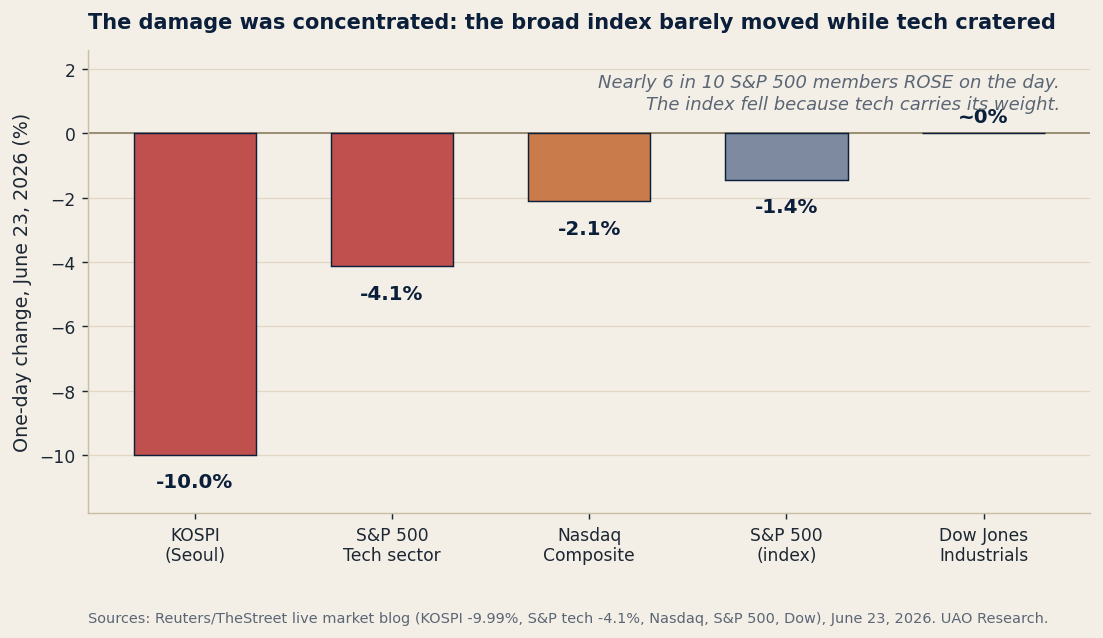

On June 23 the market did something that should unsettle anyone who owns all of it. A regulator's warning in Seoul about over-heated, leveraged chip ETFs sent South Korea's KOSPI down 9.99% — its steepest fall in over three months — and tripped the exchange's circuit breaker. By the New York close the tremor had crossed three time zones: the S&P 500 fell about 1.4% even though nearly six in ten of its members rose, because its technology sector dropped 4.1% and that is now where the index's weight lives. The lesson isn't that chips fell. It's that the thing sold to you as diversification has quietly become a leveraged bet on a dozen names and one macro regime — and both legs moved against you at once.

1. A concentration shock, not a sector story.

The KOSPI's near-10% drop began as a domestic warning about leveraged ETFs, but it exposed a global structure: SK Hynix and Samsung each fell more than 12% and dragged the whole index down with them. The same physics ran in New York — the S&P 500 lost about 1.4% while roughly 299 of 500 members closed higher, because the technology sector alone fell 4.1%. Europe rhymed: the STOXX 600 tech sub-index fell about 3% and ASML fell roughly 6–7%, shedding around $20bn of value. When the top of the index is the index, "owning the market" stops being a hedge and starts being a wager.

Source: Reuters / TheStreet live market blog; CNBC / MarketScreener (Europe, ASML), June 23, 2026.

2. Equities and duration sold off together.

This was not a flight to safety. As tech fell, the two-year Treasury yield hit its highest since February 2025 and the ten-year held near 4.50%, after a Bank of America note argued for up to three hikes in 2026 and no cuts until 2028 — a hawkish reading of Kevin Warsh's June 17 hold, where the Fed kept rates at 3.50–3.75% but lifted its year-end median dot to 3.8% and stripped out its easing language. A universal owner can't diversify equity risk into bonds when both reprice on the same news.

Source: TheStreet live blog (2Y/10Y, BofA note), June 23, 2026; Federal Reserve FOMC statement & SEP, June 17, 2026.

3. The trigger was a story about AI returns, not demand.

What turned a Korean ETF warning into a global rout was sentiment about whether the AI build-out pays off. Oracle disclosed in its annual filing that it had cut about 21,000 jobs — roughly 13% of staff — as it re-tools around AI, booking $1.8bn of restructuring; Broadcom's results earlier in June had already come in without the guidance upgrade the market wanted; and newly public SpaceX fell sharply across three sessions. Not a demand collapse — a re-pricing of the return on a half-trillion dollars of annual, increasingly debt-financed capex. For owners whose fixed-income books hold the paper funding that build-out, the equity wobble and the credit question are the same exposure.

Source: CNBC (Oracle 21,000 cuts & $1.8bn), June 23, 2026 + Oracle FY2026 filing; Broadcom Q2 results, early June 2026.

Built today and live now: an interactive map of how a single leveraged-ETF warning becomes a correlated equity-and-duration drawdown the universal owner can't diversify away — with a multi-agent room you can question. Click any player — a pension CIO, a private-credit lender, a chief risk officer — and ask the desk what they do next.

Open the live scenario →A concentration shock is also a governance question. When a handful of megacaps drive the index, an owner's stewardship leverage concentrates with it. The trans-Atlantic fault line still frames it: the UK's FRC Stewardship Code treats active ownership as part of fiduciary duty, while 2026 US DOL (EBSA) guidance narrows ESG-driven latitude for ERISA plans. A drawdown led by the very companies an owner most needs to steward sharpens the question of whether concentrated engagement is prudent risk management — or an over-reliance to be diversified.

• NBIM (21.8%), GIC and APG agreed to invest up to ~€9.5bn for a 46% stake in TenneT's German grid from Dutch parent TenneT Holding — announced Sep 2025, completing 2026, with KfW in discussions for a separate ~25.1% stake for the German state. (Global SWF)

• Gulf sovereign funds kept deploying through the recent conflict — cumulatively Mubadala >$5.6bn into developed markets and QIA ~$3.39bn since the war began. (The National, Jun 1)

The damage was concentrated: the broad index barely moved while tech cratered.

Sources: Reuters / TheStreet live market blog, June 23, 2026. UAO Research.

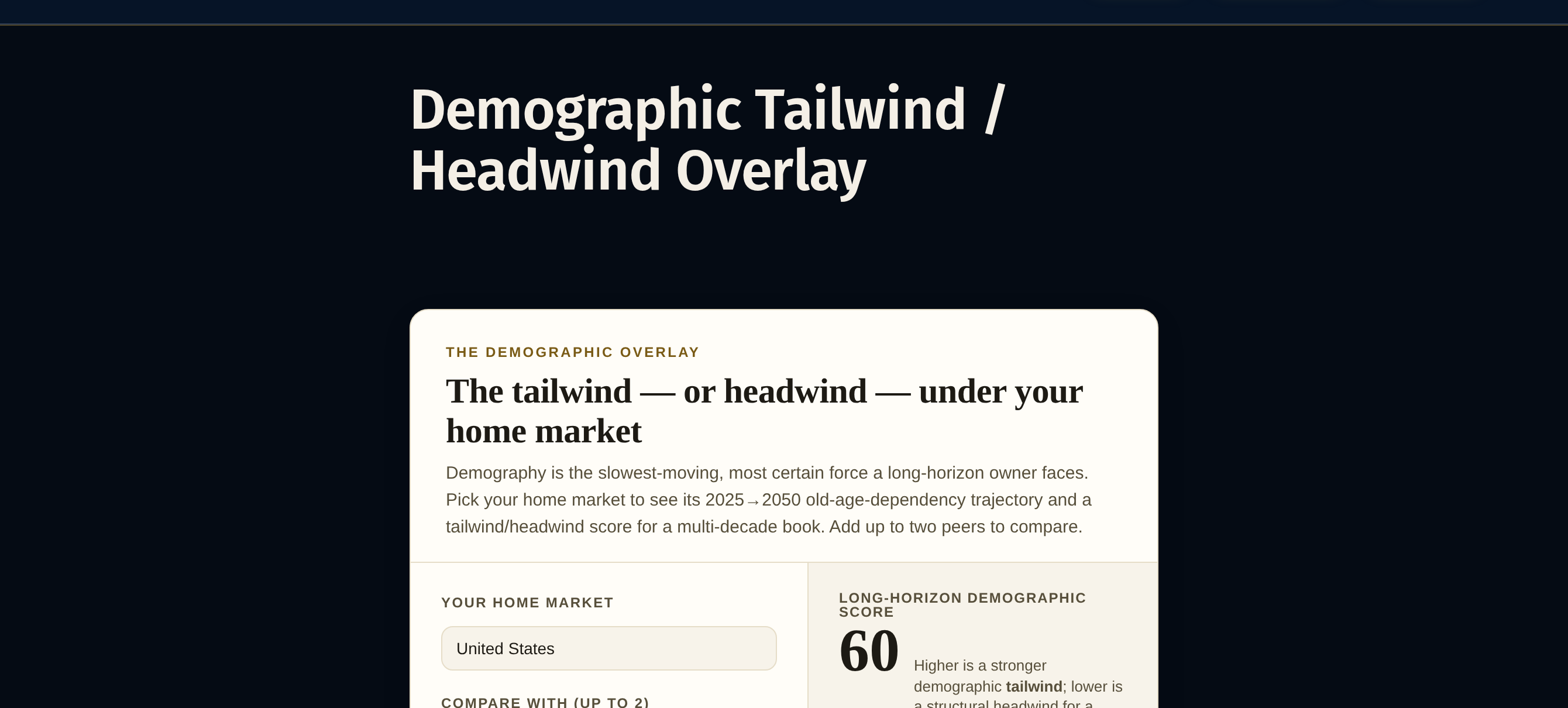

Demography is the slowest-moving, most certain force a long-horizon owner faces. Pick your home market to see its 2025–2050 old-age-dependency trajectory and a single tailwind/headwind score — and compare up to two peers.

Open the tool →"A diversified portfolio that rises and falls on a dozen tickers is not diversified — it is a concentrated bet wearing an index's clothes. Know, before the next leg, exactly how much of the 'whole market' is really one trade — and whether the bonds meant to cushion it will move the same way."

Whether the leveraged-ETF unwind in Korea stays contained or forces further deleveraging across Asian tech · Micron's earnings and the read-through to memory pricing and AI-capex guidance · whether the two-year yield keeps climbing · the 30-year JGB and any yen-carry stress · spreads on the private-credit funding AI data centers.

TheStreet — Markets June 23: BofA rate-hike note, Asian tumble, semis sinking

CNBC — Tech rout intensifies as sell-off grips global stocks

The concentration problem the index won't tell you about

The breadth paradox in one session. June 23 produced a statistic worth teaching in every investment-committee onboarding: the S&P 500 fell about 1.4% on a day when roughly 299 of its 500 constituents rose. The arithmetic is only possible because index weight has migrated to the top — technology fell 4.1% and overwhelmed gains across nearly every other part of the market. The same mechanism ran in Seoul, where two names took the KOSPI down 9.99%, and in Amsterdam, where ASML's 6–7% slide pulled the European tech complex down about 3%. A universal owner who holds the global index holds this concentration by construction; there is no opt-out short of an active underweight — itself an active bet.

Why a hawkish Fed makes concentration more dangerous. The classic answer to equity concentration is duration: hold bonds, and when stocks fall, yields fall and bonds rise. June 23 broke that reflex. The two-year hit its highest since February 2025 on a rate-path story, not a growth-fear story — so equities and bonds fell together. The diversifying asset diversifies only when rates fall for the right reason; strip that away and a 60/40 owner discovers both sleeves are short the same variable.

The trigger: AI returns, not demand. It matters that the catalyst was a return story — Oracle's 21,000 job cuts and \$1.8bn of restructuring, Broadcom's missing guidance upgrade, SpaceX's slide. Demand for compute did not collapse; what re-priced was the expected return on a capex program that exceeds half a trillion dollars a year and is increasingly debt-financed, ending up in the fixed-income books of pensions and insurers. The equity drawdown and the credit-quality question are one exposure seen from two sides.

What a universal owner does about it. Measure single-name and single-factor concentration, not sector labels; re-run the book with equity/bond correlation positive, because June 23 is what that world looks like; and separate the diversifiable (a single name's miss) from the non-diversifiable (the index-weight regime and the rate regime) — the system the universal owner is paid to survive. The discipline is set before the next leg, not after it.

Universal Asset Owners · info@universalassetowners.com

You are receiving this preview because you are the editor. Subscribers see an unsubscribe link here.