The 60-Day Window — our weekly cinematic film on this report. 4 min.

By Obaid ur Rehman | Researched and edited by the UAO editorial desk

The most important market signal in the U.S.–Iran interim framework is not the word “peace.” It is the word “license.”

Washington’s temporary 60-day sanctions waiver allows the sale, delivery and movement of Iranian crude oil, petroleum products and petrochemicals through August 21. It also authorizes associated services including banking, insurance and transportation. In legal terms, that is a major concession. In market terms, it gives traders a reason to price more oil supply, lower shipping risk and a smaller geopolitical premium across energy.

But for universal asset owners, the harder question is not whether Iran can legally sell more oil for 60 days. The question is whether the world’s most important energy corridor can become commercially normal again. That is a much higher bar.

A legal waiver does not by itself make a tanker owner comfortable. It does not make marine insurers permanently reduce war-risk premiums. It does not make banks certain they can clear payments without future sanctions exposure. It does not make Asian refiners rewrite existing supply books. It does not resolve Lebanon, Hezbollah, Gulf security, frozen assets, missile risk or the basic question of whether all sides interpret the framework the same way.

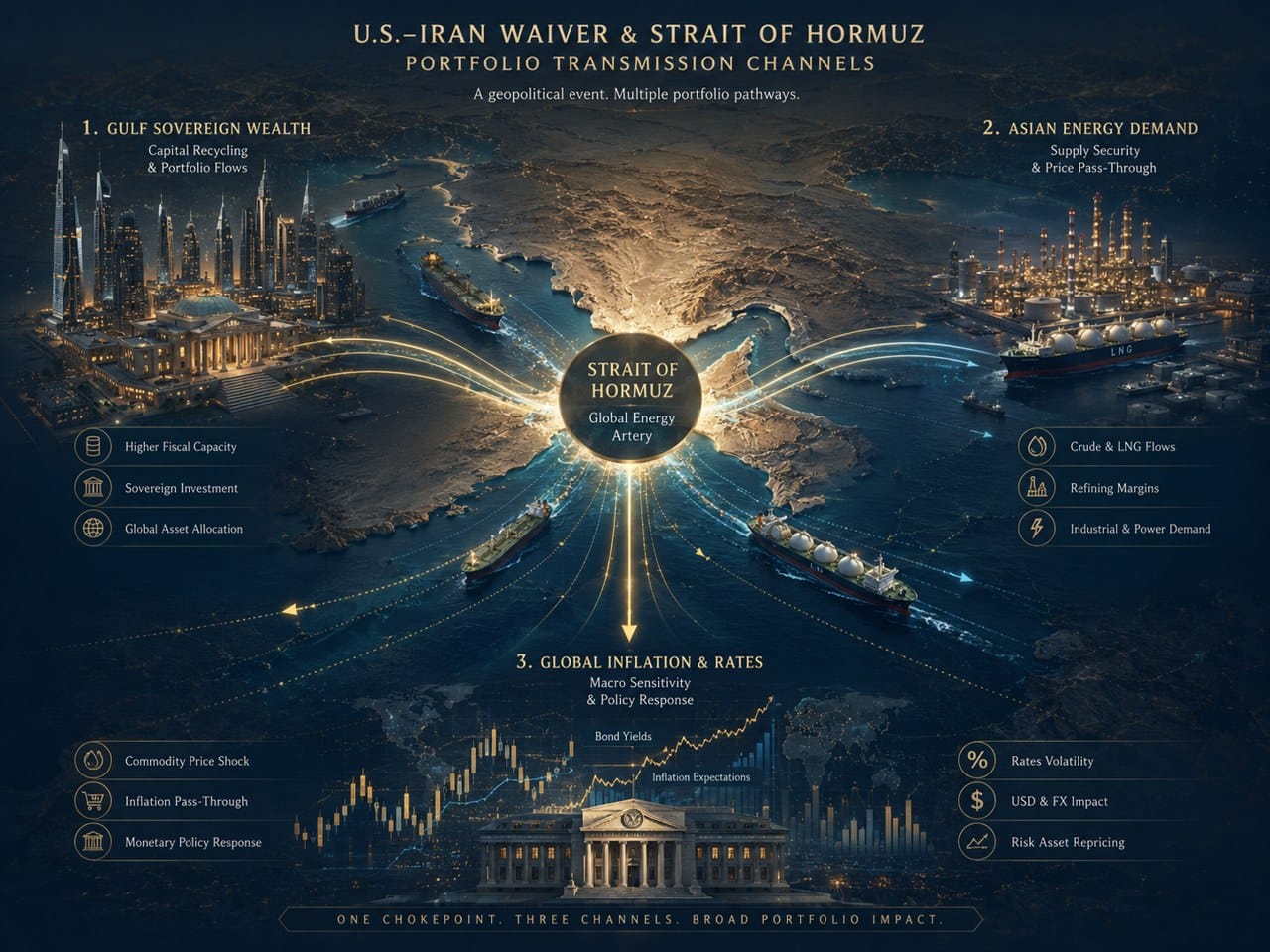

The Strait of Hormuz is not just a maritime route. It is a global discount-rate variable.

Roughly one-fifth of global petroleum liquids consumption and about one-fifth of global LNG trade move through Hormuz. When that corridor is impaired, the impact does not remain inside energy markets. It reaches inflation expectations, central-bank policy, sovereign revenues, airline margins, shipping insurance, emerging-market current accounts and long-duration asset valuations. The real lesson is deeper than any single headline: geopolitical risk is no longer an external shock to portfolios. It is part of the operating system of global capital.

The market wants to price de-escalation

The immediate logic is simple. If Iranian oil returns to visible channels, supply increases. If tankers move more freely, the war premium falls. If energy prices decline, inflation pressure eases. If inflation eases, central banks have more room to cut. If discount rates fall, long-duration equities, infrastructure, real estate and credit all benefit. That is the bullish reading — and it is incomplete. The market can remove a risk premium faster than the physical and financial system can normalize. A barrel is not truly back simply because it is legally saleable. It has to be lifted, insured, financed, shipped, received, paid for and politically tolerated after delivery. Each step carries risk. The waiver should be treated as an option, not a settlement: it gives the market the right to price lower risk; it does not prove lower risk has been earned.

Open is not the same as insurable

For asset owners, the most useful distinction is between three states of Hormuz. The first is legal openness — what the waiver attempts to create. The second is physical openness — ships can actually move through the strait in both directions at close to normal volumes. The third is commercial normality — shipowners, insurers, banks, refiners and state buyers all believe the route is safe and durable enough to price as ordinary commerce rather than a temporary exception. Universal owners should care most about the third. The global economy can live with temporary legal relief; it cannot fully reprice energy risk unless Hormuz becomes commercially normal.

That is why renewed attacks around the strait matter so much. A tanker strike or drone attack does more than damage one vessel. It tells insurers, banks and boards that the corridor is still politically contested. It makes every buyer ask whether the discount on Iranian crude is compensation for price, or compensation for operational and sanctions risk.

The investable signal is not just Brent. It is the spread between Brent and trust.

Why this matters for the owners of the world

A hedge fund can trade the oil headline. A universal owner owns the system the headline affects — through inflation-linked liabilities, government bonds, infrastructure, private credit, equities, real estate and currency translation. For Gulf sovereign funds the effect is especially two-sided. De-escalation supports tourism, logistics, capital-market confidence, FDI and diversification, and lowers the probability that shipping insurance or a regional blockade disrupts national plans. But lower oil prices can also reduce fiscal flexibility. If Iranian supply helps push Brent below fiscal comfort levels for long enough, governments may have less room to fund domestic megaprojects and global expansion at the same pace. Gulf funds do not stop investing — the marginal dollar becomes more selective. For owners co-investing alongside Gulf capital, selling assets to Gulf buyers, or depending on Gulf-backed infrastructure, that matters.

Asia is the real demand-side story

The U.S.–Iran label makes this look bilateral. It is not. China has been the dominant buyer of Iranian oil under sanctions, largely through independent refiners, intermediaries and non-dollar structures. India was historically a major buyer before sanctions pushed it away. Japan and South Korea have energy-security interests even if they move more cautiously. Qatar’s LNG through Hormuz matters directly for Asian utilities and industry. If supply returns smoothly, Asian refiners gain bargaining power and current accounts improve. But if Hormuz remains unsafe, Asia faces the worst version of energy insecurity: lower legal risk on paper, continued physical and insurance risk in practice. That false comfort is dangerous — markets may price relief before supply chains are actually resilient.

The nuclear calendar is the duration of the trade

The waiver runs through August 21. But the true duration depends on the nuclear-inspection process. If IAEA access becomes credible, intrusive enough to satisfy Washington and acceptable enough for Tehran to survive domestic politics, the waiver can become the beginning of a broader reset and a more durable reduction in the energy risk premium. If inspection access becomes symbolic, disputed or delayed, the waiver becomes a tactical pause. Oil may still move and discounts may still be offered, but long-horizon investors should not treat the macro regime as changed. Without duration, the market is not repricing peace. It is renting de-escalation.

The sectors that reveal whether the deal is real

Several sectors will reveal whether the framework is becoming real. Marine insurance is the market’s real-time confidence vote: if war-risk premiums fall and stay down despite periodic incidents, commercial actors are treating the route as manageable. Banking and trade finance — a waiver is only as useful as the banks willing to process payments; watch whether mainstream banks participate or transactions stay concentrated in intermediaries and non-dollar settlement. Shipping — composition matters more than volume; a few high-risk operators is not broad-based normalization. Asian refinery behaviour — large state refiners signing direct cargoes is a stronger signal than small intermediaries. OPEC+ — Saudi Arabia, Iraq, Kuwait, the UAE and Russia will respond through pricing or discipline. And LNG may be the more important systemic signal for Asia than crude.

Stop treating geopolitics as an overlay

The lesson is not to forecast whether the framework succeeds. It is to underwrite portfolios against the failure of any single geopolitical path — treating chokepoints as structural portfolio variables. Hormuz is one. The Red Sea, the Black Sea, the Taiwan Strait, the Panama and Suez canals, Bab el-Mandeb and the South China Sea play similar roles elsewhere. They are not discrete shocks; they are correlated with inflation, central-bank policy, shipping costs, food prices, energy security, sovereign credit and private-market valuations. A universal owner cannot diversify away from the global economy. The right question is not “Will the Iran deal hold?” It is “What does our portfolio assume about chokepoint normality?” If the answer is “not much,” the portfolio may carry more geopolitical beta than the board realizes.

Scenarios for the next 60 days

Base case — fragile normalization. The waiver holds; some Iranian barrels move; Chinese buyers absorb more than others; Indian refiners test the market but stay constrained; Hormuz traffic improves but does not fully normalize; part of the war premium stays removed. Upside — commercial normalization. Credible IAEA access; near-normal two-way tanker traffic; insurance premiums fall and stay down; mainstream banks process payments; large Asian refiners resume direct purchases; OPEC+ manages the supply impact. Downside — waiver without trust. Oil is legally saleable but buyers hesitate, payments stay uncertain, premiums stay elevated, incidents continue, and markets price relief then reverse it. Tail — false reopening. Legally open but commercially unsafe; a major incident disrupts flows; oil and LNG spike together; central banks lose the inflation relief they had begun to price. The tail is not the forecast — but it is the case universal owners must own, because they cannot exit the system.

The bottom line

The U.S.–Iran waiver matters because it tests whether diplomacy can lower the world’s energy risk premium. But the real lesson is not that peace is here. It is that legal permission, physical access and commercial confidence are three different things. Markets can trade the first; energy systems require the second; universal owners need the third. The next 60 days should be watched less like a diplomatic ceremony and more like a stress test of the global operating system. The world’s most important 60-day trade is not Iranian oil. It is trust in the corridor that moves it.

Obaid ur Rehman is a contributing journalist at Universal Asset Owners covering geopolitics, China’s strategic expansion, and the South and Central Asian capital corridors that define long-term institutional risk. Editorial analysis — not investment, legal or financial advice.