Today’s podcast Listen to The Universal Owner Our daily audio briefing for long-horizon capital — the same analysis, for your commute. Follow the show so every weekday episode lands automatically.

|

Volume 1, Issue 30. Wednesday, June 10, 2026. Sent 7:00 am ET / 15:00 GST.

|

On July 1 the largest public pension in the United States stops doing the one thing every pension is taught to do. CalPERS retires strategic asset allocation — fixed targets for each asset class — and begins judging itself against a single 75/25 reference portfolio under what it calls a total portfolio approach. Next week its board takes up the companion question of how to pay the people who will run it. That switch is the sharpest expression of a rethink moving through the whole public-pension channel, and it forces a question on every large allocator: does the total-portfolio model add return, or just move where discretion and accountability sit? Below: the switch, the pay rewire, the private-credit split it is meant to settle — plus the chart of the day and three links worth your time.

▶ Watch the video briefing

▶ Watch the video briefing1. CalPERS retires strategic asset allocation on July 1 — one benchmark replaces eleven.

On July 1, 2026, the roughly $598 billion California Public Employees' Retirement System — the largest defined-benefit public pension in the US, serving 2.4 million members (PERF assets as of March 31, 2026) — switches off the strategic asset allocation (SAA) model it has run for decades and turns on a total portfolio approach (TPA). Under SAA the board set a fixed target for each asset class and measured each against its own benchmark. Under TPA there are no asset-class targets: staff build the portfolio around which investments best contribute to the whole, judged against a single reference portfolio of 75% equities and 25% bonds in place of the eleven asset-class benchmarks used today. The discount rate is held at 6.8%. (The board voted to adopt the model on November 17, 2025; July 1 is the day it comes into force.)

For a universal owner this is not a California story. CalPERS is the first US pension to make the move, and it is the bellwether the rest of the channel watches. The deeper point is what TPA concedes: that the policy portfolio — the fixed allocation grid that has anchored institutional investing since the 1980s — may be the wrong unit of accountability when the risks that matter, from AI capex to energy to duration, cut across every box at once.

Source: CalPERS, "CalPERS Board Adopts Streamlined Investment Approach," Nov 17, 2025; PERF Monthly Asset Allocation Update, as of Mar 31, 2026. | Coverage: Pension Strategy Watch, this week.

2. The pay rewire comes to the board next week.

A model is only as good as the incentives behind it, and CalPERS knows it. At its June 15–17 board meeting the fund will weigh changes that tie more of its investment staff's pay to total-fund performance rather than to individual asset-class results — the compensation analogue of the TPA switch. Today most roles run on a 60/40 split between total-fund and individual performance; the fund's consultant, Global Governance Advisors, is finalizing recommendations in June that would push collaboration and total-fund outcomes deeper into the incentive structure, including adding "collaboration" as a performance metric for more junior investment staff from fiscal year 2026–27.

The read-across for any owner contemplating TPA is that the hard part is governance, not theory. Removing asset-class targets concentrates discretion in the investment team and removes the eleven separate scorecards a board could once point to. Replacing them with one number to defend only works if the people building the portfolio are paid to optimise that number — and if the board can still hold them to account when the single reference portfolio is missed.

3. The silo fight TPA is meant to settle: private credit splits the channel.

The case for abandoning asset-class targets is easiest to see where the channel cannot agree on whether an asset class belongs at all. Private credit is the live example. The Washington State Investment Board, which manages roughly $200 billion, is building a standalone private-credit allocation — an implementation plan is underway and the board is expected to decide the size this autumn. At the other end, the East Bay Municipal Utility District retirement system eliminated private credit entirely in March 2026, cancelling a manager search and citing lower expected returns and headline risk. The Financial Stability Board, in a May 6, 2026 report, flagged growing vulnerabilities in the asset class — leverage, opacity, and valuation lags.

Under SAA, that disagreement plays out as a fight over a target — 0%, 3%, 5% of the fund. Under TPA it becomes a fight over contribution: does a dollar of private credit, at today's spreads and liquidity terms, beat the next-best use of that dollar and the risk it adds to the whole? That is a harder question, and a more honest one. It is also the question CalPERS has just committed to answering every day rather than once every four years.

Source: Pensions & Investments, "Washington State Investment Board launches implementation plan for new private credit asset class," March 2026; FSB, "Vulnerabilities in Private Credit," May 6, 2026.

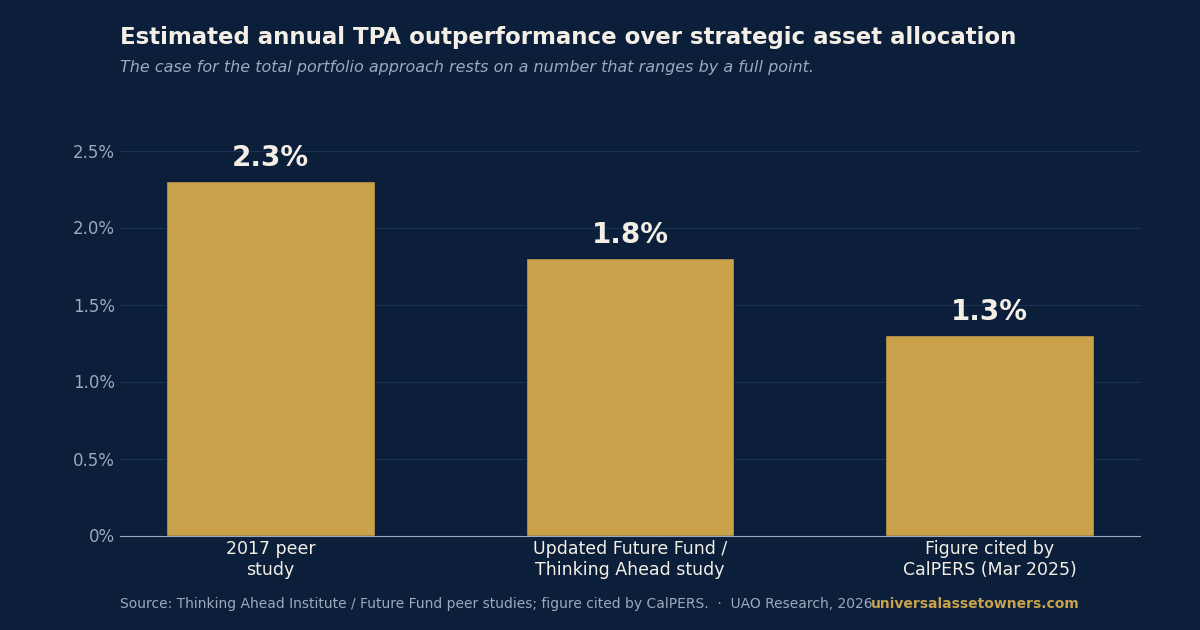

— Chart of the day —

The case for the total portfolio approach rests on an outperformance number nobody can pin down.

Source: Thinking Ahead Institute / Future Fund peer studies; figure cited by CalPERS (Mar 2025). UAO Research, 2026.

— Take of the day —

"TPA is less a return strategy than a governance bet. It trades eleven asset-class alibis for a single number to defend — buying coherence at the price of nowhere to hide. The funds it has worked for were already the best-governed in the world, which is exactly why CalPERS' real test is not the model but the pay packet it sets next week."

— UAO Research.

— Three links worth your time —

- CalPERS — "CalPERS Board Adopts Streamlined Investment Approach to Seize Market Opportunities." The primary document — the board's own framing, the 75/25 reference portfolio, and the 6.8% discount rate, in one page.

- Thinking Ahead Institute — Total Portfolio Approach hub. The peer-study research behind the outperformance claim — and the place to judge how robust the number really is.

- Financial Stability Board — “Vulnerabilities Associated with Private Credit,” May 6, 2026. Why the asset class CalPERS will now size by contribution is the one regulators are watching most closely.

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Universal Owner · view the chart of the day.

Produced and edited by the UAO editorial desk. Not investment advice.

Scenario Lab · A new scenario every day  The Strait of Hormuz Scenario — 56% desk probability Chokepoint concentration as a standing factor (Hormuz + Taiwan + Malacca + Panama) Open the interactive relationship map to see how the risk transmits through markets and portfolios — then put your own questions to the desk from the seat of a CIO, insurer or board member.

|

More from today: listen to The Universal Owner on Apple Podcasts or Spotify · watch the video briefing · the chart of the day.

Produced and edited by the UAO editorial desk. Editorial analysis for long-duration capital — not investment advice.