Volume 1, Issue 37 · Wednesday, June 17, 2026 · The Universal Owner — daily intelligence for long-horizon capital.

| 🎧 Apple Podcasts | ▶ Spotify | 🎤 Podbean |

Scenario of the Day · live in the Scenario Lab  Decision Day: The Vanishing Cut. Will today’s dot plot erase the last 2026 cut? The desk puts it at roughly 80%. It’s live and at the top of the Scenario Lab. Open the Scenario Lab → |

|

Free Tool of the Day · 2 of 12

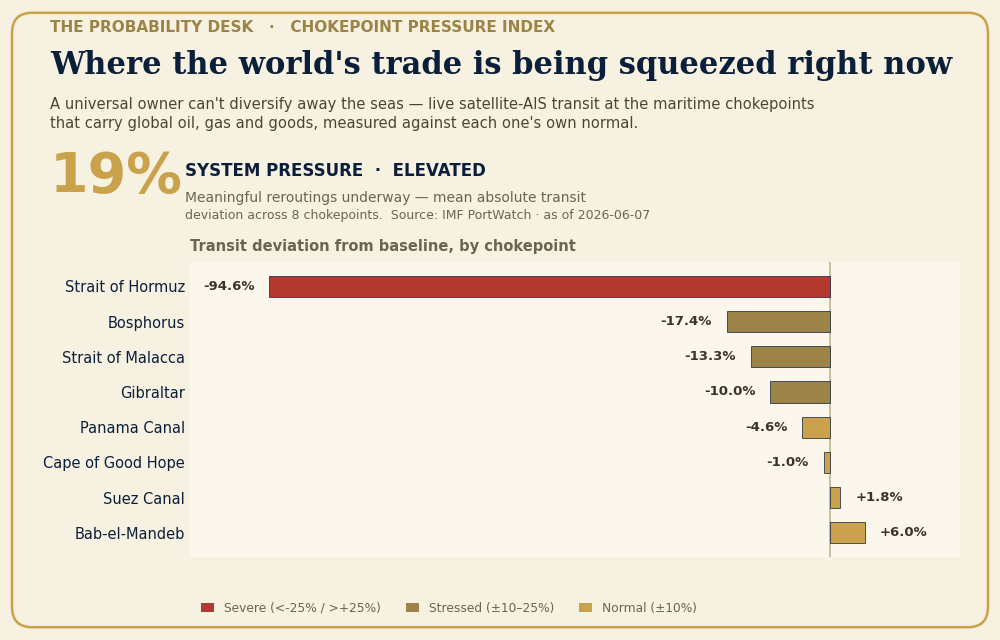

The Chokepoint Pressure Index

Today's reading: system pressure 19% (Elevated) — Hormuz still 94.6% below normal. Tap to run it live →

Today's brief turns on a single chokepoint: the Strait of Hormuz reopening, the oil price round-tripping to the high-$70s, and the disinflation the Fed may be tightening into. The Chokepoint Pressure Index puts a number on exactly that risk. It tracks the world's critical maritime and energy arteries — Hormuz, the Suez Canal and Bab-el-Mandeb, the Malacca Strait, Panama, the Taiwan Strait — and scores live pressure on each from shipping, transit and price signals. Then it shows how a closure at each one would flow through to a universal owner's book: energy, inflation, freight, and the real-asset hedges that move with them.

Pressure scores seeded from public data — IMF PortWatch transit volumes, AIS shipping density, and benchmark energy and freight spreads. Free, no login to explore.

Check today's chokepoint pressure →

|

|

From the Newsroom

Nations now treat artificial intelligence the way they once treated oil. Zubina Ahmed maps the sovereign-AI race — the US and China out front; the UK, EU, India, Singapore, Canada and a fast-moving Gulf catching up — and what "AI independence" now means for capital, security and the balance of power. A through-line for any universal owner already watching AI concentration as a systemic exposure.

Read the full report →

|

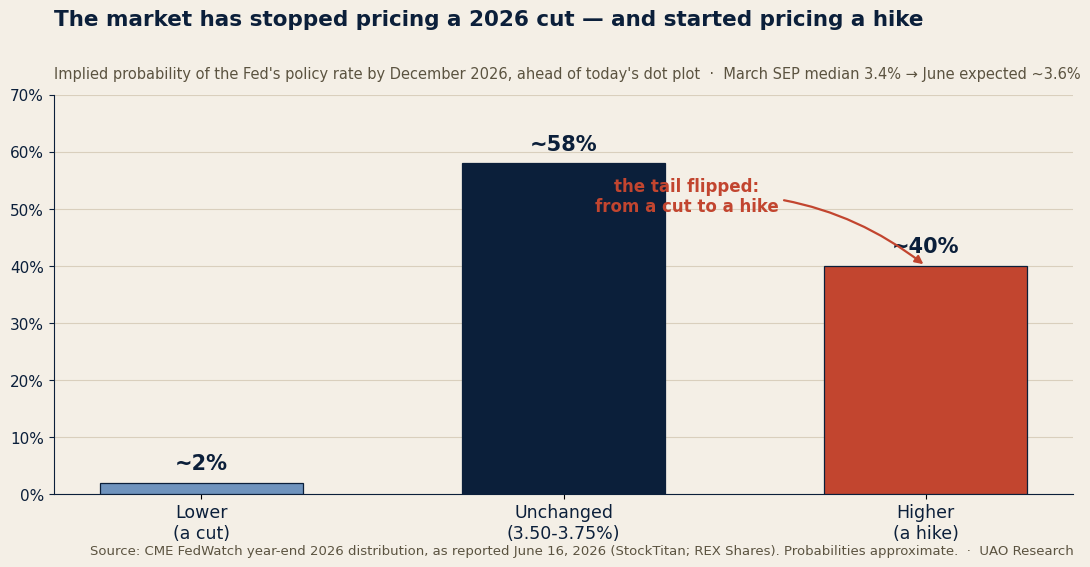

Kevin Warsh delivers his first rate decision this afternoon at 2 p.m. Eastern, and for the first time in this cycle the risk the market is hedging is not a cut the Fed won't deliver — it is a hike the Fed hasn't ruled out. Below: the dot plot that is expected to erase the last 2026 cut, an oil price in its longest losing streak of the year that is doing the disinflation the Fed may be about to fight, the long-horizon capital least troubled by any of it, and the largest US pension switching operating systems in two weeks. One chart, one take, and three links worth your time.

1. The rate is settled. The dot plot flips the tail from a cut to a hike.

The Federal Open Market Committee announces at 2 p.m. ET today, with the updated Summary of Economic Projections at 2 p.m. and Chair Warsh's first press conference at 2:30. A hold at 3.50–3.75% is priced at roughly 97%, so the rate was decided before the doors opened. The release that matters is the dot plot.

Here is what has changed in a single meeting cycle. March's dots carried one 25bp cut for 2026, with a median near 3.4%. Analysts now broadly expect that lone cut to be erased, lifting the year-end median toward 3.6%. The more striking shift is in the tail: CME FedWatch puts roughly a four-in-ten chance that the policy rate sits a quarter-point higher by December, against almost no chance of a cut, and Bank of America flags at least three members dotting hikes for 2026. Warsh, who has called the dot plot a "relic," is expected to withhold his own entry. For a universal owner this is the repricing that matters: every long-duration book built around the easing put now faces not the absence of cuts but a live hike tail it was not hedging a month ago.

Source: StockTitan — Fed Rate Decision June 17, 2026. | REX Shares — FOMC June 2026 Preview. | Coverage: Macro, today.

2. Oil is in its longest losing streak of the year — the Fed may tighten into a disinflation.

WTI fell below $78 and Brent slipped toward $80 on Tuesday, extending the year's longest run of declines as the US–Iran wind-down and the Strait of Hormuz reopening hold. Brent was above $113 in March; the supply shock that put the energy contribution into May's 4.2% inflation print is unwinding in real time.

That sharpens the awkwardness of this afternoon. If the committee removes its last cut — or signals a hike tail — on the strength of a 4.2% print, it is leaning hawkish exactly as the largest driver of that print collapses underneath it. For an owner of the whole economy the read-across cuts both ways: cheaper energy eases the headline and supports the consumer, but it also strips value from the commodity and real-asset hedges that only worked while the shock was live. The hedge and the risk were the same position — and the position is now unwinding into a hawkish meeting.

Source: Trading Economics, crude oil, June 16, 2026. | Oilprice.com — Brent crude futures.

3. Higher-for-longer rewards the capital that never had to leave.

A hawkish dot plot is a stress test of who can actually hold illiquid assets through a repricing — and the answer increasingly runs through the Gulf. The UAE's three largest sovereign vehicles — ADIA, the Investment Corporation of Dubai, and Mubadala — are projected to grow from about $1.97tn in assets in 2025 to roughly $2.77tn by 2030, an increase of nearly $800bn. Mubadala was the most active sovereign wealth fund in the world in 2024, deploying about $29bn, while PIF pulled its external spend back 37% to focus capital at home. Across nearly every major fund, technology and AI-linked capacity have become the consensus allocation theme.

This is the capital least disturbed by a missing cut. A fund underwriting a thirty-year horizon with limited liquidity needs does not have to mark a take-private to this quarter's discount rate. When the rate path turns against leverage, the owners with the longest duration and the deepest balance sheets do not just survive the repricing — they set the clearing price on the assets everyone else is forced to sell or stop bidding for.

Source: Khaleej Times — UAE sovereign fund assets, 2025. | Gulf News — Mubadala 2024 deployment. | Coverage: Gulf Capital Briefing.

4. CalPERS switches operating systems in two weeks — into exactly this test.

On July 1 the largest US public pension, with more than $556bn in assets, replaces its strategic asset-allocation framework with a Total Portfolio Approach, judging each strategy by its contribution to the whole fund rather than holding it to a fixed per-asset-class target. The board approved the change last November; CalPERS is the first US public pension to make the switch.

The timing now looks pointed in a way it did not a month ago. A total-portfolio model arrives precisely as a hawkish Fed makes holding illiquidity through volatility both more valuable and more dangerous. Does the new framework give a CIO genuine flexibility to hold private assets through a repricing — or does it quietly loosen the discipline that fixed ceilings used to impose, at the worst possible moment to loosen anything?

Source: Markets Media, June 2026. | Pensions & Investments. | Coverage: Pension Strategy Watch.

5. A Maple-8 pension just marked its credit book to a 3.1% year.

PSP Investments closed fiscal 2026 (to March 31) with net assets of C$320.6bn, up 7%, a one-year net return of 6.5% and a ten-year annualised 8.8% that beat its benchmark — a solid long-horizon record from one of Canada's Maple-8. The number that should travel further is buried in the asset-class table: PSP's credit book returned just 3.1% on the year, against a 10.5% five-year and 11.1% ten-year run-rate. Private equity returned 5.3%; real estate fell 7.3%.

PSP did not blame AI; it attributed a soft one-year (5.2% below its reference portfolio) to a tougher environment for private markets and to public-market benchmarks that diverge from private marks over short horizons. But the read-across is exactly the one this brief's deep-dive makes: when the rate path stops being kind, the private-credit book is where the repricing shows up first. The open question for every allocator — and the one the FSB flagged in its May private-credit vulnerabilities report — is whether a 3.1% credit year is a cyclical dip or the first mark of the lending book meeting a higher-for-longer rate path and, eventually, the AI disruption to borrowers that Zubina Ahmed maps in today's newsroom piece.

Source: PSP Investments, fiscal 2026 results, June 16, 2026. | The Globe and Mail, June 16, 2026. | Coverage: Pension Strategy Watch.

— Chart of the day —

The market has stopped pricing a 2026 cut — and started pricing a hike.

Source: CME FedWatch year-end 2026 distribution and March 2026 SEP dot plot, as reported June 16, 2026 (StockTitan; REX Shares; Tech Times). Probabilities approximate. UAO Research, 2026.

— Take of the day —

"For a year the trade was that the Fed would ease more than it admitted. This afternoon that trade inverts: the dots erase the last cut, the tail becomes a hike, and the oil price doing the real disinflation is falling too fast for a hawkish committee to credit. Position for the easing put to be gone — not deferred — and for the next surprise to come from data the Fed is about to under-weight, not over-weight." |

— UAO Research.

— Three links worth your time —

- StockTitan — Fed Rate Decision June 17, 2026: What to Watch. The cleanest checklist for the 2 p.m. SEP and Warsh's 2:30 debut.

- REX Shares — FOMC June 2026 Preview: The decision is settled, the dot plot isn't. Why the median dot and the hike tail are the whole event.

- Markets Media — CalPERS is the first US pension to adopt a Total Portfolio Approach. The governance change that goes live two weeks from today.

*UAO Daily Brief. Researched and edited by the UAO editorial desk. Not investment

When the Easing Put Expires

Research & Commercial Insight · The Universal Owner Risk Radar

The question: If this afternoon's dot plot erases the last 2026 cut and prices a hike tail, what does that do to a universal owner who cannot rebalance fast — and who has spent a year leaning, quietly, on a Fed put that is about to expire?

For most of the past year the long-horizon allocator could carry a comfortable contradiction. Inflation was sticky, the Fed was hawkish in its words, and yet the market — and the implied discount rate underneath every private-asset mark — kept a cut in the front window. That cut was a cushion. It told a CIO that the next move in the cost of money was down, that today's illiquidity would be refinanced into easier conditions, and that the duration in the book was a bet with the wind behind it. At 2 p.m. Eastern today, that cushion is expected to be removed.

What the evidence says. The shift is not subtle and it has happened fast. March's Summary of Economic Projections carried a single 2026 cut, a median policy rate near 3.4%. Heading into this meeting, analysts broadly expect that cut to disappear and the year-end median to rise toward 3.6% (REX Shares, June 2026). The tail has moved further still. CME FedWatch now assigns roughly a four-in-ten probability that the rate is a quarter-point higher by December, against almost no probability of a cut, and Bank of America counts at least three committee members dotting hikes for the year (StockTitan, June 17, 2026). Chair Warsh, who has described the dot plot as something that should become "a relic," is expected to withhold his own dot — removing the one number the market would most like to anchor to. The rate decision is a 97% hold; the entire event is the distribution, and the distribution has inverted.

The awkward part is the data underneath. The energy spike that put the 4.2% into May's inflation print is unwinding: WTI fell below $78 and Brent toward $80 this week, the longest losing streak of the year, with Brent down from above $113 in March (Trading Economics, June 16, 2026). A committee that hardens its stance today is doing so as the largest input to the print it is reacting to falls away beneath it.

The disagreement. Here the picture refuses to resolve, and the unresolved part is the interesting part. One reading is that the Fed is right to remove the cut and even flirt with a hike: services inflation is sticky, the labour market has not cracked, and an easing put that the market keeps re-pricing is itself a source of financial-stability risk that a credible new chair should want gone. The opposite reading is that the Fed is about to make a textbook error — tightening into a disinflation it cannot yet see because it is buried in lagging data, and doing so on the authority of a chair who has just told the market not to trust the forecasts the meeting produces. Both can be argued from the same numbers, which is exactly why the long end is volatile and the dot plot, not the rate, is the event.

For a universal owner the disagreement is not academic, because the owner cannot trade around it at speed. A sovereign fund or a large pension carries a private-markets book it values quarterly and exits over years, a liability stream measured in decades, and an allocation it can shift only at the margin each year. It does not get to be tactically long or short the dot plot. It has to hold whatever the dot plot does — which means the only honest question is whether the portfolio was built to survive the put expiring, or merely built to enjoy it while it lasted.

What it means from the allocator's seat. Three implications follow, and they pull against each other.

First, the marks have not caught up to the rate path, and a hawkish dot plot widens that gap. If the discount rate the market applies to long-duration private assets resets higher today and stays there, the carrying values in many books are describing a cost of money that no longer exists. The allocator underwriting new vintages against last year's realised IRRs — struck when a cut was still in the window — is quietly overpaying. The honest base case after today is lower forward returns on exactly the long-duration, illiquid assets that a universal owner holds most of.

Second, higher-for-longer is a sorting mechanism, and it sorts by balance sheet. The capital that can hold illiquidity through a repricing without being forced to sell — Gulf sovereigns growing toward $2.77tn by 2030, funds with thirty-year horizons and limited liquidity calls — does not just endure a hawkish turn; it gets to set the clearing price on the assets that leveraged or liquidity-constrained holders are forced to let go (Khaleej Times, 2025). The universal owner's edge is supposed to be duration. A put-free rate path is the environment that finally pays it — but only for the owners who genuinely have it and have not spent it on leverage.

Third — and this is the governance point a board should not duck — the discipline question and the rate question have arrived in the same fortnight. CalPERS switches to a Total Portfolio Approach on July 1, dropping fixed per-asset-class ceilings in favour of judging each strategy by its contribution to the whole fund (Markets Media, 2026). A total-portfolio lens is a better description of how risk compounds. It is also a looser leash, and it is being unclipped exactly as a hawkish Fed makes holding illiquidity through volatility both more valuable and more dangerous. The model should be adopted because it is true, not because it makes it easier to keep holding what a fixed ceiling would have forced a board to trim.

What to watch next. Three markers. Whether the long end treats a removed cut as already-priced or as a genuine repricing — the move in the ten-year after 2 p.m. tells you how much easing put was still embedded. Whether Warsh's first press conference frames the missing cut as conviction or as data-dependence dressed up, because a chair who distrusts his own dots has to substitute something for them. And whether the funds with real duration use a hawkish summer to buy what the constrained are forced to sell — the single clearest signal of who was built for the put to expire and who was only renting it.

The universal owner's discomfort today is the right discomfort. For a year the easing put quietly subsidised duration. When it expires this afternoon, the portfolios that were built to need it and the portfolios that were built to outlast it stop looking alike — and the rate path, for once, pays the owner who actually owned the horizon.

Sources

- StockTitan — Fed Rate Decision June 17, 2026: What to Watch.

- REX Shares — FOMC June 2026 Preview: The decision is settled, the dot plot isn't.

- Trading Economics — Crude oil, June 16, 2026.

- Khaleej Times — UAE's top sovereign wealth fund assets set to jump by nearly Dh3 trillion in 5 years.

- Markets Media — CalPERS is the first US pension to adopt a Total Portfolio Approach, 2026.

▶ Listen: The Universal Owner on Apple, Spotify or Podbean · 📊 Scenario Lab

UAO Daily Brief. Researched and edited by the UAO editorial desk. Not investment advice. Contact: info@universalassetowners.com.