Volume 1, Issue 18. Wednesday, May 27, 2026. Sent 7:00 am ET / 14:00 GST.

On July 1 the largest US public pension dissolves the walls between its asset classes and lifts its private-market targets — days after a regulator put its first dedicated warning on the very assets it is buying. Today's brief: CalPERS' move to a total portfolio approach, the Financial Stability Board's private-credit report, the pensions writing bigger private-credit cheques regardless, Britain hard-wiring the same trade into law, and the funded-status cushion that makes the risk-taking possible. One chart on who is lifting their private-credit targets.

1. CalPERS is about to tear down the walls between its asset classes — and lift private markets as it does.

On July 1, the California Public Employees' Retirement System — a $589.54bn fund, the largest public pension in the United States — replaces the strategic asset allocation model it has used for decades with a "total portfolio approach." Instead of fixed buckets for equities, bonds and alternatives, every prospective investment competes for capital against every other, measured by how it improves the whole fund against a single 75/25 equity-bond reference portfolio.

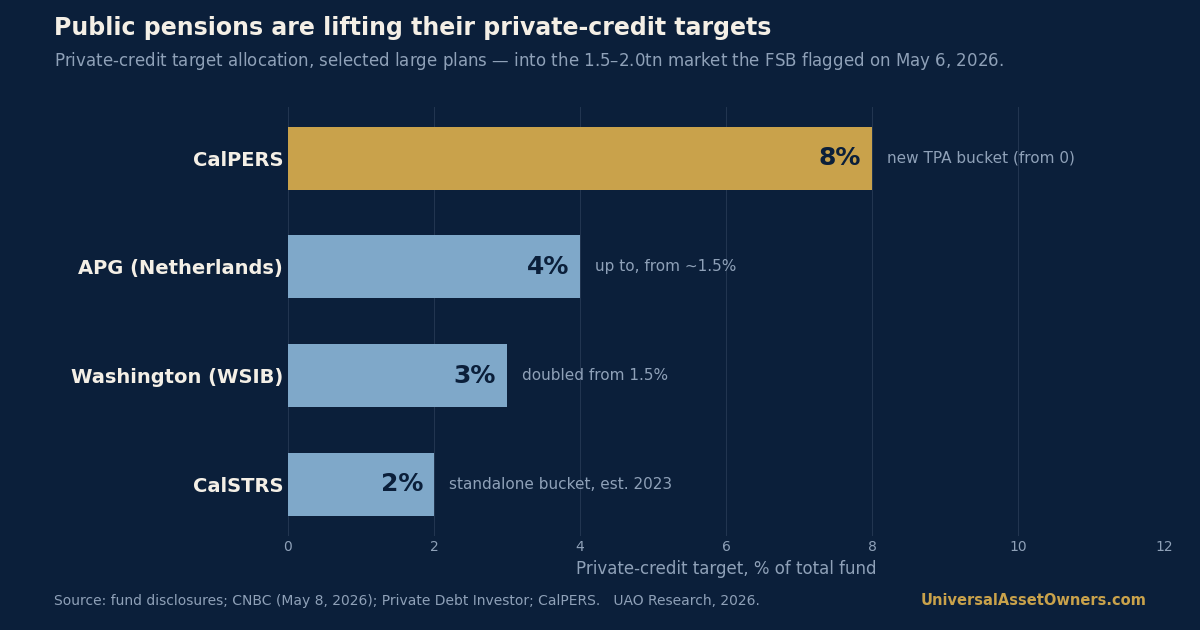

The numbers that travel with the change matter as much as the philosophy. The overhaul raises CalPERS' private-equity target to 17% and stands up a newly defined private-credit portfolio with an eventual 8% target. CalPERS frames TPA as a transparency and flexibility upgrade — the model already used by GIC, CPP Investments, Australia's Future Fund and New Zealand Super. Critics frame the same flexibility as a green light: a CalMatters commentary on May 22 called the private-markets push a "gamble" that alarms the public employees whose pensions are at stake.

For a universal owner, CalPERS is the reference case. It is the largest US plan, it discloses more than most, and where it leads, mid-sized public funds tend to follow within a cycle or two. The open question it poses to every peer: does competing all opportunities under one objective sharpen capital discipline — or simply make it easier to tilt into illiquidity when the narrative is loudest?

Source: CalPERS PERSpective, Nov 17, 2025. | Coverage: Pension Strategy Watch, this week.

2. The regulator just put a number on the risk pensions are buying.

The timing is pointed. On May 6 the Financial Stability Board published its first standalone report on vulnerabilities in private credit — the global body's clearest signal yet that the asset class large owners are crowding into deserves closer watch. The FSB sizes the market at $1.5–2.0tn at end-2024 and concentrated in a handful of jurisdictions.

Its specifics are the useful part. Roughly three-quarters of private-credit borrowers have EBITDA below $100m; reported leverage runs five to six times, but the FSB notes that EBITDA adjustments may put true leverage closer to seven times. It flags the growing share of semi-liquid vehicles offering investor redemptions — a feature that can make the sector more procyclical in stress — and "complex interlinkages" with banks, insurers and private-equity sponsors. The FSB paired the report with an action plan to close the data gaps that make these exposures hard to see at all.

The read-across for allocators is not "exit." It is that the regulator has now formally named the leverage, opacity and liquidity features that a long-horizon owner is underwriting when it writes a private-credit cheque — and that supervisory data on the sector is about to get better.

Source: Financial Stability Board, May 6, 2026.

3. Pensions are doubling down on private credit anyway — and writing bigger standalone targets.

The warning has not slowed the demand. CNBC reported on May 8 that pension funds are ramping private-credit allocations "despite deepening cracks." The targets bear it out: the Washington State Investment Board lifted its standalone private-credit target to 3% from 1.5%; Connecticut's retirement plans approved $2.75bn of new private-credit commitments for 2026; and a large Swiss pension fund is weighing up to $1.1bn in direct lending, per Bloomberg on May 20.

Two forces explain the move. Pensions are structurally suited to illiquidity — long-dated liabilities let them harvest the illiquidity premium that mark-to-market investors cannot. And after a decade of building the muscle, many now treat private credit as a core income sleeve rather than an opportunistic trade. The risk the FSB describes and the demand these funds are creating are, in other words, the same phenomenon viewed from two seats.

4. Britain hard-wires the same trade into law.

The pension-to-private-markets pipeline is now statutory in the UK. The Pension Schemes Act 2026 has received Royal Assent, handing the government a reserve power to require master trusts and group personal pensions to invest 10% of default funds in private markets — half of that, 5%, in UK assets — in line with the voluntary Mansion House Accord that 17 providers have already signed.

The safeguards are as telling as the power. It cannot be exercised before January 1, 2028, it falls away by 2035 even if used, and the Pensions Regulator can disapply it where trustees reasonably judge compliance would not serve members' interests. Ministers have signalled they would rather lean on the voluntary Accord than pull the statutory lever. For allocators, the direction of travel across the UK, Australia, the Netherlands and Canada is unmistakable: governments increasingly want pension capital steered toward domestic private assets, and they are willing to legislate the intent even where they hesitate to compel it.

Source: UK Parliament, Pension Schemes Act 2026.

5. The cushion that makes the risk-taking possible.

None of this happens in a funding vacuum. Milliman's May 2026 Pension Funding Index puts the 100 largest US corporate defined-benefit plans at a 107.8% funded ratio at the end of April, up from 105.9% a month earlier, on a trailing-twelve-month asset return of 11.31%. A surplus position is precisely what lets a plan sponsor — or a public fund in a similar posture — reach for more illiquidity rather than de-risk. The appetite for private markets is not happening despite the funding backdrop; it is partly enabled by it.

— Chart of the day —

Public pensions are lifting their private-credit targets — into a market the FSB just flagged.

Source: Fund disclosures; CNBC (May 8, 2026); Private Debt Investor; CalPERS. UAO Research, 2026.

— Take of the day —

"The total portfolio approach is the right tool and the wrong moment, at once. Dissolving asset-class silos genuinely improves how a fund weighs trade-offs — but it also removes the crude cap that used to stop a pension from over-allocating to whatever is in vogue, and what is in vogue is the asset class the FSB just warned about. The discipline TPA promises has to come from governance, not from the model; CalPERS is now the live test of whether it does."

— UAO Research.

— Three links worth your time —

- Financial Stability Board — Report on Vulnerabilities in Private Credit. The primary document behind every private-credit headline this month; read the section on semi-liquid vehicles and procyclicality.

- Thinking Ahead Institute — Total Portfolio Approach hub. The clearest account of what TPA is and where its claimed 50–100bps comes from, co-authored with the funds that pioneered it.

- CalMatters — The CalPERS gamble. The beneficiary's-eye critique of the same move — useful precisely because it argues the other side.

UAO Daily Brief. AI-assisted monitoring and drafting; reviewed and edited by the UAO editorial desk before publication. Every number is sourced to a primary document or named publication above. Not investment advice.

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Universal Owner · view the chart of the day.

Produced and edited by the UAO editorial desk. Not investment advice.