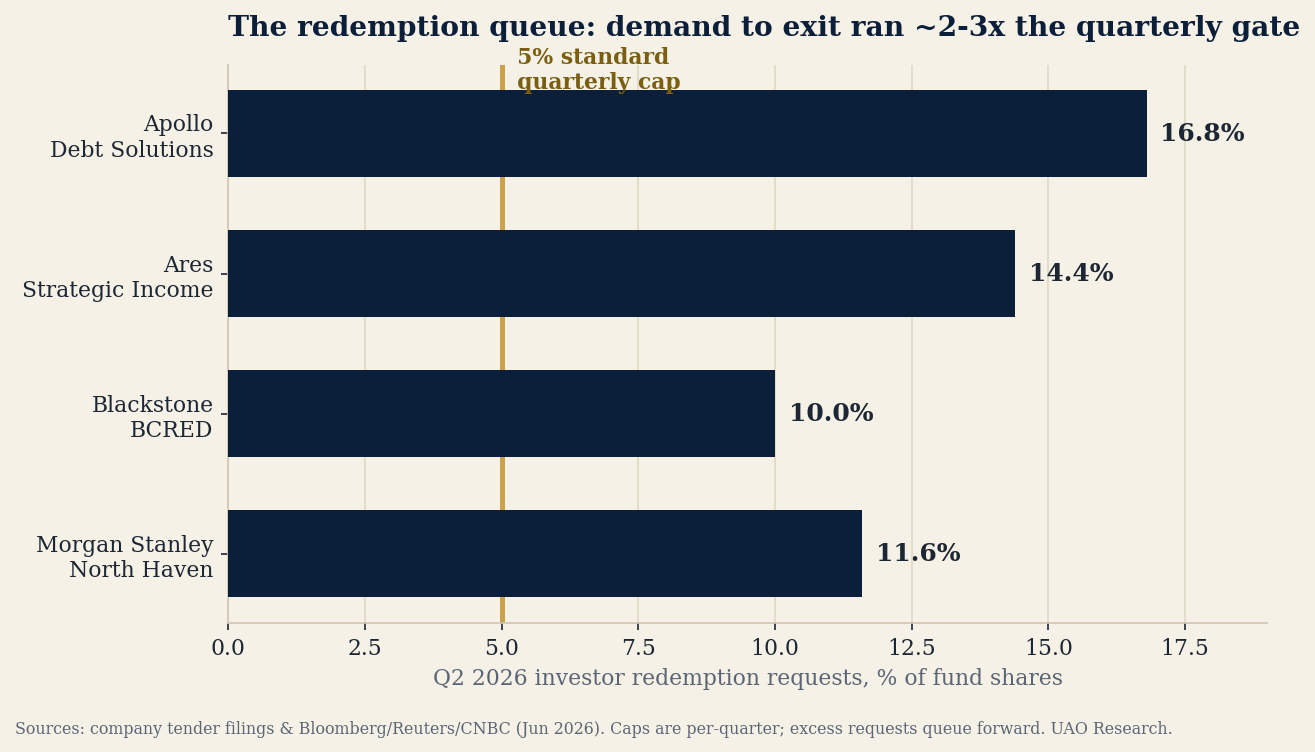

![[QC v4 — NOT SENT TO LIST] readable title + newsroom CTA — exit door / semi-liquid private markets](https://storage.ghost.io/c/f6/9c/f69cdeb4-cfe5-4393-a9d8-5769f759a132/content/images/size/w2000/2026/06/chart-redemption-queue-2026-06-26.png)

Private markets just sat their first real liquidity exam — and they did not fail it the way the headlines imply. In the second quarter, four of the largest semi-liquid funds — Ares, Apollo, Blackstone and Morgan Stanley — all capped investor withdrawals in the same window. At Ares' $22.6bn Strategic Income Fund, investors asked to pull 14.4% of shares (up from 11.6% the prior quarter); the fund honoured the standard 5% gate and met just ~34.7% of what was requested, pro rata. Yet 829 of its 831 loans were performing. This is the tell: the stress was not credit, it was liquidity design. Private markets do not need a default cycle to create governance risk — they only need investors to ask for their money at the same time.

A 50/50 climate-tech + carbon-finance barbell, built with the UN Environment Programme and now raising. See the strategy →

1. The exit door opens in semi-liquid private markets.

The number that matters is the spread between what investors asked for and what they got. Across the wealth-channel's flagship evergreen funds, Q2 redemption demand ran two to three times the 5% quarterly gate: Ares 14.4%, Apollo Debt Solutions 16.8% (its largest since the fund's 2022 launch), Blackstone's BCRED ~10%, Morgan Stanley's North Haven 11.6%. None of these are credit blow-ups — Ares reported 829 of 831 loans performing and a positive year-to-date return. The pressure was also concentrated, not a retail panic: Reuters reports the bulk of Ares' requests came from non-US institutions and family offices — under 1% of its 20,000-plus shareholders — while US private-wealth requests were just 2.4% of shares and actually fell about a third. Investors pulled $12.9bn from wealth-channel private-credit funds in the first five months of 2026 (Stanger). The promise of these wrappers is “private assets, liquid enough.” This quarter tested the “liquid enough” — and the gate held, which is the point: the gate is the product working as designed, not failing.

Implication for owners: Treat this as a re-underwriting prompt, not a fire alarm. For every semi-liquid fund you own, ask one plain question: if a quarter of your co-investors tried to leave at once, are you comfortable being gated beside them? Wherever the honest answer is no, you have been counting a multi-year asset as ready cash — far better to resize or relabel it now, while the loans still perform, than to discover the mismatch from inside the queue.

Sources: Bloomberg (Ares, Jun 25) · AltsWire (14.4% / 34.7% honoured) · CNBC (Apollo 16.8%) · Bloomberg (BCRED) · Investment Executive (Morgan Stanley)

2. The cushion returned — but inflation did not leave.

The latest BEA print was a study in crosswinds. The PCE price index rose 4.1% year-on-year in May, with core PCE at 3.4% — both the firmest since 2023. Personal income, disposable income and consumer spending each rose 0.7% on the month: a consumer still spending into sticky prices. And yet bonds rallied — the 10-year Treasury yield eased to about 4.37%, near a six-week low, helped by the slide in oil. For a universal owner the cushion came back, but for the wrong reason: duration is rallying on falling energy, not on a credible disinflation path. A higher-for-longer cost of capital is exactly the regime that makes semi-liquid private assets harder to sell, harder to refinance, and harder to defend when an investor wants cash.

Implication for owners: Don't read the bond rally as the all-clear. With core PCE still at 3.4%, the discount rate isn't falling on fundamentals — so stress your private marks against a rate path that stays high, not one that obligingly drops.

Sources: BEA, Personal Income & Outlays, May 2026 (released Jun 25) · Trading Economics (10Y yield)

3. Risk radar: Hormuz repriced, not resolved.

Oil fell again Friday and is headed for a steep weekly loss — Brent near $73.8 and WTI near $70.4 — as more tankers resumed transit through the Strait of Hormuz, even after a vessel was struck near Oman. The war premium that had lifted crude sharply earlier in the month has largely bled out. But “repriced” is not “resolved”: the projectile incident is a reminder that the chokepoint risk hasn't gone away, it has simply moved from the front page back into the tail. For the universal owner the lesson is structural — a single strait is now an asset-allocation input that moves your energy, inflation, rates and currency books at once.

Implication for owners: Keep Hormuz in the allocation model, not just the news feed — price the tail explicitly, so you are positioned for it rather than re-reacting each time the premium snaps back.

Sources: Trading Economics (Brent/WTI, Jun 26) · CNBC (US-Iran roadmap & Hormuz shipping)

4. AI infrastructure: memory becomes a contracted supply chain.

Micron's fiscal-Q3 results moved AI memory from speculative capex into contracted scarcity. Revenue hit $41.5bn (up ~346% year-on-year) at a record ~84.9% non-GAAP gross margin, with fourth-quarter revenue guidance of $50bn ± $1bn. The structural tell: Micron signed 16 Strategic Customer Agreements, 14 of which carry roughly $100bn of cumulative minimum revenue commitments on five-year, take-or-pay terms, plus about $22bn of cash deposits and related financial commitments (including roughly $18bn in cash deposits). When buyers pre-commit to volume regardless of price, memory starts to look less like a cyclical commodity and more like a long-term power contract — reinforcing both the AI-equity concentration and the inflation impulse threaded through this brief.

Implication for owners: Take-or-pay memory contracts make the AI build-out's revenue more visible — and its cost more durable. Size the inflation pass-through, not just the equity upside, because you hold both sides of it.

Sources: TechTimes (Micron Q3, Jun 25) · Micron Investor Relations

5. Watch next: NATO's defense-industrial cycle.

Bigger defense spending will top the agenda when NATO leaders meet in Ankara on July 7–8. Secretary-General Mark Rutte has signalled the summit will translate last year's pledge — 5% of GDP on defense and security by 2035 (3.5% core military plus 1.5% resilience and infrastructure) — into tens of billions of dollars of concrete procurement and capability targets. For long-horizon owners this is the shift from a tactical budget line to a structural capital cycle: multi-year procurement, dual-use AI, supply-chain and infrastructure spend — funded by heavier sovereign issuance that competes for the same duration owners are buying.

Implication for owners: Position ahead of Ankara as a decade-long allocation theme — defense, dual-use industrials and the infrastructure around them — while sizing the sovereign supply that funds it against your duration book.

Sources: Washington Times (summit agenda, Jun 25) · NATO (5% commitment)

The redemption queue: Q2 demand to exit ran two-to-three times the quarterly gate.

Sources: company tender filings & Bloomberg / Reuters / CNBC (Jun 2026). Excess requests queue forward. UAO Research.

Built today and live now: an interactive map of how higher-for-longer rates, a shut exit window and wealth-channel inflows combine into synchronized redemptions — tripping gates and forcing a mark-vs-exit question on the universal owner. Click any player — a pension CIO, an insurer, a chief risk officer — and ask the desk what they do next. The headline figure is the desk's judgment-weighted probability that a second large evergreen fund pro-rates redemptions within 90 days.

Open the live scenario →A gate quietly rewrites the rules of stewardship: when you can't exit, you have to engage. Selling is the cheapest form of governance — and a redemption cap takes it off the table for everyone queued behind the 5%. Their only remaining lever is voice: pressing managers on how marks are struck, who sits on the valuation committee, and what actually triggers the gate. The sharper, newer duty question is landing on DC plan sponsors: as private assets move into 401(k) target-date defaults, can a daily-valued, daily-liquid retirement option safely hold a fund that just met one dollar in three of redemption requests? The Financial Stability Board's May review urged exactly this liquidity stress-testing. This isn't the familiar ESG fault line — it's a plumbing question about whether retirement savers should sit behind a gate at all. How much weight a trustee can put on stewardship, liquidity terms and long-term system risk still differs by regime: the UK's FRC Stewardship Code sets voluntary stewardship and transparency expectations for asset owners and managers, while 2026 US DOL / EBSA guidance keeps ERISA fiduciary actions anchored to maximizing risk-adjusted financial return. Presented as contested; both sides per house standard.

Do we know which sleeves, consultants, OCIO mandates or wealth-channel structures rely on quarterly-liquidity assumptions that would fail under synchronized redemption behaviour?

• APG (Europe's largest pension investor) is planning to lift private-markets exposure above 30% of assets, treating current credit volatility as a buying opportunity rather than a reason to retreat. (Benefits & Pensions Monitor)

• Nest (UK state-backed DC scheme) has committed £450m to US private credit and is targeting ~30% private-markets by 2030; CalPERS is staying the course on its private-credit build under a total-portfolio approach. (Markets Group)

“The semi-liquid gate did its job this quarter — which is precisely why every allocator should re-read the fine print now, while the loans are still performing. The question private markets just put to you isn't 'will it default?' It's 'did you buy strategic capital, or a yield product with an exit door?' You want to answer that before the queue does it for you.”

Whether a second large evergreen fund pro-rates Q2 redemptions · secondary-market discounts to NAV · queue resubmission rates · whether managers meet gates with credit lines, repayments or asset sales · core PCE and the next Fed dot plot · Brent and any fresh Hormuz incident · the July 7–8 Ankara summit · AI-memory pricing and data-center credit spreads.

Bloomberg — Ares private-credit fund caps redemptions after 14% seek to exit

FSB — Report on vulnerabilities in private credit (May 6, 2026)

More for long-horizon allocators — recent deep dives worth your time:

Universal Asset Owners · info@universalassetowners.com

QC PREVIEW — sent to the editor only.