closes Hormuz

Subscriber-Only Research — Complimentary Sample

The Lloyd's Reinsurance Special Briefing

This special briefing is normally reserved for UAO paying subscribers and institutional clients. As part of our outreach to qualified prospective clients, we're releasing a complimentary preview of the full briefing below — read the opening pages, then request the complete PDF.

Researched and edited by the Universal Asset Owners editorial desk. Not investment advice.