Volume 1, Issue 21. Saturday, May 30, 2026. The Weekend Brief.

US equities ended May at record highs, the long end rallied hard, and within 48 hours the ECB warned the calm is borrowed. The Weekend Brief reads three signals off that split screen — the rally and what it leans on, the official sector's fragility warning, and the densest macro week of the quarter now starting Monday.

1. Wall Street closed May at record highs — but the rally is leaning on a ceasefire bet and an AI trade the official sector is calling stretched.

The S&P 500 closed Friday, May 29 at a record 7,580.06, up 0.22% on the day and 1.43% on the week — its ninth straight weekly gain, the longest run since December 2023 — capping a May of roughly +5.2%. The Nasdaq added 2.39% on the week; the Dow set its own record. The move was led by technology (the tech sector rose about 5.6% on the week, with Dell up roughly a third on results), and propelled at the margin by falling energy prices and US–Iran de-escalation hopes: WTI crude slid below $87 a barrel for the first time since April 21. The bond market rallied alongside it — the 10-year Treasury yield finished at about 4.45%, down roughly 11.8 basis points on the week, its largest weekly fall since February.

For a universal owner the question is not the level but what is holding it up. Two props carry this tape: continued AI-earnings validation, and a bet that the Middle East conflict de-escalates rather than re-escalates. Both can reverse in a single headline. Records built on a ceasefire that has not been signed are records to respect, not to extrapolate.

Source: Yahoo Finance / Zacks, May 29, 2026. · Source: Advisor Perspectives, May 29, 2026.

2. The ECB just told euro-area owners the calm is borrowed.

Two days before that record close, the European Central Bank published its Financial Stability Review on May 27 and drew the opposite picture. The euro-area outlook, it warned, is being shaped by geoeconomic stress and an energy supply shock from the Middle East war; equity valuations remain stretched by historical standards, corporate-bond risk premia are compressed globally, and pockets of leverage in non-banks — notably hedge funds — could amplify any adjustment. Banks, it judged, sit on enough capital and liquidity to absorb a shock; the markets around them do not have the same cushion.

That is the value of a primary document on a record-high weekend: the institution charged with watching the plumbing is saying the price of calm is high and the exposures are concentrated. The Fed is no more relaxed — minutes from its late-April meeting, released earlier in May, showed a majority of officials would consider a rate hike if the energy-driven inflation persists, a striking stance with the curve rallying. The tape and the supervisors are telling different stories; a long-horizon owner has to hold both.

Source: European Central Bank, May 27, 2026.

3. The densest macro week of the quarter starts Monday.

The next twelve days front-load the data that resets every discount rate. ISM manufacturing lands Monday, June 1; ISM services Wednesday, June 3; the US May employment report Friday, June 5; the OPEC+ ministerial June 7; and the ECB's rate decision June 11. After a holiday-shortened week (US markets were closed for Memorial Day on May 25), allocators move straight into a calendar where rates, the dollar and oil can all reprice in the same five sessions. The universal-owner risk is correlation: in a market the ECB calls concentrated, the diversification in a 60/40 sleeve tends to thin out precisely when the prints cluster.

Source: US BLS release schedule. · Source: ECB Governing Council calendar.

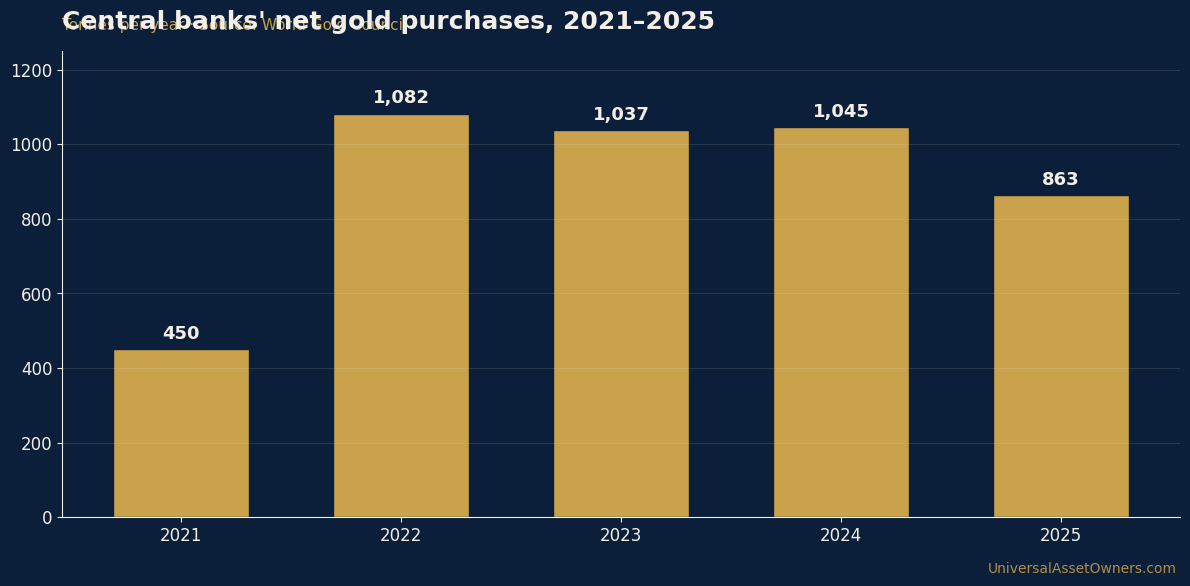

— Chart of the day —

Central banks keep hedging the same duration-and-dollar risk: net gold buying has held near record pace.

Source: World Gold Council (2025 full-year 863t; net 244t in Q1 2026). UAO Research, 2026.

— Take of the day —

*"A record close on a Friday and a financial-stability warning on the Wednesday before it are not a contradiction — they are the trade. Th

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Universal Owner · view the chart of the day.

Produced and edited by the UAO editorial desk. Not investment advice.