Volume 1, Issue 28. Sunday, June 7, 2026. Sent 7:00 am ET / 14:00 GST.

The AI buildout has stopped being a technology story and become an ownership one. A Blackstone- and Canada-Pension-backed operator has committed $30 billion to build five gigawatts of data-centre capacity in India; the largest cloud platforms are guiding to roughly $725 billion of capital spending this year; and on the biggest US grid, wholesale power has posted its sharpest jump on record, with most of the increase pinned to data-centre demand. For a universal owner, those are not three stories. They are one position — financed, powered, and ultimately paid for by the same balance sheet. Below: the deal, the scale, the bill, and the return question — plus the chart of the day and three links worth your time.

1. A pension-backed operator just committed $30 billion to build five gigawatts in India.

On June 5, AirTrunk — the Asia-Pacific hyperscale developer owned by Blackstone and the Canada Pension Plan Investment Board — said it plans to invest more than $30 billion in Indian data-centre capacity by 2030, underpinning five gigawatts of new build. The company framed India as "a cornerstone" of its global strategy; the commitment ranks among the largest digital-infrastructure programs under consideration in the country, and follows AirTrunk's entry into the market six weeks earlier through its acquisition of Lumina CloudInfra.

The detail that matters for this audience sits in the ownership column. The capital behind the gigawatts is a public pension fund. CPP Investments is not lending against the compute backbone from a distance — it is an equity owner of it. When a retirement system for 22 million Canadians is building power-hungry infrastructure to host other people's AI models, the line between "allocator" and "operator of the real economy" has effectively dissolved.

AirTrunk's own framing makes the scale legible: its proposed five gigawatts, combined with commitments from Google, Microsoft, Amazon and Adani, would require India to build more data-centre capacity in four years than it has built in its entire history, several times over.

Source: AirTrunk, June 5, 2026. | Coverage: AI and the Long-Term Portfolio, this week.

2. The capital scale behind that demand is now a macro force, not a sector trade.

The demand AirTrunk is building toward is set by a handful of balance sheets. The largest hyperscalers have guided to a combined roughly $725 billion of capital expenditure in 2026 — up about 77% from around $410 billion in 2025 — led by Amazon at approximately $200 billion, with Alphabet, Microsoft and Meta each guiding above $100 billion and rising. (Treat the totals as company guidance that moves quarter to quarter, not a settled figure.)

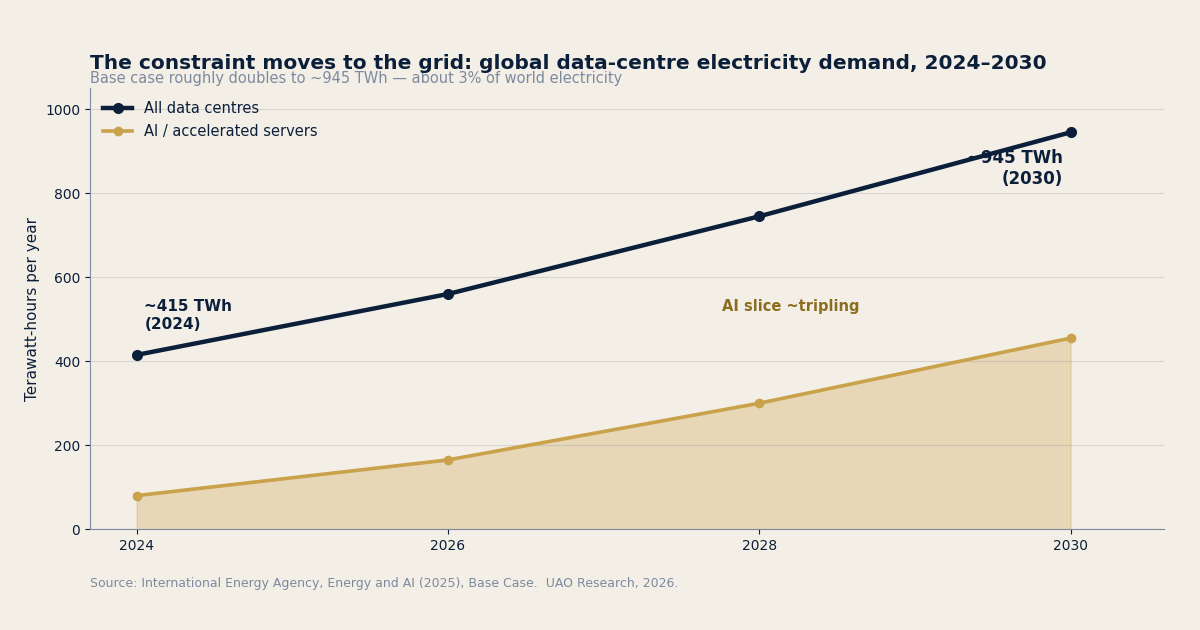

That spending lands as physical load. In its Energy and AI analysis, the International Energy Agency projects global data-centre electricity consumption roughly doubling — from about 415 terawatt-hours in 2024 to around 945 TWh by 2030, just under 3% of world electricity — with consumption from AI-driven "accelerated" servers growing about 30% a year, more than four times faster than electricity demand from everything else. The IEA's framing is the one a long-horizon owner should internalise: the binding constraint on this cycle has moved from chips, to capital, to electrons.

Source: International Energy Agency, Energy and AI, 2025.

3. The cost of the megawatts is already landing on the public.

The clearest signal that the constraint is real is the price of power. On the 13-state PJM grid — the largest in the US — Q1 2026 wholesale power averaged $136.53 per megawatt-hour, up 76% from $77.78 a year earlier, the largest single-year jump in PJM's history. The independent market monitor, Monitoring Analytics, attributed 63% of that increase to data-centre load — roughly $9.3 billion in added costs to be absorbed over the coming year. The capacity auction tells the same story: the 2026–27 round cleared at the FERC-approved price cap of $329.17 per megawatt-day, against $28.92 two years earlier.

For a universal owner this closes a circle most allocators never see. The same institution that finances the data centres and owns the hyperscaler tenants also serves beneficiaries who are the ratepayers and voters now absorbing 15–30% commercial retail increases. The externality of the buildout is not outside the portfolio — it is inside it, two desks over.

Source: Monitoring Analytics via E&E News / Utility Dive, 2026.

4. The open question is whether the build earns its cost of capital.

The buildout is being marketed to long-horizon owners as a clean liability match: contracted, inflation-linked cash flows from creditworthy hyperscaler tenants, secured against physical plant, over multi-decade horizons. That pitch is real. But it rests on the revenue arriving. In its 2025 Global Technology Report, Bain & Company estimated the buildout would need roughly $2 trillion in new annual revenue by 2030 to fund the required compute — and forecast an $800 billion shortfall even on generous assumptions, naming power supply as the gating input. (This is a consultancy forecast, not a settled fact; pair it with each manager's own disclosures.)

The universal owner's discomfort is that it cannot diversify the bet away. It funds the build, owns the tenants, supplies the power, and carries the ratepayer politics — four exposures to one complex, gated by one constraint. The honest posture is not to pick a side but to act on the part it controls: capex discipline at the tenants, grid investment, "bring-your-own-generation" rules, and ratepayer fairness — because all of those protect the whole book.

Source: Bain & Company, September 2025.

— Chart of the day —

The constraint, in one curve: global data-centre electricity demand roughly doubles by 2030, and the AI slice drives it.

Source: International Energy Agency, Energy and AI (2025). UAO Research, 2026.

— Take of the day —

"For a universal owner, the AI-infrastructure trade is sold as a diversifier and is in fact the opposite — a concentrated doubling-down on an exposure you already carry, intermediated through a constraint you don't govern. You fund the build, own the tenants, supply the power, and pay the bill through your beneficiaries. Diversification across those four desks is illusory because they are the same bet on the same complex. The remaining edge isn't the clever allocation; it's that you will still be here, owning the grid and the consequences, in 2050."

— UAO Research.

— Three links worth your time —

- International Energy Agency — Energy and AI (Energy demand from AI). The primary, modelled backbone for the whole debate — read the base-case demand curve and the regional split before your next infrastructure commitment.

- Bloomberg — Blackstone's AirTrunk to Spend $30 Billion on India Data Centers. The week's clearest example of pension capital directly owning the compute backbone, not lending to it.

- Utility Dive — Data centers were a record share of PJM capacity costs: market monitor. The numbers that make the "your beneficiaries are the ratepayers" argument land — straight from the independent market monitor.

The UAO Daily Brief is produced by Universal Asset Owners — intelligence for long-horizon capital. Read the archive and the AI and the Long-Term Portfolio franchise at universalassetowners.com. Questions, corrections, or to reach the desk: info@universalassetowners.com. Not investment advice.

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Universal Owner · view the chart of the day.

Produced and edited by the UAO editorial desk. Not investment advice.