Volume 1, Issue 29. Monday, June 8, 2026. Sent 7:00 am ET / 14:00 GST.

A labor market can look healthy on the surface and have quietly stopped hiring underneath, and that gap is now the most important thing on an allocator's screen. Friday's US jobs report beat every forecast, yet almost three-quarters of the gain came from two sectors and the long-term unemployed hit a cycle high. Into that ambiguity walks a week of central-bank meetings on opposite sides of the Atlantic, oil back above $96 on a Strait of Hormuz that will not fully reopen, and a 10-year Treasury drifting toward 4.55%. Below: the print, the policy split, the supply shock, and the duration tell — plus the chart of the day and three links worth your time.

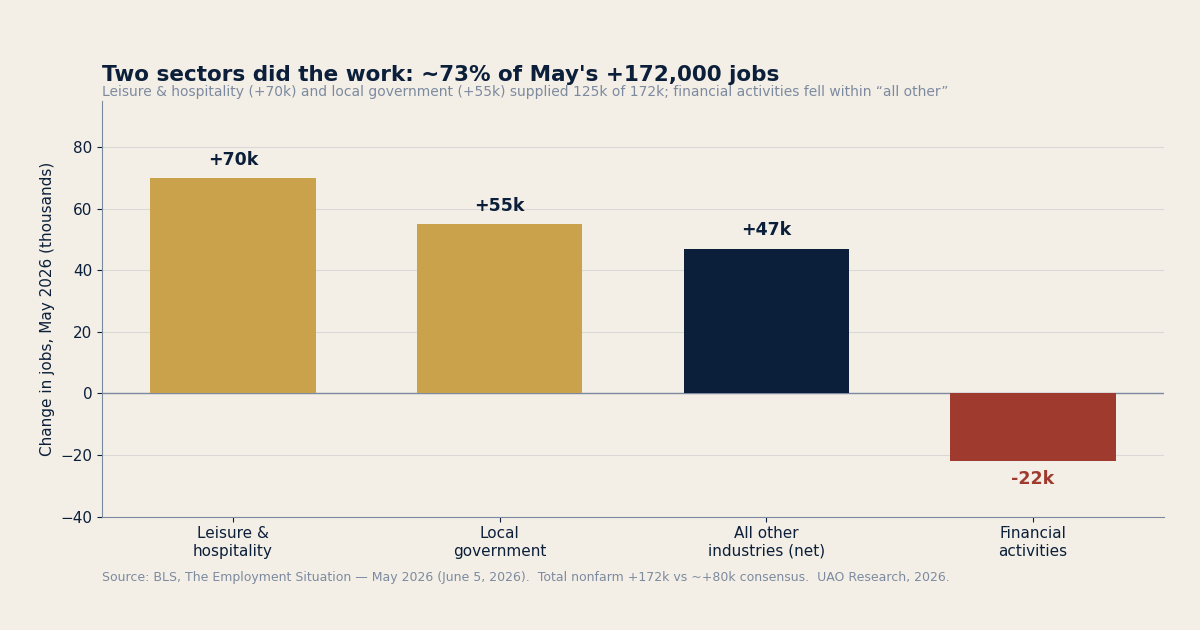

1. The May jobs beat was real — and narrower than it looked.

US nonfarm payrolls rose 172,000 in May, reported the Bureau of Labor Statistics on June 5, more than double the roughly 80,000 economists expected, with March and April revised up by a combined 93,000 and the unemployment rate unchanged at 4.3%. On the headline, a labor market refusing to break.

Look one layer down and the picture is a market that is freezing rather than cooling gently. Leisure and hospitality (+70,000) and local government (+55,000) supplied 125,000 of the 172,000 — roughly 73% of the gain — while financial activities shed 22,000. The more telling number is a stock, not a flow: the long-term unemployed rose 524,000 over the year and now make up 27.5% of all unemployed people, the highest share of this cycle. When few are being laid off but the unemployed cannot find work, you have an economy that has stopped hiring without yet contracting.

For a universal owner the read-across is to the duration book and the soft-landing premium embedded across the whole portfolio. A late-cycle market that is strong on top and brittle underneath narrows the path between the inflation that keeps policy tight and the slack that finally cracks it.

Source: BLS, The Employment Situation — May 2026, June 5, 2026. | Coverage: Macro / overnight, this week.

2. The Atlantic splits this week — and that is a currency and duration event.

The same data lands into a divergence in policy direction. Futures have the Federal Reserve holding at its June 17 meeting, with markets not pricing a cut until December at the earliest. Across the Atlantic, markets price a near-certain (~99%) chance the European Central Bank hikes 25 basis points on June 11, taking its deposit rate to 2.25%, as euro-area inflation climbed to 3.2% in May on the energy shock — a central bank tightening into an inflation its own rates cannot supply-fix.

A universal owner does not get to treat this as a domestic-rates story. Divergence in policy direction is, mechanically, a repricing of the currency and the cross-border duration book — the euro hedges, the dollar-funding cost, the relative value of European versus US long bonds that sit in the matching portfolio. When two of the world's largest central banks pull in opposite directions, the FX and rates carry inside a global book moves whether or not the allocator touched a single position.

Source: Marketplace / CNBC, June 2026.

3. The supply shock under everything: oil back above $96 on a Hormuz that won't reopen.

Brent crude climbed above $96 a barrel Monday (WTI above $93) after fresh Iran–Israel missile exchanges, with the near-closure of the Strait of Hormuz continuing to choke Persian Gulf supply. OPEC+ has leaned against the strain only modestly, approving an additional 188,000 barrels per day for July. S&P Global Ratings has raised its Brent and WTI price assumptions, citing the ongoing effective closure of the strait.

This is the input that makes the other two items legible. The euro-area inflation forcing the ECB's hand is, at its core, an energy bill; the "higher for longer" pressure on the US long end is partly an oil-price tail. A supply-driven price shock is the one inflation a central bank cannot ease away without crushing output — and it is precisely the exposure a globally diversified owner cannot diversify, because it is short energy through its beneficiaries and its growth assumptions at the same time.

Source: Vantage Markets / TradingEconomics oil wrap, June 8, 2026.

4. The duration tell: the 10-year is repricing on the inflation it is meant to insure.

The clearest single-instrument summary sits in the long end. The benchmark 10-year US Treasury yield rose to roughly 4.55% by Friday's close, up from 4.44% a week earlier, on solid data, oil volatility and hawkish Fed commentary. The move is small in basis points and large in meaning: the asset long-horizon owners hold to hedge equities is itself selling off on the inflation it is supposed to insure against.

That is the quiet problem in items one through three combined. If the next shock is a supply shock, bonds are less likely to rally when equities fall — a point the IMF made directly this year, and the subject of today's deep-dive.

Source: T. Rowe Price, Global Markets Weekly Update, June 5, 2026.

— Chart of the day —

Two sectors did the work: leisure & hospitality and local government were about 73% of May's 172,000 jobs.

Source: BLS, The Employment Situation — May 2026 (June 5, 2026). UAO Research, 2026.

— Take of the day —

"The market is trading the jobs beat as resilience and the bond market as caution; both are right, which is the problem. A labor market that has stopped hiring without yet firing, an inflation shock central banks can't ease away, and a long bond selling off on that same inflation describe an economy where the soft-landing premium and the duration hedge are quietly being charged against the same account. For a universal owner the instruction isn't a trade — it's to stop assuming the bond leg will catch the fall."

— UAO Research.

— Three links worth your time —

- BLS — The Employment Situation, May 2026. The primary print itself — read the household-survey detail and the long-term-unemployment share before you take the headline at face value.

- IMF — Stock-Bond Diversification Offers Less Protection From Market Selloffs. The research backbone for why the bond hedge is weaker in a supply-shock, inflation-driven regime — the heart of today's deep-dive.

- S&P Global Ratings — Raised WTI and Brent assumptions on the Strait of Hormuz. A ratings agency moving its price deck is the supply shock entering credit and discount-rate assumptions across the book.

The UAO Daily Brief is produced by Universal Asset Owners — intelligence for long-horizon capital. Read the archive at universalassetowners.com. Questions, corrections, or to reach the desk: info@universalassetowners.com. Not investment advice.

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Universal Owner · view the chart of the day.

Produced and edited by the UAO editorial desk. Not investment advice.