Today’s podcast Listen to The Universal Owner Our daily audio briefing for long-horizon capital — the same analysis, for your commute. Follow the show so every weekday episode lands automatically.

|

▶ Watch the video briefing & read the full analysis →

The largest IPO in history is coming, and the people who will be forced to own it are calling its governance "reckless." SpaceX is targeting a valuation of at least $1.8 trillion — a number that would put it straight into every major index, and therefore straight into every indexed portfolio on earth. Pension funds cannot vote away the structure they object to, and most of them cannot refuse to buy. One Danish fund just did. Below: the revolt, the refusal, and the $20 billion pressure valve opening up in private credit — plus the chart of the day and three links worth your time.

🎧 Listen to today's edition. The Universal Owner covers today's brief — plus a deeper take on who really controls the trillion-dollar index switch — in about twelve minutes. Follow on Spotify or listen on the site — one tap, and every morning's episode comes to you.

▶ Watch the video briefing

▶ Watch the video briefing1. Pension funds call SpaceX governance "reckless" — as forced buying looms.

The universal-owner problem rarely arrives this cleanly. SpaceX is preparing an IPO at a targeted valuation of at least $1.8 trillion — large enough for rapid inclusion in the major indexes, which means index-tracking pension capital will be buying whether it wants to or not. And it does not want to. Elon Musk is expected to retain more than 80% of the voting rights while holding the roles of chief executive, chief technology officer, and chair of the board. In mid-May, Marcie Frost, CEO of the roughly $598 billion CalPERS, joined New York City Comptroller Mark Levine and New York State Comptroller Thomas DiNapoli in a letter to Musk objecting to the company's "extreme governance structure." This week Pensions & Investments reports fund executives describing the arrangement as "reckless" — with the same executives acknowledging that index inclusion will make them owners anyway.

For a universal owner, this is the whole stewardship question in a single filing: when you own the market, you do not choose your holdings — your only lever is governance, and SpaceX's structure is engineered so that the lever does not move. A company can now come to public markets at a $1.8 trillion ask, concentrate control beyond anything the governance codes contemplate, and know that trillions in indexed capital must show up regardless.

Source: Pensions & Investments, "Pension funds call SpaceX governance 'reckless' as forced buying looms ahead of IPO," June 8, 2026 | Coverage: The Universal Owner Risk Radar, this week.

2. The first fund to walk away — and what saying "no" actually costs.

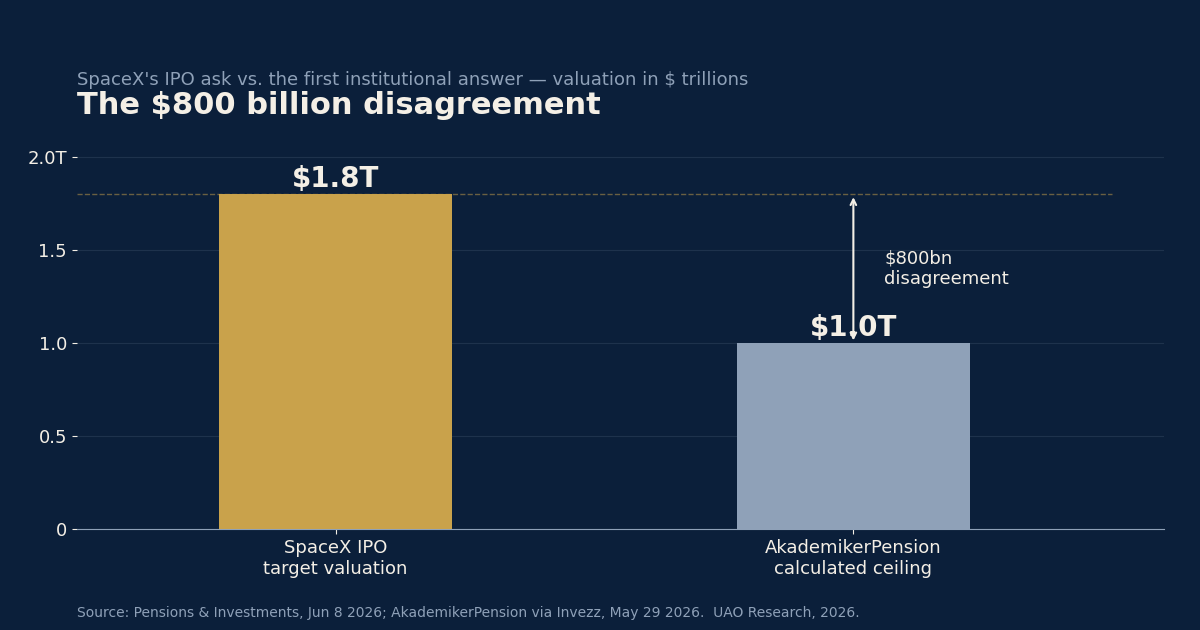

One institution has already done the thing the others say they cannot. Denmark's AkademikerPension has blacklisted the SpaceX IPO, putting numbers on both objections. On valuation: by the fund's own calculation, SpaceX cannot reasonably be worth more than $1 trillion — meaning investors at the $1.8 trillion ask are being offered unusually low compensation for the risk. On governance: the fund said the structure alone would be disqualifying even if the price were right, and that its concerns are shared by other institutional investors.

The decision is more interesting than it looks. An active exclusion by a mid-sized Danish fund does not move SpaceX's book. What it does is establish the benchmark question every investment committee will now face: if you would not buy this company at this price with this structure as an active decision, why will you own it as a passive one? Pre-IPO exclusion is the one moment where an indexed investor still has a choice — after inclusion, the choice is gone and only the tracking error remains. Expect the exclusion lists, and the carve-out requests to index providers, to grow between now and listing day.

Scenario Lab · A new interactive scenario every day SpaceX IPO Index Inclusion Risk — 45% desk probability  This is not a chart — it’s a live model you can get inside. Every morning the desk rebuilds it from sourced market, policy and flow signals, scores today's probability against a 35% historical base rate, today's signals putting it 10 points above that prior, confidence 3/10, and maps all 12 institutions, markets and risk factors it touches into a live relationship graph. Open it and the map responds: drag the network, click any player — SpaceX IPO, Market Volatility, S&P Index — and see exactly what it drives and what drives it. Then interrogate it: 6 vantage points sit inside the scenario — a sovereign wealth allocator, a pension CIO, a reinsurance underwriter, the markets desk — and each answers your questions in its own voice, grounded only in the scenario's research.

|

3. Private credit's pressure valve: secondaries volume doubles to $20 billion.

The private-credit story we tracked yesterday — the channel splitting over whether the asset class deserves a standalone allocation — has a liquidity chapter. In a June 8 analysis, Pensions & Investments reports that private credit secondaries volumes nearly doubled to $20 billion from 2024 to 2025, with GP-led volume tripling year over year to $12 billion (full-year 2025 figures — context, not a new announcement). The driver is not enthusiasm; it is exit demand. Semi-liquid private credit vehicles have been curbing withdrawals as redemption requests outrun liquidity, and scrutiny of business development companies is pushing more holders to look for an off-ramp at a negotiated price rather than a gated one.

For a long-horizon allocator, a maturing secondaries market cuts both ways. It is genuine infrastructure — duration and liquidity risk in private credit can now be managed mid-life rather than held to term, which makes the asset class more ownable for funds that mark liquidity honestly. But it is also a tell: pressure valves get built where pressure exists. The bid side of a $20 billion market is a real-time, arm's-length read on what private credit paper is actually worth — worth watching closely by any board still carrying the asset class at model marks.

Source: Pensions & Investments, "Private credit secondaries poised for explosive growth," June 8, 2026; CNBC, "Private credit's 'off-ramp' emerges as investors look to cash out," March 17, 2026.

— Chart of the day —

The $800 billion disagreement: SpaceX's ask vs. the first institutional answer.

Source: Pensions & Investments, June 8, 2026; AkademikerPension via Invezz, May 29, 2026. UAO Research, 2026.

— Take of the day —

"Index inclusion was designed to make ownership automatic; SpaceX is about to demonstrate that it also makes objection optional. When a company can raise the largest IPO in history from investors who call its governance reckless — and who buy anyway — the discipline is not coming from the share register. The funds that matter most own everything, which is precisely why this listing tests whether owning everything still means anything."

— UAO Research.

— Today's interactive scenario: SpaceX IPO Index Inclusion Risk —

This question is live in the Scenario Lab right now. Will SpaceX enter the major cap-weighted indexes within 30 trading days of listing, forcing indexed universal owners to buy? Drag the relationship map, click any node to see what it drives, and ask the scenario your own questions — answers come from the day's sourced evidence.

— Three links worth your time —

- Pensions & Investments — "Inside SpaceX's IPO filing: the red flags pension funds can't vote away." The filing-level detail behind the governance objections — what is actually in the structure, clause by clause.

- Fortune — "World's largest sovereign wealth fund backs push for Google oversight." NBIM voting against Alphabet management on AI oversight — the other live test this month of whether universal-owner stewardship moves outcomes.

- CNBC — "Why pension funds are doubling down on private credit despite deepening cracks." The allocation side of today's secondaries story — who is still adding, and why.

🎧 The Universal Owner — today's edition and the index-provider deep take, in your feed every morning. Follow on Spotify · All episodes

More from today: listen to The Universal Owner on Apple Podcasts or Spotify · watch the video briefing · the chart of the day.

Produced and edited by the UAO editorial desk. Editorial analysis for long-duration capital — not investment advice.