Today's video briefing — Hormuz: open on paper, closed in practice (97s).

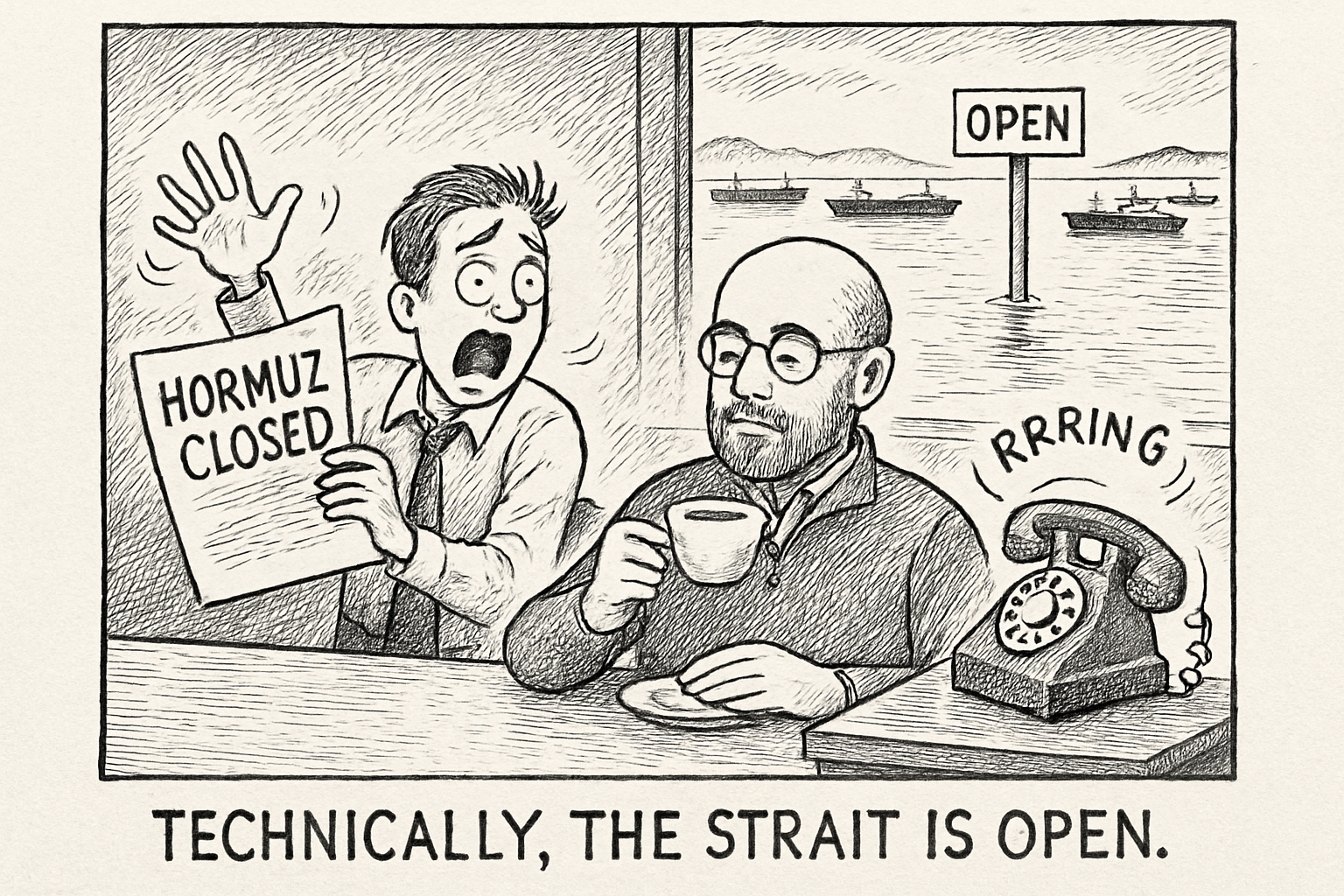

Hormuz is open on paper. In practice, it is partly closed.

The Strait of Hormuz did not shut this weekend so much as slip into a more dangerous condition: a passage technically available but increasingly difficult to use. Iran's Revolutionary Guard declared the strait closed “until further notice” on Sunday after firing on a vessel it accused of travelling along an unapproved route. U.S. Central Command insisted that freedom of navigation still prevailed, after conducting another wave of strikes against Iranian air defences, coastal radars and missile sites.

Maritime authorities describe a more complicated operational reality. The southern route through Omani waters remains available, but the Joint Maritime Information Center rates the threat as “severe,” while a mine-danger area remains in the established traffic-separation scheme. JMIC says there is no recognized authority administering commercial passage or requiring vessels to pay for transit.

An asset can remain technically available while becoming economically, operationally or politically unusable. Only six vessels crossed on Sunday, the fewest in roughly five weeks, according to Kpler data reported by Reuters. Most tankers operating in the high-risk zone had switched off their transponders, and no LNG carrier was detected transiting over the weekend.

Iran also said it had electronically disabled two ships. It provided no vessel names or supporting evidence, and the assertion has not been independently confirmed.

Iran does not need to establish an official toll to impose costs on the corridor. Insurance exclusions, war-risk premiums, charter rates, crew refusals and delays already function as a private-sector toll. The United States may be able to keep a route technically available, including through naval protection, without compelling owners, insurers or crews to use it.

The counterargument is real. Alternative pipelines, inventory drawdowns, spare OPEC+ capacity, softer demand and naval protection have so far prevented the catastrophic shortfall once feared. Brent traded around $79 early Monday, up approximately 4% from Friday, suggesting that markets still expect the disruption to remain manageable.

Our working interpretation is that markets may be underpricing the disruption's duration rather than its direction. That thesis would be weakened by a rapid recovery in LNG crossings, falling war-risk premiums and a sustained return toward normal traffic volumes.

The IMF's July forecast provides useful context. Its baseline assumes that reopening begins in mid-July, with conditions returning broadly to their prewar state by March 2027. That is a modelling assumption, not an operational prediction.

A volume equivalent to roughly one-fifth of global petroleum-liquids consumption passes through Hormuz, alongside approximately one-fifth of global LNG trade. You can underweight a company. You cannot easily underweight a chokepoint already embedded throughout your portfolio.

The corridor war has a second front

A Ukrainian drone struck a tanker as it entered the Azov–Black Sea canal on Saturday. Russian authorities said the vessel was empty, the resulting fire was controlled and no spill occurred.

Ukraine's drone-force commander said approximately 90 Russian-linked vessels had been targeted in less than a week. That figure has not been independently verified and should be understood as Kyiv's claim.

Two chokepoints, one lesson: the risk premium is migrating from the barrel to the hull, the crew and the insurance contract.

Iraq starts designing an energy system that assumes Hormuz can fail

Iraqi Prime Minister Ali al-Zaidi is due in Washington, where oil-and-gas agreements are expected to be signed as part of a broader push for economic and investment cooperation.

Iraq is also pursuing alternative export outlets, including routes through Syria, as it seeks to reduce its exposure to disruption in Hormuz. The conflict is accelerating the re-plumbing of energy trade, turning pipelines, storage, alternative ports and interconnections into national-security assets.

That creates potential opportunities for sovereign funds, infrastructure managers and development institutions—but also stranded-asset risk if emergency routes are financed using overly optimistic assumptions. The Washington agreements are expected, but had not been signed at publication time.

The AI-power trade meets a physical stress test

A new heat dome is forecast to push AccuWeather RealFeel temperatures as high as 105–115°F across parts of the Plains and Midwest this week, with dangerous heat extending farther east.

It will test an already strained electricity system. PJM, which serves approximately 67 million people across 13 states and Washington, recorded balancing costs of $217 million in the first quarter, up 215% year over year. During the previous heat wave, balancing prices briefly approached $28,000 per megawatt-hour.

Recent federal emergency orders have also allowed PJM, under specified emergency conditions, to call on backup generation at large electricity users and operate certain power plants beyond normal restrictions. Transmission congestion has affected multiple areas, including the Northern Virginia data-centre corridor.

A portfolio simultaneously long hyperscalers, data centres, utilities and grid infrastructure—and exposed to consumer bills and regulatory intervention—may contain one concentrated theme masquerading as several diversified allocations.

Asset-owner moves

Qatar loses an architect of its modern sovereign model—but not its ruler. Former Emir Sheikh Hamad bin Khalifa Al-Thani died Sunday at 74. He transferred power to his son, current Emir Sheikh Tamim bin Hamad Al-Thani, in 2013, so his death does not create a succession crisis.

It nevertheless marks the passing of the leader under whom Qatar transformed its LNG wealth into a sovereign balance sheet, global investment platform and source of diplomatic influence. His legacy is also a reminder that well-built sovereign institutions can outlast their founders.

Watch — a policy signal, not yet a policy

EU weighs curbing settlement trade. EU foreign ministers meet Monday to consider three possible approaches to trade involving Israeli settlements in the occupied West Bank: an import-licensing system, prohibitive tariffs or an outright ban.

No decision is expected. Member states also disagree over whether a measure would require a qualified majority or unanimity.

Implementation could force asset owners to determine where economic activity actually occurs—and whether applicable legal screens extend to trade, procurement, portfolio securities or some combination of the three.

Sponsor · AssetOps Chicago

Where U.S. operations leaders turn transformation into execution. Join senior buy-side operations, technology, data and transformation leaders at AssetOps Chicago on August 11. Explore practical strategies for operating-model transformation, AI, private markets and operational resilience through candid, peer-led discussions. Complimentary VIP registration is now available. Register free →

Today’s scenario · The Corridor That Stops Reopening

The desk assigns approximately 60% probability to the corridor remaining contested and only partly usable through the third quarter. Open the interactive scenario →

Listen — The Universal Owner

Today’s episode: The private toll — how a strait gets closed without being closed.

Subscribe: Apple Podcasts · Spotify — sponsored by AssetOps Chicago by Corinium.

Universal Asset Owners — Institutional Membership

For investment teams that need a continuous research relationship. Premium research, probability-weighted scenario analysis, weekly research calls, reasonable-use editorial Q&A and board-ready briefings for sovereign funds, pensions, endowments, family offices and institutional allocators.

The private toll: how a strait gets closed without being closed

Control of a strait once meant physically closing it. The lesson of this weekend is subtler: a state may be able to make a waterway commercially unusable without preventing every vessel from passing.

Iran fired on a vessel, declared Hormuz closed and claimed to have electronically disabled two ships. The United States declared the strait open and continued protecting traffic. Those positions can coexist because what governs a commercial corridor is not simply a military declaration. It is the willingness of shipowners, insurers, charterers and crews to enter it.

That willingness is priced privately. War-risk coverage is repriced, restricted or withdrawn. Charterers demand hazard premiums. Crews may refuse routes. Underwriters add exclusions.

The result is an economic toll imposed by insecurity, even without an official charge—and one that Washington cannot abolish merely by declaring the strait open.

Only six vessels crossed on Sunday, and no LNG carrier was detected transiting over the weekend. If that persists, the binding constraint on Asian energy security, Gulf sovereign cash flows and the inflation outlook may be not the availability of the commodity, but the availability of ships, insurance and willing crews.

The market's current signal is comparatively restrained: Brent rose approximately 4% rather than pricing an immediate catastrophic shortage. But operational data points to a corridor whose availability remains conditional and contested.

When financial pricing implies a brief disruption while operating data shows persistent impairment, universal owners should monitor both.

The indicators to watch are not limited to the oil price. Watch LNG crossings, war-risk insurance capacity, charter rates and the number of owners willing to transit.

Federal Reserve references reflect Kevin Warsh, who became chair in May 2026. Signal provenance: July 11 onward verification; live signal snapshot. The desk's simulation leg carries zero published weighting and is used only as an internal tool, not as external validation.

with The Allocator

Comfortable with our positioning. A lighter look at the institutional week, from the desk of a man who owns a slice of everything and is pitched by everyone.

The Allocator · "The Raise" (41s)

Follow The Allocator — launching this week.