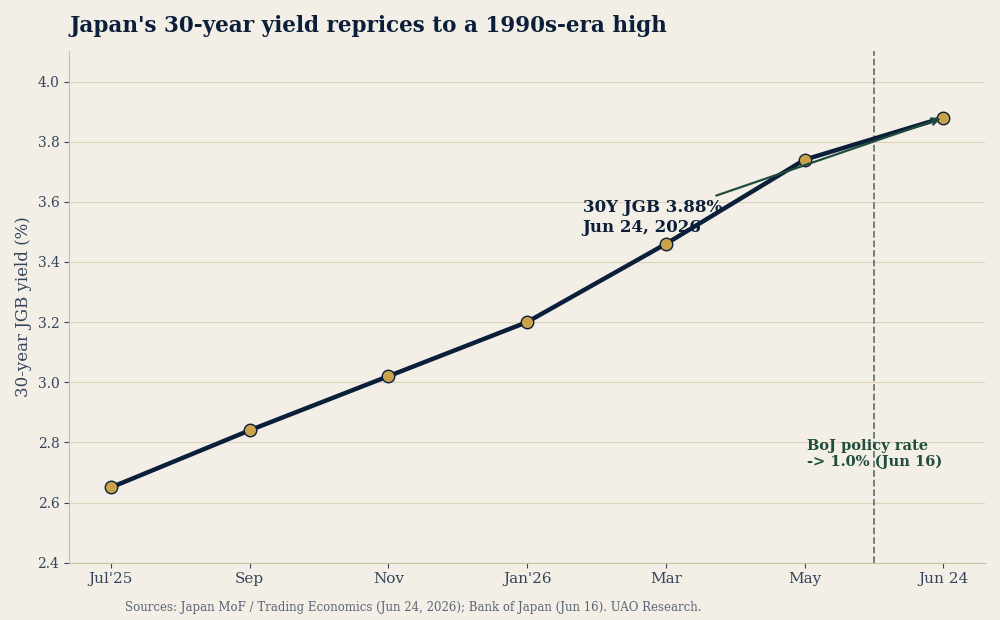

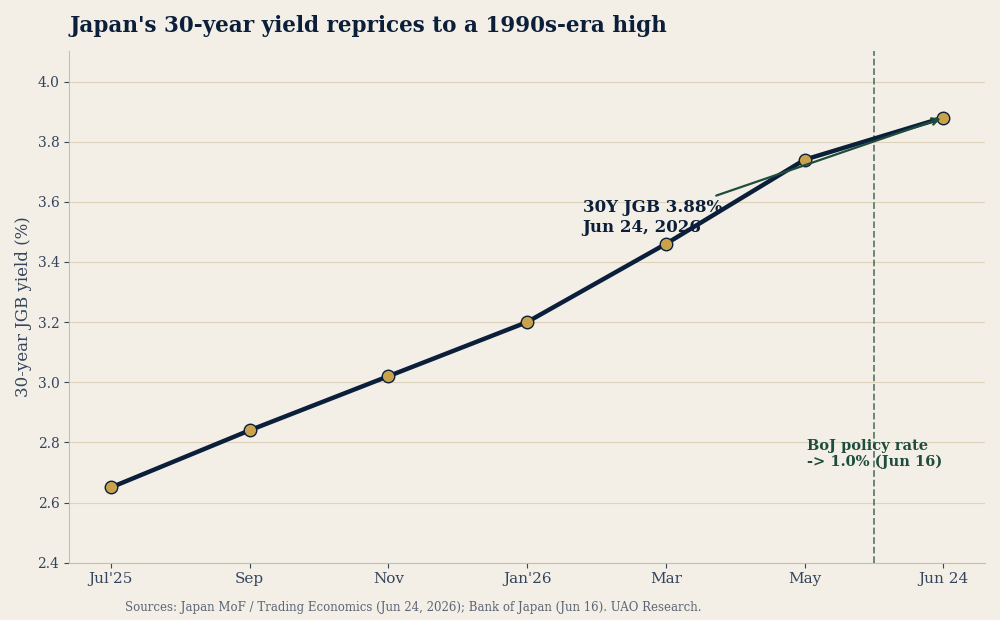

For thirty years, the cheapest money in the world came from one place. Japan held its policy rate at or below zero while the rest of the planet borrowed yen, sold them, and bought everything else — the carry trade that quietly financed risk in every time zone. On June 24 the 30-year Japanese government bond closed near 3.9%, an effective 1990s-era high, eight days after the Bank of Japan lifted its policy rate to 1.0% (from 0.75%). When one of the world's largest creditors can finally earn a real yield at home, the marginal yen comes home with it — and the discount rate on every long-dated asset a universal owner holds resets higher. This is not a Tokyo story. It is the end of cheap global liquidity.

1. Japan's rate shift: the end of cheap global money.

The 30-year JGB near 3.9% and a 1.0% policy rate, up from 0.75% — the highest since the mid-1990s — are repricing the single most important funding source in global macro. As long-dated yen yields rise, the yen-funded carry trade that underwrote leverage worldwide becomes more expensive to run, and Japanese capital that bid long-dated Treasuries and global credit has reason to stay home. Against that backdrop, lawmakers have floated folding the $1.3tn in FX reserves, the BoJ's ETF holdings and pension assets — roughly ¥500tn ($3.2tn) — into a sovereign wealth fund chasing higher returns; officials are already pushing back on touching reserves held for intervention. Either way, the direction is set: the global term premium resets higher, lifting the discount rate on every long-dated asset an owner holds.

So what for owners: Re-underwrite anything whose return leaned on cheap funding — yen carry, levered carry sleeves and long-duration illiquids financed short reprice first as the global discount rate rises.

Sources: Trading Economics / Japan MoF (30Y JGB, Jun 24, 2026); Reuters draft growth-strategy report & Nikkei Asia (SWF debate), Jun 23–24; Bank of Japan (policy rate, Jun 16).

2. The sovereign secondary wave: GIC, ADIC and CIC force a re-pricing of private markets.

With IPOs and M&A exits sluggish, fund stakes bought for long horizons are sitting on balance sheets past their welcome — so the largest sovereign owners are taking matters into their own hands. Industry tracker Global SWF reports GIC (Singapore), ADIC (Abu Dhabi) and CIC (China) among funds using the secondary market to actively sell private-equity and venture stakes. GIC alone has been running an LP-led process (reported as ‘Project Royal Eagle’) of up to ~$3bn (on roughly $5.5bn of original commitments), buyout-heavy and concentrated in North America, with underlying names reported to include Apollo, Bain Capital and Blackstone funds. When the world's most patient capital sells early, it sets a public clearing price for illiquid assets — and every pension and endowment marking a private book has to take notice.

So what for owners: Treat these sovereign secondary prints as a live mark on your own private book — pressure-test your carrying values against where peers are actually clearing, before a transaction sets the price for you.

Sources: Global SWF roundup (June 2026); Pensions & Investments and DealStreetAsia (GIC LP-led process, up to ~$3bn; reported 2025).

3. The AI capex collision: data centers as the new inflation engine.

The demand is real — Micron's record June-24 print (revenue $41.5bn, ~85% gross margin, a data-center run-rate above $100bn, supply tight beyond 2027 with multi-year take-or-pay agreements) is the hardest evidence yet that the roughly $700bn of 2026 hyperscaler capex has contracted buyers behind it. But the same build-out is now a macro force: Morgan Stanley flags a roughly six-fold rise in memory prices over the past year and warns “chipflation” is spreading from the data center into the wider economy, with US electricity up about 6% year-on-year. For a universal owner this is one exposure wearing three hats — equity concentration, AI-linked credit, and an inflation impulse that feeds straight back into the rate story above.

So what for owners: You can't hedge this with a single sector trade — size your true AI exposure across equities, credit and the inflation it feeds, because all three sit in the same names.

Sources: Micron fiscal Q3 2026 results & CNBC (Jun 24); BNN Bloomberg / Morgan Stanley “chipflation” (Jun 3); industry capex estimates, 2026.

4. NATO's 5% shift: a multi-decade fiscal and infrastructure regime.

Secretary-General Mark Rutte met President Trump at the White House on June 24 to ease alliance tensions before July's leaders' summit in Ankara, with burden-sharing front and centre. The backdrop is the agreed target of 5% of GDP on defence and security by 2035 — 3.5% core military plus 1.5% resilience and infrastructure. For long-horizon owners this is a structural, decade-plus stream: rising defence and dual-use industrial spend, heavier sovereign issuance to fund it, and a durable thematic tilt across defence, infrastructure and critical supply chains.

So what for owners: Read it as a decade-long spending stream, not a headline — a durable tilt toward defence, dual-use industrials and the sovereign issuance that funds them.

Sources: NATO (5% commitment); Modern Diplomacy / Reuters (Rutte–Trump, Jun 24, 2026; Ankara summit in July).

5. China's liquidity plumbing: the PBOC adds an overnight lever.

The People's Bank of China will conduct overnight reverse repos on June 29–30, the next step in Governor Pan Gongsheng's shift toward a price-based framework anchored on a short-term rate. The aim is to damp the money-market swings that periodically spook institutional investors and make onshore yuan bonds less attractive versus dollar and euro alternatives. Quiet plumbing, but it matters to reserve managers and global fixed-income allocators weighing China exposure: a more predictable overnight rate is a precondition for treating RMB bonds as core, not tactical.

So what for owners: A steadier onshore overnight rate is the precondition for treating RMB bonds as a core (not tactical) reserve allocation — watch whether the plumbing actually damps money-market volatility.

Source: Bloomberg (PBOC overnight reverse repo, Jun 25, 2026).

MARKET BULLET · OIL. The war risk-premium has largely unwound: US Energy Secretary Chris Wright told the Reuters Global Energy Forum that ~20 million barrels exited the Strait of Hormuz in 24 hours, and Brent fell more than $3 toward pre-war levels as flows normalise, though full normalisation may take time. Tactical for now, but it pulls the near-term inflation impulse the opposite way from the AI build-out above. (Reuters / Baird Maritime)

Built today and live now: an interactive map of how a Japanese rate shift drains cheap funding from the system — tightening carry, lifting the global term premium, and meeting an AI build-out that is itself an inflation source. Click any player — a pension CIO, a private-credit lender, a chief risk officer — and ask the desk what they do next.

Open the live scenario →The sovereign secondary wave is a governance question as much as a liquidity one. When the most patient owners sell stakes early to set a price, they are exercising a kind of stewardship over valuation discipline that GPs have been slow to deliver. How far an allocator can lean on that lever still differs by regime: the UK's FRC Stewardship Code treats active ownership as part of fiduciary duty, while 2026 US DOL (EBSA) guidance narrows ESG-driven latitude for ERISA plans. Forcing a real mark on an illiquid book is prudent risk management — provided it is process, not signalling.

• GIC is marketing an LP-led secondary portfolio of up to ~$3bn (buyout-heavy, North-America-weighted), continuing to use secondaries for active rebalancing. (DealStreetAsia)

• Japanese lawmakers floated a sovereign wealth fund drawing on ~¥500tn ($3.2tn) of public financial assets; government officials cautioned against repurposing intervention reserves. (Nikkei Asia)

The anchor moves: Japan's 30-year yield has climbed sharply over the past year.

Sources: Japan MoF / Trading Economics (Jun 24, 2026); Bank of Japan (Jun 16). UAO Research.

"Cheap money was never free — it was borrowed from Japan. As that last cheap-funding anchor reprices, the discount rate on every long-dated asset rises at once, and the patient capital that used to wait for an exit is now setting the price itself. Know which of your returns were really just leverage on someone else's zero rate."

The 30-year JGB and any yen-carry stress · whether more sovereign owners follow GIC into secondaries and where stakes clear vs. last marks · today's US PCE and final Q1 GDP · the PBOC's June 29–30 overnight repos and onshore money-market rates · the Ankara summit run-up and any new defence-spending roadmaps · AI-capex guidance and private-credit spreads on data-center paper.

Japan's rate shift and the global liquidity turn

For three decades, the single cheapest input in global finance was the Japanese yen. With the Bank of Japan holding rates at or below zero, investors borrowed yen for almost nothing, sold them, and bought higher-yielding assets everywhere else. That carry trade was not a niche strategy — it was a structural subsidy to global leverage. On June 24, 2026, the 30-year JGB closed near 3.9% (3.88% on June 24), an effective high not seen since the mid-1990s, eight days after the BoJ took its policy rate to 1.0% (from 0.75%). The level matters less than the regime: one of the world's largest creditors can now earn a real yield at home.

Three channels run from a higher JGB to a universal owner's book. Funding cost: a dearer yen withdraws leverage at the margin. Repatriation: Japanese institutions that reached abroad for yield have less reason to, so the marginal buyer of long-dated Treasuries and global credit steps back. Term premium: as the last anchor of cheap duration lifts, the global term premium — the discount rate on every long-dated cash flow — resets higher. Japan is no longer the world's single largest net creditor, but it remains one of the largest — and the marginal yen it supplied set the global price of risk. Layer on the politics: lawmakers are floating a sovereign wealth fund drawing on roughly ¥500tn ($3.2tn) of public assets. Whether or not it is built, the signal matches the bond market's: Japan is done subsidising the world's risk appetite for free.

If higher discount rates are the macro, the sovereign secondary wave is the micro. With exits sluggish, the most patient owners are not waiting: Global SWF reports GIC, ADIC and CIC among funds selling private stakes into the secondary market, with GIC alone marketing up to ~$3bn. When a sovereign owner sells a real portfolio at a real price, it creates a public reference that can diverge — uncomfortably — from a model mark. The re-pricing of private markets may arrive not through a regulator or a GP, but through the trades of the world's largest allocators.

Cutting the other way is the AI build-out. Micron's record June-24 quarter is the hardest demand proof yet — with supply tight beyond 2027 and multi-year take-or-pay agreements locking in demand. But the same build-out is a cost-push: memory prices up roughly six-fold in a year, US electricity up about 6%, and Morgan Stanley warning that "chipflation" is spreading. One exposure, three hats — equity, credit, inflation — and that inflation is exactly what keeps a term premium from falling.

The take: cheap money was never free — it was borrowed from Japan. As that last cheap-funding anchor reprices, the discount rate on every long-dated asset rises at once, and the patient capital that used to wait for an exit is now setting the price itself. The work this week is to know which of your returns were yield, and which were just cheap funding — before the market tells you.

Universal Asset Owners · info@universalassetowners.com

You are receiving this preview because you are the editor. Subscribers see an unsubscribe link here.