UAO Daily Brief — Thursday, July 2, 2026

Build the CIO, or Rent One?

Intelligence for long-horizon capital. Vol. 1 · Issue 50 · Franchise: Capital Flow Watch Subject line: "The $8bn question: build the CIO, or rent one?"

Today: The world's largest owners aren't just changing portfolios — they're choosing operating systems. CalPERS is building investment judgment inside the fund; British Coal is renting it from BlackRock; Gulf sovereigns and Washington are contesting the AI cap table; and reserve managers are re-routing the pipes beneath the dollar. The question is no longer only what they own. It's who controls the judgment, the votes, the plumbing, and the strategic upside. State-owned investors now steer $62.5tn — $16tn in sovereign funds, $28tn in pensions, $17.6tn in central banks and $0.9tn in royal family offices (Global SWF) — and every one of them is answering that question this week.

1 — The Governance Divide: CalPERS builds the CIO; British Coal rents one

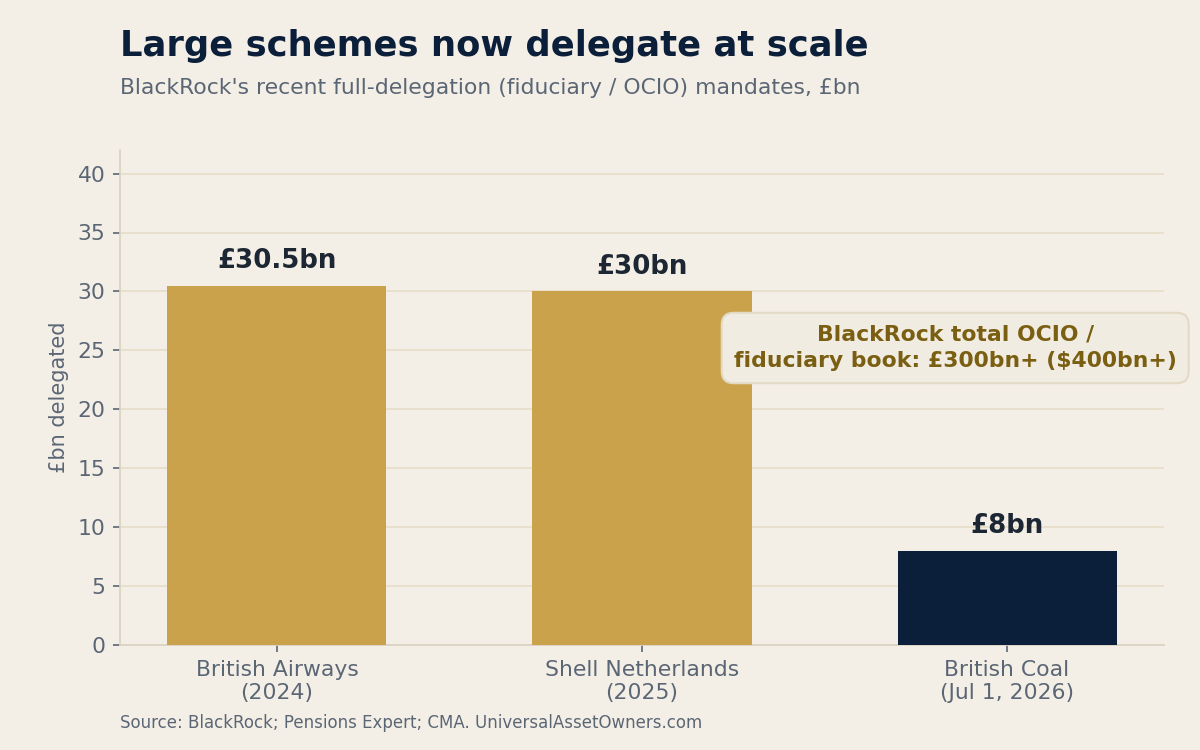

On July 1, CalPERS' Total Portfolio Approach went live — America's largest public pension ($556bn) moving off 11 asset-class benchmarks toward a single total-fund reference portfolio, staff judged on contribution to the whole fund. The same day, the £8bn British Coal Staff Superannuation Scheme (~39,000 members) named BlackRock its fiduciary manager. One fund is formalizing internal judgment; the other is deciding an internal model is no longer the answer. And a third answer landed a day earlier: QIA, alongside Trian and General Catalyst, closed the $7.4bn take-private of Janus Henderson on June 30 — the sovereign buying the manager outright.

Read the delegation precisely: BlackRock runs the money day-to-day within parameters, while trustees keep full control of strategy and risk (BlackRock; BCSSS). BlackRock already managed £2bn+ for the scheme — this takes it to the full £8bn. Full fiduciary delegation was historically a sub-£1bn solution (per the UK CMA); an £8bn scheme delegating is the model moving up-market, into a BlackRock outsourced book now past $400bn / £300bn (alongside British Airways $30.5bn, Shell's Dutch plans $30bn).

For a universal owner the sharper question isn't "who runs the portfolio?" but "who votes it?" As one manager runs more of the index, ETF, private-markets, risk (Aladdin) and stewardship stack, delegating implementation can mean delegating market voice — live, given BlackRock's climate-stewardship pushback (NYC's index rebid; PFZW's partial exit over its voting record, per Reuters). And the downside isn't purely private: British Coal's benefits carry a statutory Government Guarantee — taxpayer backstop, private execution, trustee accountability.

In fairness, British Coal may be right. Closed to new members since 1994 and maturing, its job is disciplined management of cash flows and funded status toward an endgame — a mandate a scaled fiduciary with LDI machinery may serve better than a small in-house team. The old middle model — a part-time board, a consultant deck, quarterly meetings — is simply breaking; the future is a real internal investment office or a real external one.

2 — The State Enters the AI Cap Table

Two moves this week say frontier AI has outgrown normal private markets. From the outside, Abu Dhabi's MGX (anchored by Mubadala and G42) closed MGX Fund 1 at $49bn, above its $45bn target — invested across ~14 companies in semiconductors, AI infrastructure and enabling platforms, having backed Anthropic, OpenAI and xAI. Gulf sovereigns aren't cornering the stack; they're buying bargaining power across it. Total Gulf deployment hit a record $53.9bn across 108 deals in H1 (Mubadala first at $15.2bn; ~half into the US), and Saudi Arabia's PIF reported 2025 assets up 5% to $1.21tn.

From the inside, the AI company is inviting the state onto the cap table: OpenAI has proposed handing the US government a ~5% stake (~$42.6bn at its ~$852bn valuation) — donated equity to seed a "Public Wealth Fund," part of a framework in which Washington would hold 5% of leading US AI developers (FT, via Bloomberg/CNBC; no final terms). MGX buys the stack from outside; OpenAI offers it to the state from inside. Together: AI is becoming public-strategic infrastructure, not just venture-backed tech.

The structural backdrop: global M&A hit a record $2.8tn in H1 (+48% YoY) even as deal count fell to a six-year low — ~47 deals above $10bn drove nearly half the value (LSEG). The market is consolidating into mega-transactions only apex allocators can swallow. The middle is hollowing in deal flow, too. The tension worth naming: sovereigns are deploying most aggressively just as the Hormuz reopening (below) pulls oil toward $70 and thins the surpluses that fund the buying.

3 — Resilience Replaces Returns — and Re-routes the Pipes

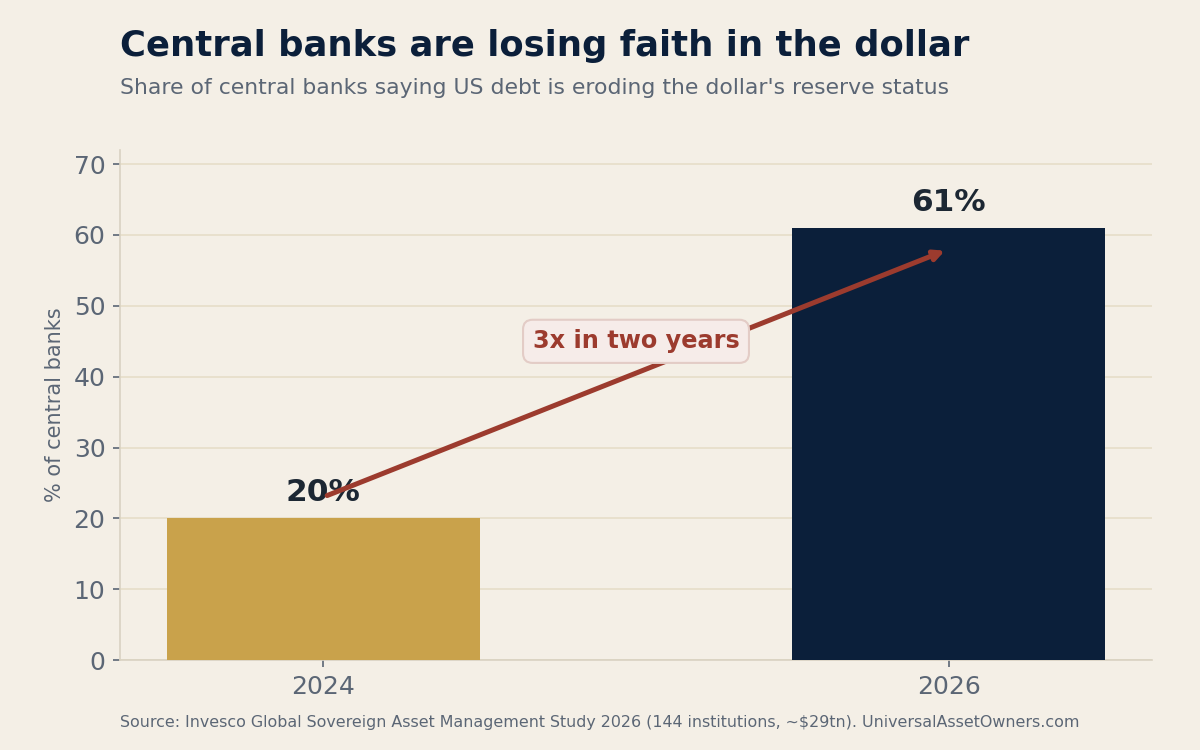

The Invesco Global Sovereign Asset Management Study (144 institutions — 90 SWFs + 54 central banks — ~$29tn) captures the shift: 61% of central banks say US debt is eroding the dollar's reserve status — up from 20% in 2024; a third of sovereign investors plan to raise gold; 80% cite energy security and transition infrastructure as the top resilience play; infrastructure is now 9% of SWF assets. Private capital agrees: the UBS Global Family Office Report finds 47% of family offices feel overexposed to the dollar and 65% expect its reserve status to weaken. And resilience is no longer only about currency weights — Reuters reports some reserve managers are reviewing reliance on US custodians and clearing infrastructure. The reserve question is shifting from "what currency do we hold?" to "whose pipes do we need to pass through to use it?"

The fragility went live in 48 hours. A Bloomberg-reported Meta plan to sell access to idle AI compute raised a new fear — that the AI bottleneck could flip from scarcity to overcapacity — and chips sold off worldwide (Samsung −7.7%, SK Hynix −9.3%); Korea's Kospi closed down 6.3% below 8,000, and the Korea Exchange suspended program selling (a "sidecar") after a sharp drop in Kospi futures. Simultaneously, the US–Iran ceasefire and reopening of the Strait of Hormuz erased crude's war premium — Brent back toward ~$72 from a late-April spike above $126 — with Morgan Stanley modeling a 4.8m bpd oil surplus in 2027. The BIS, in its June Annual Economic Report, framed the backdrop: a disconnect between elevated equity valuations and spiking geopolitical risk, and $1tn+ of debt-funded AI capex. AI has moved from the CIO's opportunity set to the central banker's risk register (a dominant theme at the ECB's Sintra forum this week).

What to watch: - The new floor for full delegation — if £8bn schemes delegate, watch the next; the OCIO market re-rates upward. - Stewardship concentration — as one manager votes more of the market, scrutiny rises. - The AI-ownership question — does Washington take equity in frontier AI, and do other states follow? - The oil/fiscal squeeze — can record sovereign deployment survive $70 oil? - Who can move when rates stay higher — the governance model that matters is the one that can actually rebalance under stress, not the one that looks clean in a policy deck.

Chart of the day: OCIO moves up-market — largest known full-fiduciary mandates by scheme size (British Coal £8bn vs. the historical sub-£1bn norm), alongside BlackRock's $400bn+ outsourced book. (chart-ocio-2026-07-02.png)

Sources: BlackRock (July 1, 2026) & BCSSS; Pensions Expert; Professional Pensions; CIO; CMA Order 2019; Reuters (BlackRock stewardship / NYC / PFZW; reserve custody). QIA / Janus Henderson / Business Wire (take-private closed June 30, 2026). Global SWF / The National ($62.5tn state-owned universe; Gulf $53.9bn H1). CNBC / The National (MGX $49bn). Arab News (PIF $1.21tn). FT via Bloomberg / CNBC (OpenAI 5% US government stake). LSEG / Bloomberg (M&A $2.8tn H1). Invesco Global Sovereign Asset Management Study 2026; UBS Global Family Office Report 2026; BIS Annual Economic Report (June 2026); Reuters (ECB Sintra). Reuters / Morgan Stanley (US–Iran ceasefire, Hormuz, 4.8m bpd 2027 surplus). Bloomberg / KED Global / CNBC (Meta compute; Kospi −6.3%, sidecar, July 2).