Today’s podcast Listen to The Universal Owner Our daily audio briefing for long-horizon capital — the same analysis, for your commute. Follow the show so every weekday episode lands automatically.

|

Volume 1, Issue 38. Thursday, June 18, 2026. Sent 7:00 am ET / 15:00 GST. DRAFT — pending Tim's approval.

Yesterday at 2 p.m. Eastern the Federal Reserve answered a year's worth of speculation about Kevin Warsh in about forty minutes: no rate move, no forward guidance, no dot from the chair, and five task forces to overhaul the institution from the inside. Nine of eighteen members are now projecting at least one hike this year. The world's largest sovereign fund just reported its best recovery quarter in years — and the tool that tracks it is today's Research Tool. Below: what Warsh actually changed, what it means for long-horizon capital into a Juneteenth long weekend, and why Norway's $68 billion comeback is the frame every allocator needs for what comes next.

1. Warsh drops forward guidance — and rewrites the Fed playbook.

The rate decision was a formality: a unanimous 12-0 hold at 3.50–3.75%. The substance was everything else. Kevin Warsh used his first press conference as chair to announce that the Fed has "dropped forward guidance" — the practice, standard since 2008, of signalling the likely path of rates to anchor market expectations. The revamped FOMC statement shrank to its shortest in the modern era and ended with a single line: the committee "will deliver price stability." The shift is not cosmetic. Forward guidance was the mechanism by which the easing put was communicated, re-priced, and re-priced again through eighteen months of rate-path uncertainty. Removing it does not change rates — it changes the price of information about rates.

Warsh also announced five task forces — on communications, the balance sheet, data, productivity and jobs, and the inflation framework — composed of internal and external experts, with recommendations due by year-end. The arc is legible: the chair who called the dot plot a "relic" is building the case to retire or replace the whole communications apparatus, probably by next year's January meeting.

Source: CNBC — Fed meeting recap, Warsh announces task forces, June 17, 2026. | InvestingLive — Warsh rewrites the Fed playbook, June 17, 2026. | Coverage: Macro, today.

2. Nine dots for a hike — the rate path after yesterday.

The dot plot is the number that will move portfolios. The median year-end forecast rose from 3.4% in March to 3.8% — a full 30 basis points above the current top of the range. Nine of eighteen members now project at least one hike in 2026; six project two. Warsh withheld his own dot for the second consecutive meeting, consistent with his stated view that the SEP as currently structured is misleading. The 2-year Treasury yield jumped 16 basis points to 4.216% in the immediate aftermath; the S&P 500 fell 1.21% and the Nasdaq 1.34%.

This morning markets are muted — equity futures near flat, the 10-year yield at 4.45% — which is a signal worth reading. The session closes early on Juneteenth (Friday June 19 is a federal holiday, NYSE and Nasdaq closed), leaving institutional allocators one afternoon session to position, hedge, or sit still before a three-day weekend with a hawkish Fed signal fresh in their books.

Source: Fox Business — June FOMC, Warsh era begins, June 17, 2026. | Rockstar Markets — FOMC Decision June 2026 live reaction. | Coverage: Macro, today.

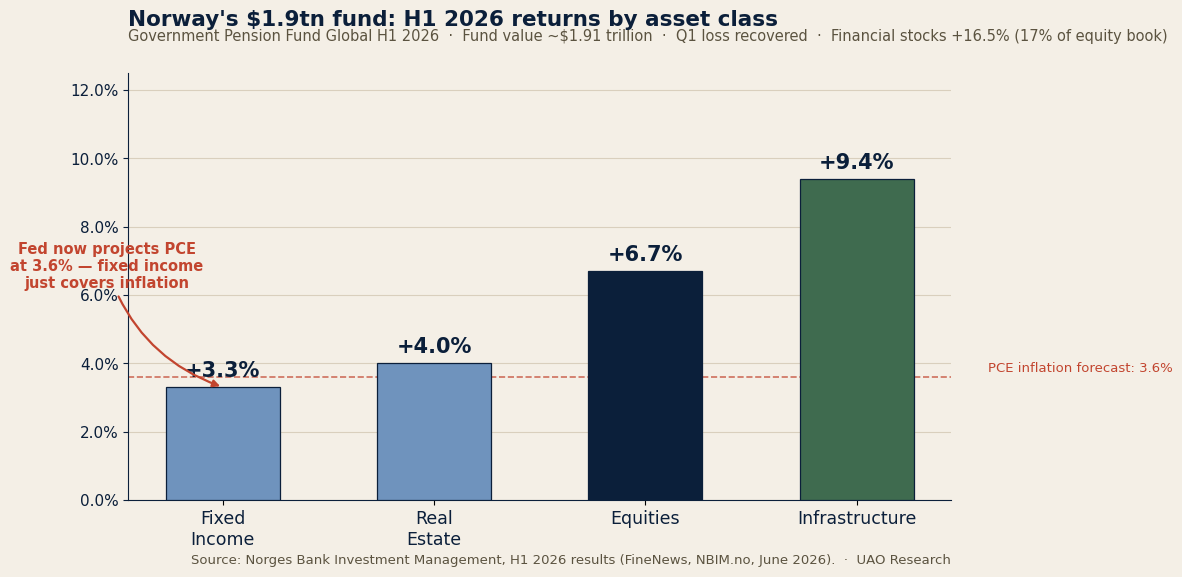

3. The world's largest fund recovered $68bn from its Q1 rout — and the read-across matters.

Norway's Government Pension Fund Global — the world's largest sovereign wealth fund, now valued at approximately $1.91 trillion — posted a 5.7% return in the first half of 2026, generating NOK 698 billion ($68.3bn) in investment gains. It is the strongest story the fund can tell after a painful first quarter that briefly knocked the fund below $1.9 trillion. Financial stocks drove the equity recovery, returning 16.5% over H1 and accounting for 17% of the equity book. Infrastructure returned 9.4%; equities overall returned 6.7%; real estate returned 4.0%; fixed income returned 3.3%.

Three things stand out for an allocator watching Norway as a benchmark. First, the full recovery was driven almost entirely by a single sector — financials — which underscores how concentrated the rebound was. Second, infrastructure's 9.4% was the strongest of any sleeve, at a moment when the rate path has just turned against leverage-dependent real assets generally. Third, fixed income at 3.3% — in a world where Brent fell from $113 and PCE is now projected at 3.6% through year-end — leaves less cushion than that number implies if yields reprice further from yesterday's dots.

Source: FineNews — Norwegian Sovereign Wealth Fund Benefits from Stock Market Recovery, H1 2026. | Norges Bank Investment Management — Fund returns. | Coverage: Sovereign Wealth Monitor.

4. Private-market allocations hit a record high — going into exactly this test.

According to Aviva Investors' 2026 institutional study, average private-markets allocations among global institutional investors reached 12.5% of total portfolio — the highest since the study began eight years ago. North American allocators lead at 14.4%. 88% plan to maintain or increase that exposure over the next two years. Institutional investors' primary driver is diversification (76%), followed by the illiquidity premium (55%).

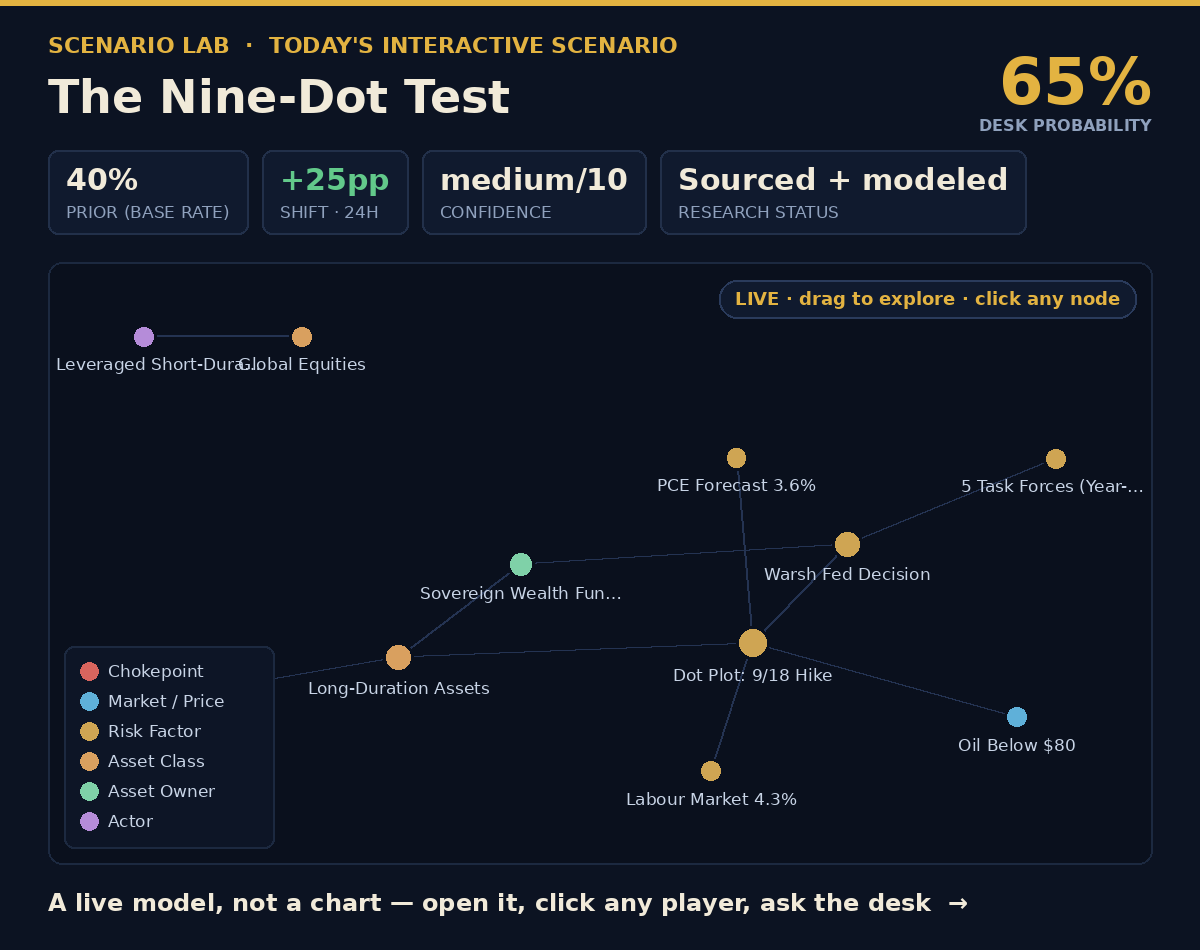

Scenario Lab · A new interactive scenario every day The Nine-Dot Test — 65% desk probability  This is not a chart — it’s a live model you can get inside. Every morning the desk rebuilds it from sourced market, policy and flow signals, scores today's probability against a 40% historical base rate, a +25pp shift in the last 24 hours, confidence medium/10, and maps all 11 institutions, markets and risk factors it touches into a live relationship graph. Open it and the map responds: drag the network, click any player — Dot Plot: 9/18 Hike, Warsh Fed Decision, Long-Duration Assets — and see exactly what it drives and what drives it. Then interrogate it: 6 vantage points sit inside the scenario — a sovereign wealth allocator, a pension CIO, a reinsurance underwriter, the markets desk — and each answers your questions in its own voice, grounded only in the scenario's research.

|

The timing of this peak allocation matters. Illiquidity premia are worth most when the public market is volatile and the marginal buyer is constrained — exactly the environment that a hawkish dot plot and a lost easing put create. But they are also most vulnerable when the discount rate that underlies private-asset marks moves upward and stays there. Nine dots for a hike and a year-end median of 3.8% is precisely that scenario. The allocation trend is sound; the vintage and entry-price discipline that comes with it is the variable to watch.

Source: Aviva Investors — Private Markets Study 2026, allocations reach new high. | Pensions Age — Private markets allocations hit record 12.5%. | Coverage: Private Markets.

5. Today's take: the Juneteenth gap — one session to position for a post-guidance world.

This afternoon is the last session before a three-day weekend, the first full trading day after the Warsh Fed declared it will no longer signal what it plans to do next. For a long-horizon institutional owner this is not a tactical problem — you cannot trade around a dot plot and a holiday. But it is a structural moment. The Fed that guided markets through every twist of the post-COVID cycle has gone quiet. There is no longer a sentence in the statement that tells a CIO what to expect. The chair has withheld his own number. Five task forces will redesign the communication architecture entirely.

The universal owner who carries illiquid assets through a rate cycle just lost the navigation aid they had been given. What replaces it — inflation data, labour market prints, Warsh's own public statements — is less precise, more volatile, and harder to anchor a twenty-year liability stream to. That discomfort is the new baseline.

Source: EBC Financial Group — Is the stock market open Juneteenth 2026? | The Hill — Federal Reserve shifts away from forward guidance under Warsh. | Coverage: Universal Ownership.

— Chart of the day —

Norway's $1.9tn fund: how each asset class performed in a year the rate path mattered.

Source: Norges Bank Investment Management, H1 2026 results. Fund value ~$1.91 trillion USD as at June 30, 2026. UAO Research.

— Take of the day —

"The Fed that guided markets for sixteen years went quiet yesterday afternoon. No forward guidance. No dot from the chair. Five task forces that will rebuild the communications architecture by year-end. For an allocator whose discount rate just moved 30 basis points in a dot plot, the new question is not 'what does the Fed signal next?' It is: 'what does policy mean when the Fed stops signalling?'"

— UAO Research.

— Research Tool of the Day — Day 3 of 12 —

Shadow the Oil Fund → /shadow-the-oil-fund/

Norway's Government Pension Fund Global — the world's largest sovereign fund — just posted its H1 2026 results. Track how the fund is actually positioned: its equity book by sector, its fixed-income exposure, and whether your own allocation mirrors, trails, or departs from the benchmark every CIO watches. Free. No login.

Open the Shadow the Oil Fund tracker →

— Three links worth your time —

- CNBC — Fed meeting recap: Warsh announces task forces to overhaul major Federal Reserve operations. The clearest account of yesterday's press conference and the five reform task forces.

- FineNews — Norwegian Sovereign Wealth Fund Benefits from Stock Market Recovery, H1 2026. NBIM's $68.3bn H1 recovery and what drove it.

- The Hill — Federal Reserve shifts away from forward guidance under Warsh. The structural shift in how the Fed now communicates — and what it removes from every allocator's toolkit.

UAO Daily Brief. Researched and edited by the UAO editorial desk. Not investment advice. Contact: info@universalassetowners.com.

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Universal Owner · view the chart of the day.

Produced and edited by the UAO editorial desk. Not investment advice.

Daily Oracle Brief

The Probability Desk’s governed read on the state of the world — the structural risks a universal owner carries, and what moved today.

The Universal Owner — Daily Oracle Brief

2026-06-18 · model run 2026-06-18 11:07 UTC · 10 structural risks · radar load 7.9/100

The state of the world

The desk is tracking 10 structural risks at a combined radar load of 7.9/100 — 8 rising, 1 easing this run. The dominant vector is market & capital regime (the diversification & capital-cycle dividend fading), followed by geopolitical fragmentation. Read together, the board describes a world becoming less hedge-able and more security-priced: the diversification, globalization and disinflation dividends that quietly underwrite long-horizon return assumptions are eroding at the same time. For an owner of the whole market, the through-line is that systemic, cross-asset risk is migrating from the tails toward the base case — while the very tools used to hedge it (long bonds, geographic diversification, insurance, the dollar's exorbitant privilege) are each, separately, under quiet strain.

Forces, ranked by where capital is most exposed:

- Market & capital regime — the diversification & capital-cycle dividend fading (mean 26%, ▼ -2.0pp this run)

- Geopolitical fragmentation — a security premium repricing trade & energy (mean 53%, ▲ +8.0pp this run)

- Climate & resource stress — physical risk migrating into collateral & sovereigns (mean 40%, ▲ +11.0pp this run)

- Monetary & fiscal order — the dollar anchor & fiscal space eroding (mean 32%, ▲ +7.0pp this run)

- Demographic gravity — aging suppressing real rates, growth & the bid (mean 32%, ▲ +5.0pp this run)

What moved

- Chokepoint concentration as a standing factor (Hormuz + Taiwan + Malacca + Panama) 53.0% (+8pp) — Strait of Hormuz traffic returns to normal by end of August? [Polymarket]

- Transition-mineral & grid-interconnection bottleneck caps electrification / AI 43.0% (+5pp) — Copper (global price)

- Pension-system inversion 33.0% (+5pp) — 10y-2y curve

In focus: Chokepoint concentration as a standing factor (Hormuz + Taiwan + Malacca + Panama)

Governed estimate 53.0% (sourced prior 45.0%, +8pp from live signals; confidence 5/5; tail-priority 21.1).

The prior is a documented base rate — At least one portfolio-material maritime-chokepoint disruption (Hormuz / Suez-Bab-el-Mandeb / Malacca / Panama / Taiwan) in a rolling 3-year window (Systemic impacts of disruptions at maritime chokepoints (Nature Communications)).

Why a universal owner should care (consequence chain): 1. A single strait disrupts ~20% of oil/LNG or container flow 2. Freight + insurance + energy cost-push 3. Inflation/rates repricing 4. Route diversification capex; friend-shoring 5. Globalization dividend in return assumptions erodes

Blind spot the desk is investigating

Surfaced by the source-gated simulation leg. It carries 0% weight on any published probability — it tells us what to investigate, not what is true.

- Insurance/freight cost-push as a distinct inflation channel — Agents separated war-risk premia + re-routing from the energy shock; this leg persists even when crude round-trips. (investigate: size historical insurance/freight cost-push vs oil in past chokepoint episodes; add to inflation stress test)

- Friend-shoring eroding the globalization dividend in CMAs — Recurring agent theme: low-vol, high-duration repricing of the return premium embedded in long-horizon assumptions. (investigate: quantify globalization-dividend assumption in our return model; sensitivity to friend-shoring)

What it means

For universal owners: Treat correlation-regime risk as a base case, not a tail: the bond hedge and the 60/40 may not cushion the next equity drawdown. For sovereigns & SWFs: Reserve diversification and the erosion of dollar privilege argue for a deliberate currency and gold posture, not drift. For pensions: Demographic gravity (aging, net-seller inflection, low real rates) is the long anchor — funding and contribution policy should assume it.

Explore it yourself: open the Scenario Lab (universalassetowners.com/scenario-lab/) to see any scenario as a live relationship map and put your own questions to the sovereign-wealth allocator, the pension CIO, the reinsurer and the markets desk.

Read the full reasoning behind any number at the Oracle (universalassetowners.com/oracle/) and the live board at the Command Center (universalassetowners.com/command-center/). Probabilities are the desk's analytical estimates, fused from public-source signals through a transparent, explainable model; they are not forecasts of certainty. Editorial scenario analysis for long-duration capital — not investment, actuarial, legal or financial advice.

The Daily Delta · what changed today · as of 2026-06-18 What moved for an owner who can’t diversify away

|

More from today: listen to The Universal Owner on Apple Podcasts or Spotify · watch the video briefing · the chart of the day.

Produced and edited by the UAO editorial desk. Editorial analysis for long-duration capital — not investment advice.