Volume 1, Issue 40. Saturday, June 20, 2026. Sent 7:00 am ET / 15:00 GST.

The Strait of Hormuz has been declared open, and the tankers have not yet agreed. Brent crude held near $80 a barrel on Friday — well below the levels of the four-month crisis — even as verified transit data showed fewer than ten commercial vessels moving through the chokepoint, against more than a hundred before the conflict. For a universal owner, the spread between what the oil price now assumes and what the shipping data actually shows is the most important number in the market this week. Below: why the reopening is real on paper but slow in the water, what an $80 Brent does to the Gulf's fiscal arithmetic and therefore to its sovereign funds, and why — through all of it — the world's largest allocators kept signing cheques for hard infrastructure.

1. The Strait reopened on paper — the tankers haven't followed.

Oil markets spent Friday digesting a contradiction. The risk premium that drove Brent toward multi-year highs during the spring closure has largely unwound — crude steadied near $80 a barrel — on the back of a US–Iran framework reported signed midweek that calls for the full reopening of the Strait of Hormuz without Iranian tolls for at least 60 days. But the physical recovery is lagging the diplomatic one badly. Nearly ten million barrels of crude were observed transiting or staged near the Strait on Thursday, including the first Saudi-owned tankers to move since the conflict began more than three months ago — and then, on Friday morning, no outbound vessels were seen leaving the Persian Gulf at all. Commercial transits remain at an estimated 5–10% of pre-crisis levels, held down by mine-clearance requirements, war-risk insurance surcharges, and demands for verified safety assurances.

For a long-horizon allocator the read-across is not the oil price itself but the divergence. The market has priced a clean reopening; the shipping data has priced a fragile one. Kpler estimates volumes could recover to roughly 40 transits a day — near half the prewar norm — within 30 days if no setbacks emerge, but the qualifier is doing the work: planned US–Iran follow-on talks in Switzerland were canceled, and fighting erupted in Lebanon on Friday. The base case is normalization; the tail that an owner of the whole market cannot diversify away from is a re-closure that the oil curve is no longer paying you to hedge.

Source: Oil prices rise as Lebanon fighting erupts and Hormuz traffic still slow, Al Jazeera, June 19, 2026. | CNBC — Strait of Hormuz reopening may take weeks to ease backlog, June 18, 2026. | Coverage: Gulf Capital Briefing, today.

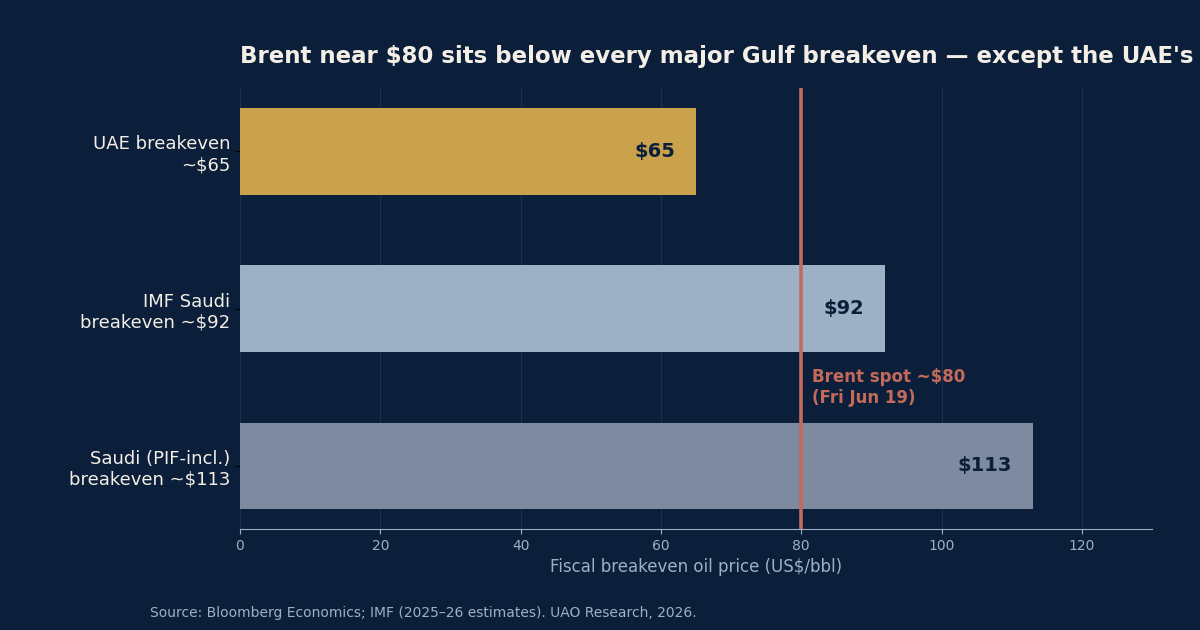

2. At $80 Brent, the Gulf's fiscal arithmetic turns against the funds.

An $80 Brent is comfortable for an oil consumer and uncomfortable for most of the producers that own the Gulf's sovereign wealth. Saudi Arabia's fiscal breakeven — the oil price at which the budget balances — was estimated by Bloomberg Economics at roughly $113 a barrel for 2025 once the Public Investment Fund's domestic Vision 2030 commitments are included, against an IMF breakeven nearer $92 (both 2025 estimates). The kingdom forecast a 2026 deficit of about 165 billion riyals ($44bn), or 3.3% of GDP, in its December 2025 budget; Goldman Sachs has modelled something closer to 6.6%. The UAE, with a breakeven near $65 a barrel, sits on the other side of the line.

The mechanism matters more than the headline. When oil prints below breakeven, a Gulf sovereign fund becomes, at the margin, a source of domestic fiscal support rather than a pure global allocator — capital that might have been deployed into international equities, private markets or infrastructure is instead reserved to backfill the state, or the state borrows to avoid drawing it down. Saudi Arabia has leaned on debt issuance precisely to keep PIF deploying. For the asset managers, banks and data providers that sell to Gulf capital, an extended sub-breakeven Brent is the variable that quietly governs the size of next year's mandates.

Source: Saudi Arabia's policy trilemma: Oil, debt and deficits in 2026, AGBI, December 2025.

3. Even amid the shock, the universal owners keep buying the hard assets.

Step back from the oil tape and the deployment machine of the world's largest funds kept running. GIC and Temasek of Singapore, CalPERS, and Korea's National Pension Service are the institutional capital behind Macquarie Asset Management's A$11.7bn ($8.2bn) take-private of Qube Holdings, Australia's largest integrated logistics and port operator. Qube shareholders approved the scheme of arrangement on June 16, at A$5.20 cash per share; the deal cleared its competition review around the June 19 statutory deadline, with the second court hearing set for early July (dates as background).

The signal for universal owners is the through-the-cycle posture. Four very different institutions — two Asian sovereigns, a US public pension, a Korean national fund — converged on the same trade: a regulated, inflation-linked, physically essential asset bought at scale and held for decades. That is the universal owner's natural habitat. It is also a reminder that while the oil headline is the noise, the structural allocation into real assets and infrastructure is the signal, and it does not pause for a geopolitical crisis. Today's deep-dive takes the same instinct into its most crowded expression — the financing of the AI build-out.

— Chart of the day —

Brent near $80 sits below every major Gulf budget breakeven — except the UAE's.

Source: Bloomberg Economics; IMF (2025–26 estimates). UAO Research, 2026.

— Take of the day —

"The oil curve has stopped paying universal owners to worry about Hormuz, but the shipping data says the risk hasn't left — it has just gone unpriced. When the market and the physical world disagree this openly, the long-horizon owner's edge is to trust the tankers over the tape, and to treat a sub-breakeven Brent as a constraint on Gulf deployment, not a discount."

— UAO Research.

— Three links worth your time —

- International Monetary Fund — Global Financial Stability Report, Ch. 2: The Rise and Risks of Private Credit. The primary text behind today's deep-dive: where the leverage hides, and why insurers and pensions are the channel.

- Financial Stability Board — Report on Vulnerabilities in Private Credit, 6 May 2026. The regulators' own map of stale valuations, layered leverage and unclear interconnections in the asset class now financing the data-centre boom.

- Infrastructure Investor — Temasek, GIC and CalPERS in the Macquarie–Qube consortium. A clean look at how four very different universal owners converge on the same real-asset trade.

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Universal Owner · view the chart of the day.

Produced and edited by the UAO editorial desk. Not investment advice.