Volume 1, Issue 34. Sunday, June 14, 2026. The Long Horizon edition.

A universal owner does not get to treat artificial intelligence as a sector. It owns the demand through its index weight in the hyperscalers, it is being courted to fund the supply through grid and generation assets, and it carries the consequences — power prices, reliability, a slower energy transition — if the two fail to meet. This Long Horizon edition looks at the AI build-out from that seat: why electricity, not silicon, is now the binding constraint; why allocators are quietly repricing the trade from chips to power; why the grid itself has become the scarce asset; and how sovereign and pension capital is already moving to the supply side. The week ahead gives it a near-term frame — CalPERS takes its Investment Committee on Monday, and the fight over how America runs its largest power grid is now in the open.

1. The binding constraint on AI is electricity, and the universal owner is on every side of it.

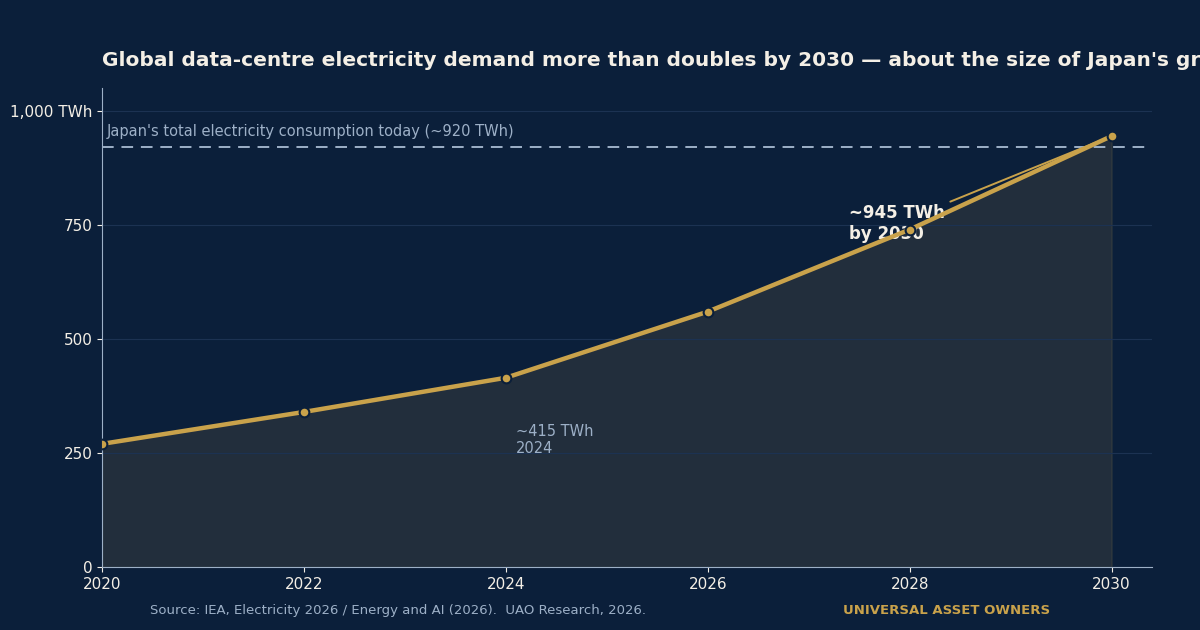

Start with the arithmetic that reframes the whole trade. Global data-centre electricity demand is on track to more than double to roughly 945 terawatt-hours by 2030 — slightly more than Japan consumes today — with AI the single largest driver, according to the International Energy Agency's 2026 work. In the United States, data centres account for close to half of all electricity-demand growth between now and 2030. The constraint on the next leg of AI, in other words, is no longer how many chips can be fabricated; it is whether enough power can be generated, moved and connected to run them.

For a stock-picker this is a margin question. For an owner of the whole economy it is a structural one. The same balance sheet holds the AI demand (the hyperscalers are an unavoidable index exposure), is the natural financier of the AI supply (grid, generation and transmission are exactly the long-duration, inflation-linked assets a pension or sovereign fund wants), and absorbs the second-order costs if supply lags — higher power prices for the whole portfolio's industrial holdings, and a decarbonisation path that slips if the gap is filled with gas. You cannot index your way around a force that touches every line of the book at once.

Source: IEA, Energy and AI / Electricity 2026, 2026. | Coverage: The Long Horizon, this week.

2. Allocators are repricing the AI trade from chips to power.

The institutional money has already begun to move down the stack. In BlackRock's Spring 2026 Investment Directions, published April 24 and drawing on a survey of 732 of the firm's EMEA clients, only about one in five still considered large US technology firms the most compelling way to express the AI theme. More than half named energy and power providers as the best opportunity; 37% pointed to infrastructure companies. "Interest is broadening from core AI technology to the wider ecosystems underpinning it," the firm wrote — its phrasing for a rotation from the demand side of AI to its supply side.

That is a comfortable move for a long-horizon owner, because the supply side is where its natural advantages lie: patient capital, tolerance for illiquidity, and a horizon long enough to underwrite a power asset that takes years to connect. The risk is crowding — if every allocator reaches the same conclusion at once, the "diversification" of owning power instead of chips erodes as the assets reprice. Watch whether the capital flows to genuinely scarce assets (interconnection rights, firm generation) or simply bids up the same listed utilities.

Source: BlackRock, 2026 Spring Investment Directions, April 24, 2026.

3. The grid, not the chip, is the scarce asset.

Here is where the constraint bites hardest. The IEA estimates that meeting electricity demand through 2030 requires annual grid investment to rise by roughly half from today's about $400 billion, and warns that without faster transmission build-out up to 20% of planned data-centre projects risk delay. The queue is the symptom: the average wait for a large new grid connection now runs seven to ten years across established North American and European hubs. The largest US grid operator, PJM Interconnection — which serves more than 65 million people across 13 states — has projected, on the basis of its December 2025 capacity auction, a reliability shortfall of roughly six gigawatts by 2027; in early-June 2026 reporting that strain had hardened into open calls to restructure or break up the operator.

For the universal owner the read-across is precise: when grid access is the binding constraint, the interconnection right and the firm megawatt become the assets worth owning, and "shovel-ready with a signed connection agreement" is worth more than another speculative campus. It also turns a portfolio question into a policy one — permitting, transmission siting and grid governance now move the value of assets the owner already holds.

Source: IEA, Electricity 2026 — Grids, 2026.

4. Sovereign and pension capital is already building the supply side.

This is not theoretical. The pattern of the largest long-horizon funds is to own the physical layer of AI rather than rent its equity beta. CPP Investments and the Australian developer Goodman Group established a roughly $9.3 billion European data-centre partnership, announced in January 2026, and GIC has explored Goodman's data-centre platform; GIC, CPP and Equinix earlier built a $15 billion US data-centre venture. These are dated moves, not this weekend's news — but together they describe a standing strategy: use the balance sheet's duration to fund the power-and-compute stack directly, capturing the build margin rather than paying the listed multiple.

The open question for an investment committee is sequencing. Funding the supply side is sound — until the demand assumptions that justify a campus prove too aggressive, and the long-dated asset is left waiting on a tenant. The discipline is to underwrite the power, not the hype.

Source: CPP Investments / Goodman, European data-centre partnership, January 20, 2026.

— Chart of the day —

Global data-centre electricity demand is on track to more than double by 2030 — roughly the size of Japan's grid.

Source: IEA, Electricity 2026 / Energy and AI (2026). UAO Research, 2026.

— Take of the day —

"The cleanest way to understand AI from an allocator's seat is to stop treating it as a technology bet and start treating it as an electricity bet with a software option attached. The universal owner's edge is not picking the winning model — it is owning the grid, the generation and the interconnection rights that every model will need, on a horizon no venture fund can match. The risk is that everyone now sees this at once."

— UAO Research.

— Three links worth your time —

- IEA — Energy and AI. The single best primary source on how much power AI actually needs, and where the grid breaks first.

- BlackRock — 2026 Spring Investment Directions. The clearest read on how institutions are repricing AI from chips to power.

- Bloomberg — AI Data Center Boom Risks Breakup of Biggest US Power Grid Operator. Why grid governance is now a portfolio variable.

*The Universal Owner publishes UniversalAssetOwners.com. Reply to this email or wri

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Universal Owner · view the chart of the day.

Produced and edited by the UAO editorial desk. Not investment advice.