UNIVERSAL ASSET OWNERS · FLAGSHIP

There is a moment in the history of capital when the center of gravity moves. For most of the last century it sat in two cities — New York and London — where the deepest pools of savings were gathered, priced, and put to work. That center is now shifting. Not collapsing, not fleeing, but tilting, steadily and deliberately, toward the Gulf.

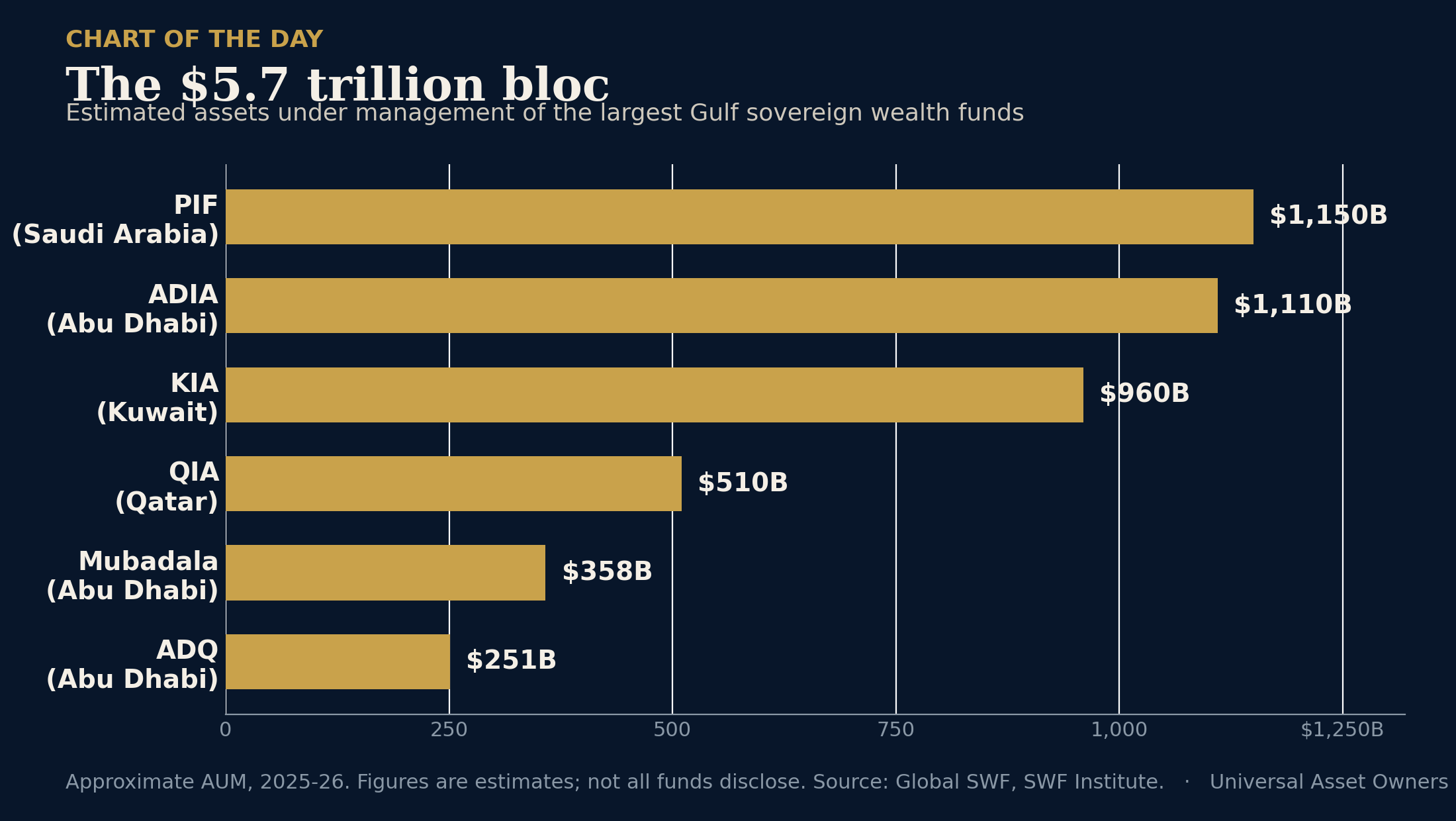

The headline figure is hard to absorb. The sovereign wealth funds of the Gulf Cooperation Council now manage roughly $5.7 trillion between them, according to Global SWF’s mid-2026 accounting. That is not a rainy-day reserve. It is a standing, permanent claim on a meaningful slice of the world’s listed companies, private businesses, infrastructure, and real estate. It is, in the truest sense of the phrase, universal-owner capital: large enough, diversified enough, and patient enough that its fortunes are bound to the global economy as a whole rather than to any single trade.

For allocators everywhere — the pension funds, endowments, insurers, and asset managers who increasingly sit across the table from this money — the relevant question is no longer whether Gulf capital matters. It plainly does. The question is whether you understand how it thinks.

A bloc, not a handful of funds

It is tempting to treat the Gulf funds as a list of names. The more useful framing is a bloc. Abu Dhabi’s ADIA holds on the order of $1.1 trillion. Saudi Arabia’s Public Investment Fund has grown past the trillion-dollar mark. Kuwait’s KIA, Qatar’s QIA, and Abu Dhabi’s Mubadala and ADQ fill out a roster that, taken together, rivals the largest national economies on earth.

Their scale is matched by their activity. In 2024, five GCC funds deployed a record $82 billion, and for the third consecutive year all five ranked among the ten most active sovereign investors in the world. Mubadala alone wrote roughly $29 billion across more than fifty deals — making a single Abu Dhabi fund the most active state investor on the planet. This is not idle reserve management. It is a deliberate, sustained programme of acquiring claims on the future.

The figures above are estimates — not every fund discloses its assets, and reasonable sources differ at the margin — but the shape of the picture is not in dispute. A small number of institutions, concentrated in a handful of Gulf capitals, now command a pool of long-term capital large enough to move markets simply by deciding where to stand.

Five funds, five strategies

Treating the bloc as a single actor is useful for grasping scale, but it obscures how differently these institutions actually behave. Each reflects the priorities of the state behind it.

Saudi Arabia’s PIF is the most overtly strategic of the group. It is less a conventional wealth fund than the financial engine of a national transformation, charged with seeding entire domestic industries — tourism, sport, entertainment, manufacturing, and giga-projects — while taking marquee positions abroad. Its mandate is explicitly developmental: build the post-oil Saudi economy, and accept that some of that capital will be patient to the point of being uncommercial in the near term.

Abu Dhabi’s ADIA sits at the opposite pole — the archetype of the diversified, globally invested, deliberately low-profile sovereign fund. It behaves much like a very large, very long-term institutional allocator, spreading capital across public equities, fixed income, private markets, real estate, and infrastructure worldwide, and prizing discretion over headlines.

Mubadala is the dealmaker, comfortable taking concentrated, direct, strategic stakes — often in technology, life sciences, and energy — and acting as an operator and partner rather than a passive holder. QIA built its name on trophy assets and global brands and has since pushed toward technology and diversification. Kuwait’s KIA, the oldest sovereign fund in the world, remains the most conservative and reserve-like of the group, a reminder that this model is not new — only newly dominant.

Read together, the differences matter as much as the totals. An asset manager pitching ADIA is selling into a diversified allocator; one pitching PIF is competing with a state-building agenda; one pitching Mubadala is negotiating with a direct investor that may prefer to lead. The capital is not monolithic, and treating it as such is the first mistake outsiders make.

The advantage is the horizon

What distinguishes this capital is not size alone. Plenty of large pools of money exist. What sets the Gulf funds apart is the length of the horizon over which they are free to think.

A corporate pension answers to a schedule of retirements. A hedge fund answers to quarterly redemptions and the risk that clients walk. An insurer answers to its liabilities and its regulator. Each of these is a perfectly rational investor, but each is, in some measure, a prisoner of its own time horizon. The largest Gulf funds are unusual in how little they are constrained that way. They are stewarding national wealth across generations — the explicit task, in several cases, of preparing an economy for the decades after hydrocarbons. That mandate changes the arithmetic of risk.

When your horizon is measured in decades, the discipline of trying to beat the market each year begins to look beside the point. You can absorb drawdowns that would force a leveraged fund to liquidate. You can hold illiquid assets — infrastructure, private companies, real estate — through cycles that would terrify an investor who has to mark to market every quarter. And you can do something almost no other investor can: you can stop trying merely to beat the market, and start trying to shape it.

What they are actually buying

The deeper story is not how much these funds spend, but what they are buying, and why. Three threads run through almost everything.

The future of energy. The irony is deliberate: even as Gulf states sell the oil and gas of today, their funds are among the most aggressive buyers of the energy system of tomorrow — grids, solar, storage, hydrogen, and the transmission that ties them together. This is not philanthropy or signalling. It is a hedge written at national scale against the very transition their export economies must survive. A universal owner cannot diversify away from the energy transition; it can only try to own both sides of it.

Intelligence. The second thread is artificial intelligence and the physical economy that underpins it. From data centers to semiconductors to the compute capacity that will power the next decade of productivity, Gulf capital has become one of the largest sources of patient funding for AI infrastructure anywhere in the world. For a long-horizon owner, this is the logical bet: if AI is the general-purpose technology of the century, you do not want to rent exposure to it. You want to own the rails.

Home. The third thread points inward. Capital that for decades flowed almost entirely outward is increasingly being put to work at home — in new cities, ports, manufacturing, tourism, and the diversified industries that are meant to outlast oil. Regional events can accelerate this turn; reports through 2026 noted that Gulf states may tilt more capital toward domestic priorities. But the structural logic predates any single shock: a fund created to prepare an economy for the post-oil era must, eventually, invest in that economy directly.

The universal owner’s dilemma, at the largest scale

Put these threads together and you arrive at the defining condition of the universal asset owner. When you own a slice of everything, you cannot trade your way around the world’s systemic risks. You are exposed to climate, to the diffusion of AI, to the reordering of global trade, to demography — not as positions you might choose to take or avoid, but as conditions you are obliged to manage. Selling out of one risk simply moves you into another, and at this size the act of selling moves the price against you.

This is why the behaviour of the Gulf funds is worth studying even by those who will never co-invest with them. They are running, in real time and at enormous scale, the experiment that every large allocator is edging toward: how to steward capital when your effective benchmark is the global economy itself, and when your decisions are large enough to bend that economy at the margin. Their answer — long horizons, real assets, ownership rather than trading, and a willingness to fund the structural shifts they cannot avoid — is becoming a template.

The case for caution

None of this is a one-way story, and a serious reader should hold the counterarguments alongside the thesis. Several are worth stating plainly.

Transparency. These funds disclose far less than the public pension and endowment world. Assets under management are often estimated rather than reported, governance is opaque by Western standards, and the line between commercial mandate and political objective is not always clear. That opacity is itself a risk for counterparties and for the funds’ own discipline.

Concentration and correlation. A bloc this large, this active, and this thematically aligned — energy transition, AI, domestic build-out — can crowd into the same assets at the same time. Patient capital is a genuine advantage, but patient capital pointed at crowded trades can still overpay, and size makes any eventual exit difficult.

Underlying exposure. However diversified the portfolios, the funding source remains tied to hydrocarbons and to the fiscal health of the sponsoring state. A prolonged downturn in energy revenues, or a domestic call on capital — reconstruction, fiscal support, or accelerated diversification spending — can turn a sovereign fund from a net buyer into a net seller. Regional security shocks add a further layer of uncertainty that a purely financial model understates.

Governance and key-person risk. Strategy concentrated in a small number of decision-makers can move fast, but it can also turn sharply, and accountability structures are thinner than those that constrain a public pension board. For partners, the question is not only what the capital wants today, but how durable that intent is.

The honest conclusion is not that the Gulf funds are unstoppable, but that they are structurally important, strategically intentional, and likely to remain so — with risks that are real and worth pricing rather than dismissing.

What it means for everyone else

For asset managers, the implication is straightforward and uncomfortable: the Gulf is no longer simply a source of mandates to be won. These funds are building internal capability, taking direct stakes, and increasingly setting terms rather than accepting them. The relationship is shifting from client-and-vendor toward partner-and-competitor.

For other asset owners — the pension and endowment world — the Gulf funds are a live case study in how to act on a long horizon without being captured by short-term noise. Few Western institutions enjoy the same freedom from near-term liabilities, but the direction of travel is shared: toward private markets, toward real assets, toward stewardship of the systems that determine long-run returns.

And for policymakers and the companies on the receiving end of this capital, the lesson is that the money now arrives with intent. It is not passive index capital. It wants board seats, technology transfer, local presence, and a say in the direction of what it owns. That is what ownership at this scale looks like.

The center of gravity has moved before, and it will move again. What is unusual about this shift is its character: capital that is not merely large, but long; not merely seeking returns, but seeking to shape the conditions that will produce them. When you own the whole market, your task is not to beat it. It is to understand — and, where you can, to shape — the future of the market itself. The Gulf’s great funds have understood that for some time. The rest of the field is only beginning to catch up.

Editorial analysis for long-duration capital. Figures are drawn from Global SWF and the SWF Institute (2025–26) and are estimates; not all funds disclose assets under management. This is journalism, not investment advice.

Voiceover transcript

There is a moment in the history of capital when the center of gravity moves. For most of the last century it sat in two cities — New York and London. That center is now shifting. Not collapsing, not fleeing, but tilting, steadily and deliberately, toward the Gulf. This is the Frontier, from Universal Asset Owners.

The headline figure is hard to absorb. The sovereign wealth funds of the Gulf Cooperation Council now manage roughly five-point-seven trillion dollars between them. That is not a rainy-day reserve. It is a standing, permanent claim on a meaningful slice of the world's listed companies, private businesses, infrastructure, and real estate.

Treat this as a bloc, not a handful of funds. Abu Dhabi's ADIA holds on the order of one-point-one trillion dollars. Saudi Arabia's Public Investment Fund has grown past the trillion-dollar mark. Kuwait's KIA, Qatar's QIA, and Abu Dhabi's Mubadala and ADQ fill out a roster that, taken together, rivals the largest national economies on earth.

Their scale is matched by their activity. In 2024, five GCC funds deployed a record eighty-two billion dollars. For the third consecutive year all five ranked among the ten most active sovereign investors in the world. Mubadala alone wrote roughly twenty-nine billion across more than fifty deals — making a single Abu Dhabi fund the most active state investor on the planet.

But the differences matter as much as the totals. Saudi Arabia's PIF is the most overtly strategic — less a conventional wealth fund than the financial engine of a national transformation. ADIA is the archetype of the diversified, globally invested, deliberately low-profile sovereign fund. Mubadala is the dealmaker, comfortable taking concentrated direct stakes. QIA built its name on trophy assets and has since pushed toward technology. Kuwait's KIA, the oldest sovereign fund in the world, remains the most conservative. An asset manager pitching ADIA is selling into a diversified allocator; one pitching PIF is competing with a state-building agenda; one pitching Mubadala is negotiating with a direct investor that may prefer to lead.

What distinguishes this capital is not size alone. It is the length of the horizon over which these institutions are free to think. A corporate pension answers to a schedule of retirements. A hedge fund answers to quarterly redemptions. The largest Gulf funds have no such constraint. Their horizon, in the truest sense, is generational.

For every allocator who competes with this capital, sits alongside it, or hopes to co-invest with it, the question is the same: do you understand how it thinks? The center of gravity is moving. The Frontier, from Universal Asset Owners.