Tuesday, June 9, 2026 — the daily brief for the world's long-duration owners of capital.

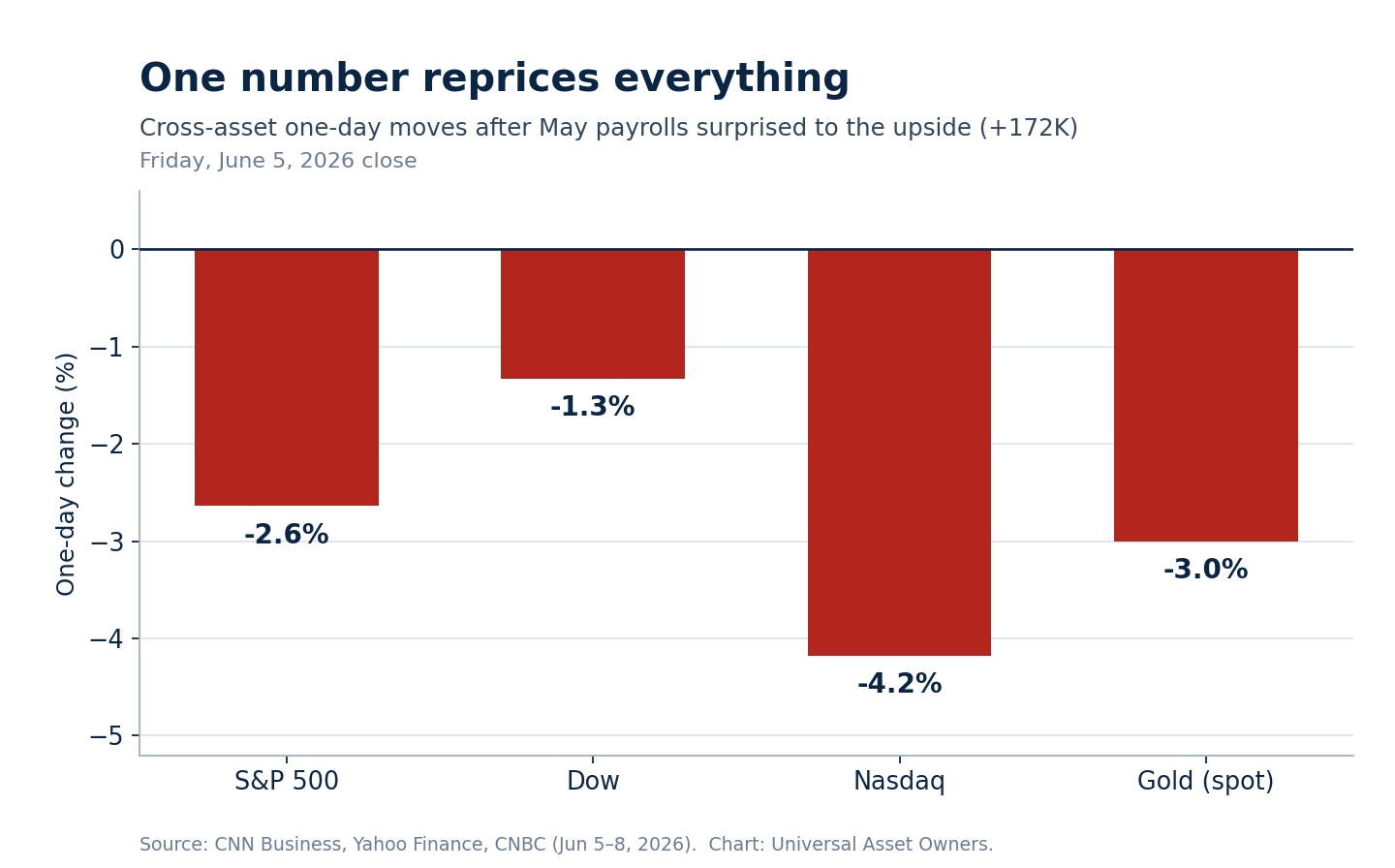

One labour-market number has done what a year of Fed commentary could not: it has taken rate cuts off the table and put a rate hike back on it. May payrolls landed Friday at +172,000 — more than double the roughly 80,000 economists expected — with unemployment holding at 4.3% and the prior two months revised up a combined +93,000. For a universal owner, the interesting part is not the print itself but how cleanly it travelled: in a single session it repriced equities, the curve, gold and the dollar at once. When one variable moves everything, diversification is doing less work than the policy portfolio assumes.

The regime flip

Futures now price better than a 70% chance of a Fed hike by December, up from roughly 45% a week earlier, and forecasters including Goldman Sachs have shifted to no cuts in 2026. The June 16–17 FOMC meeting is still almost universally expected to hold the funds rate at 3.50–3.75%; the live question is whether the Committee drops its easing bias altogether. The signal for long-horizon allocators is that the "higher-for-longer" rate path many capital-market assumptions had begun to discount away is reasserting itself — with direct consequences for discount rates, the cost of leverage in private books, and the marginal value of the bond hedge.

What it did to markets

Friday delivered the worst equity session since October. The S&P 500 fell 2.6% to 7,383.74, the Nasdaq dropped 4.2% as a soft AI-chip outlook from Broadcom hit the semiconductor complex, and the Dow shed 1.3%. The selloff paired a yield jump with stretched AI valuations — a reminder that the concentration powering index returns cuts both ways. Markets steadied into Monday and Tuesday on a chip-led rebound, but the episode is a clean illustration of how much of the market's recent direction has rested on a single, crowded theme.

The hedge that didn't hedge

The move worth dwelling on is gold. Rather than catch a safe-haven bid, bullion fell roughly 3% on Friday and slipped to about $4,314 an ounce — a more-than-two-month low that erased its entire 2026 gain — as the repricing of real rates overwhelmed the geopolitical story. For owners who treat gold and long bonds as ballast, the lesson is the uncomfortable one the Oracle Brief below keeps returning to: in a rate-driven shock, the diversifiers correlate. Correlation-regime risk belongs in the base case, not the tail.

Oil and the security premium

The exception to the risk-off tape was crude. Brent pushed more than 3% higher, back above $96 a barrel on Monday, after Israeli strikes on Lebanon and reports of explosions in Iranian cities revived fears of a wider conflict — and with it, the standing question of the Strait of Hormuz. Traders are once again weighting geopolitical supply risk over OPEC+ barrels. This is the security-premium repricing of trade and energy that sits at the top of the desk's risk board, and it is increasingly a structural input to inflation rather than a passing headline.

What the largest owners are doing

Beneath the tape, the biggest pools of long-term capital are leaning into real assets and AI infrastructure. Norges Bank Investment Management recently agreed to take a one-third stake in a portfolio of North American operating renewables alongside Brookfield and British Columbia Investment Management; CPP Investments has backed a data-centre expansion in Ontario; and the Gulf funds — PIF, with its stated ambition to deploy on the order of $70bn a year through 2030, alongside Temasek and the Kuwait Investment Authority — continue to anchor the consortia financing data centres and compute. The through-line is capital rotating toward assets with contracted cash flows and a structural demand story, precisely as the discount-rate environment turns less forgiving.

What to watch

The week's hinge is Wednesday's May CPI at 8:30 a.m. ET. After Friday's payrolls, a hot inflation print would harden the hike narrative and pressure duration further; a soft one buys the doves time. The June 16–17 FOMC follows. For now, the desk's read is simple: the market has spent a year pricing the end of the tightening cycle, and a single jobs report has reminded everyone that the cycle gets a vote too.

The numbers above reflect Friday's close and Monday's session; intraday levels move. Editorial analysis for long-duration capital — not investment advice.