The gatekeeper for Sweden's public pension savers has decided private credit will not get near them — and he said so out loud. That single "no," delivered days after the world's two top financial-stability bodies mapped the same fault line, is the cleanest statement yet of the question every long-horizon owner now faces: is the liquidity private credit promises real, or is it the next thing the market discovers it doesn't have? Below: the refusal, the regulatory weather behind it, the largest US public plan leaning the other way on Monday — plus the chart of the day and three links worth your time.

🎧 Listen to today's edition. The Universal Owner walks through today's brief — and a deeper take on why the second-round losses land on pension balance sheets, not banks — in about twelve minutes. Follow on Spotify or listen on the site — one tap, and every morning's episode comes to you.

1. Sweden's pension gatekeeper draws a line: no private credit on the public platform.

The cleanest risk signal of the week is a refusal. Erik Fransson, who runs the Swedish Fund Selection Agency — the body that curates the fund menu for Sweden's roughly SEK 1.4 trillion premium pension system — said this week he does not expect private credit to be offered to savers any time soon: "that's long into the future, if that's possible at all." His reason was structural, not ideological: "Private market structures with daily liquidity are usually a recipe for difficulties."

It is a small decision with a large meaning. A gatekeeper whose entire job is to decide what retail-pension capital may buy looked at the fastest-growing corner of private markets and declined — specifically on the mismatch between products that offer frequent redemptions and assets that do not trade. The agency has spent the past year running competitive procurements worth more than SEK 150 billion to raise the quality of its menu; this is what that scrutiny produces when it reaches private credit.

For a universal owner, the read-across is not "Sweden is cautious." It is that the liquidity terms — not the credit losses — are where a serious allocator now expects the trouble to start.

Source: Bloomberg, "Sweden's Top Pension Gatekeeper Wants to Keep Private Credit Out," June 10, 2026. | Coverage: The Universal Owner Risk Radar, this week.

2. The gatekeeper isn't alone — the watchdogs spent five weeks mapping the same crack.

Fransson's caution has institutional company. In its May 6 report, the Financial Stability Board put the private credit market at $1.5–2 trillion and warned that its leverage, opacity and bank linkages could amplify stress in adverse scenarios. The European Central Bank's Financial Stability Review, published later in May, went further on the specific mechanism: semi-liquid vehicles such as business development companies have faced sizeable redemption requests since the start of 2026, and some have capped withdrawals at their contractual gates — exactly the daily-liquidity problem Stockholm flagged.

Treat both as labelled background, not breaking news: the FSB report is five weeks old and the ECB's a few days younger. But their timing is the point. When a national pension gatekeeper and the two bodies charged with watching the system independently arrive at the same worry inside a month, the burden of proof shifts to the allocators still adding exposure.

Source: Financial Stability Board, "Report on Vulnerabilities in Private Credit," May 6, 2026.

3. CalPERS reviews its private-debt program on Monday — leaning in as gatekeepers pull back.

The tension becomes concrete next week. On June 15, the CalPERS Investment Committee — stewards of roughly $598 billion — takes a scheduled program-strategy review of its Private Debt book, alongside private equity, real estate and infrastructure. CalPERS built private debt into a deliberate, fast-growing allocation; Monday's session is where the largest US public plan restates how hard it intends to keep pressing.

That is the whole Risk Radar question in one calendar week. A European gatekeeper keeps the asset class out of reach of savers on liquidity grounds; a US plan of comparable systemic weight reviews how much further to lean in. Both are acting rationally from their own seat — and only one of them can be reading the liquidity risk correctly. Watch the framing in the agenda materials, not the headline allocation number.

Source: CalPERS, Investment Committee meeting agenda, June 15, 2026.

4. The migration the gate is meant to slow.

Step back and the direction of travel is unmistakable. Sovereign-wealth-fund-backed deal value rose 198% to $199.9 billion in 2025, while pension-backed deal value slipped 5.5% to $74.3 billion — the long-horizon world moving deeper into private, illiquid assets from both ends. That standing trend (2025 full-year data) is the current Stockholm is pushing against, not a fresh event. The faster the migration into instruments that don't trade, the more a single "no" on liquidity terms is worth reading closely.

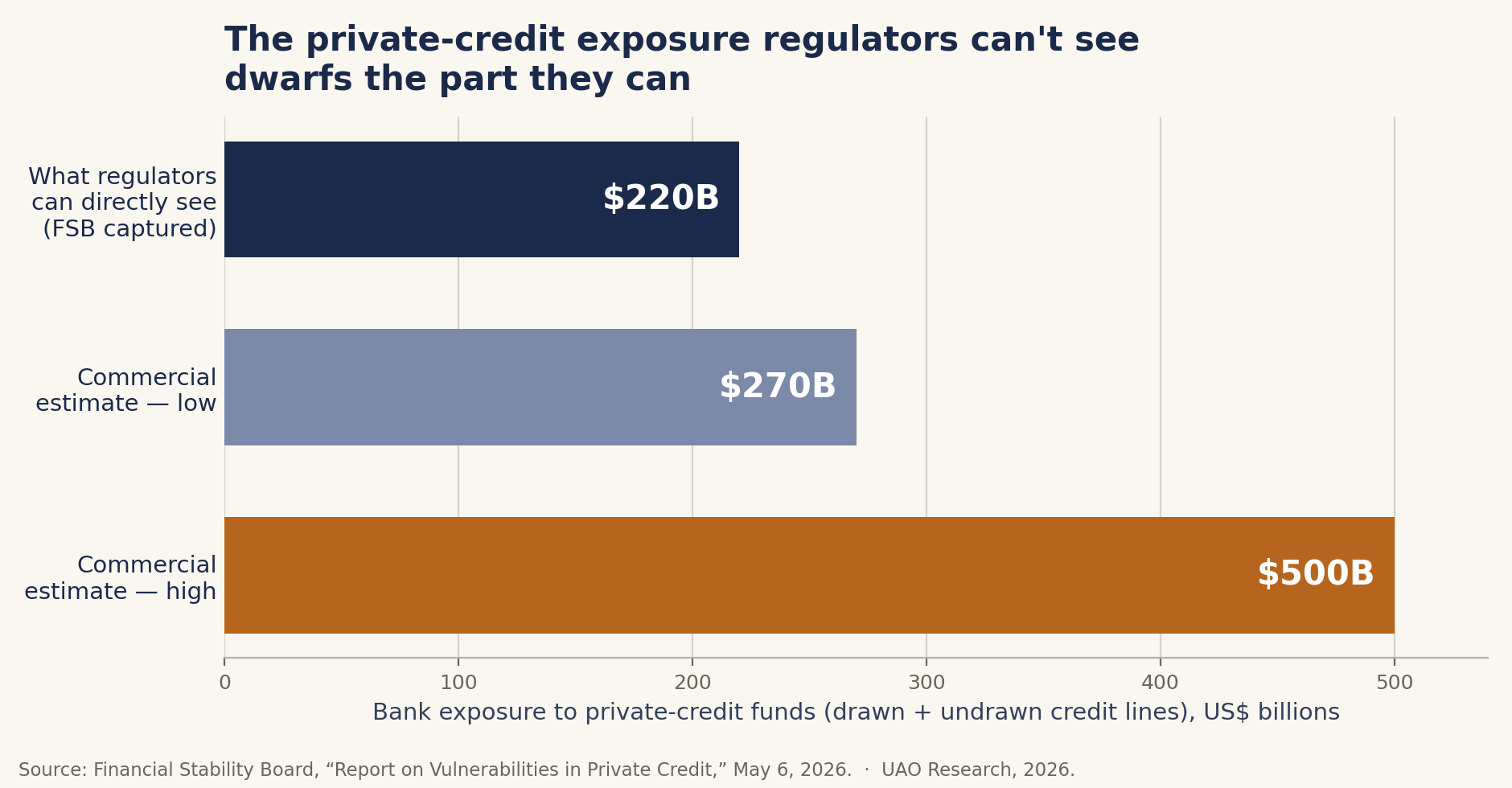

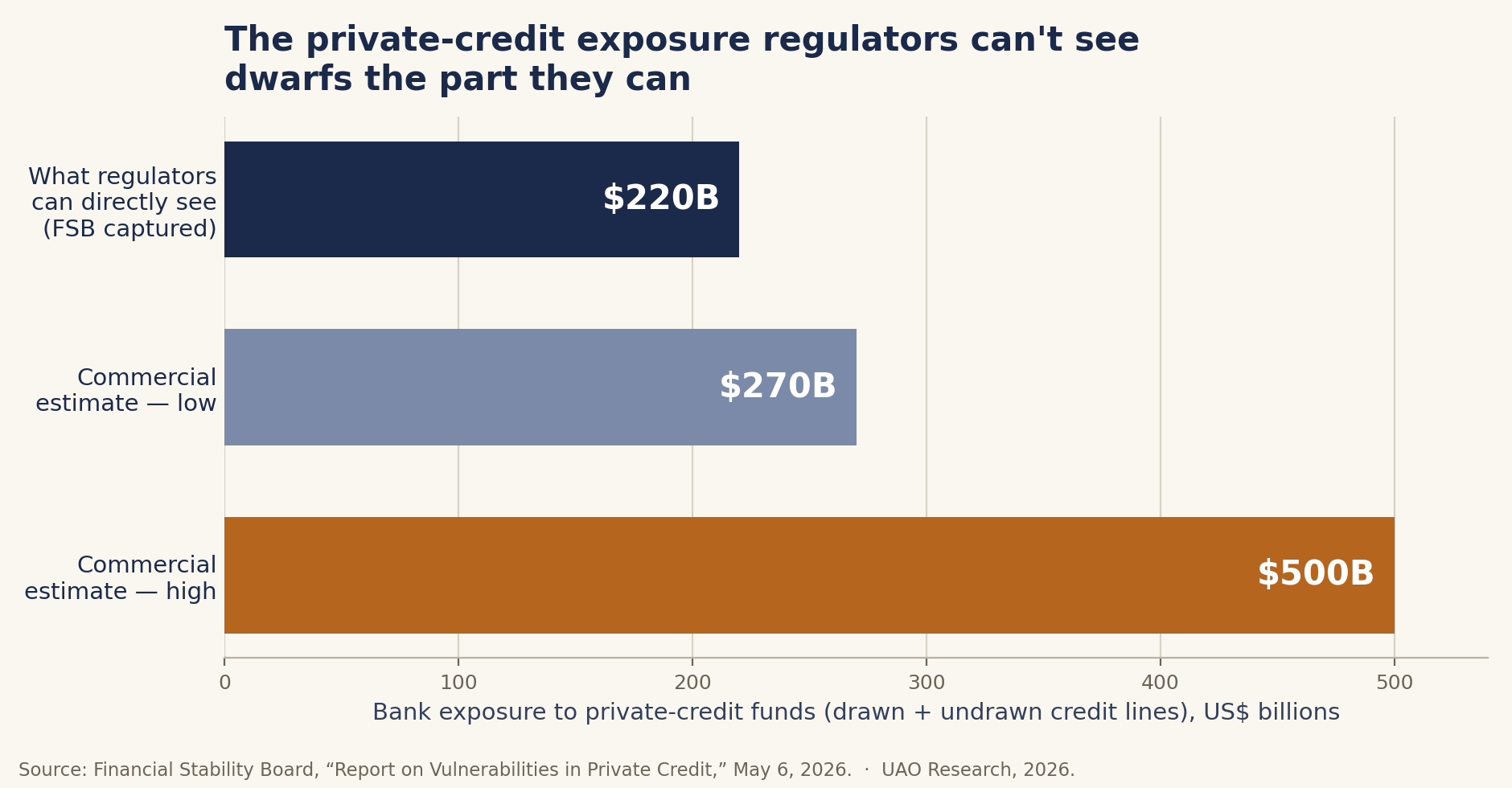

— Chart of the day —

Regulators can directly see about $220 billion of bank exposure to private credit. The market thinks the real number is closer to $500 billion.

Source: Financial Stability Board, "Report on Vulnerabilities in Private Credit," May 6, 2026. UAO Research, 2026.

— Take of the day —

"The instructive thing about Sweden's 'no' is what it is not about. It is not a call on credit quality or default rates — it is a call on plumbing. The gatekeeper is betting that the first failure in private credit will be a liquidity failure, not a solvency one: redemptions a fund cannot meet on the terms it promised. For a universal owner that cannot diversify away from the system, that is the more dangerous kind, because it is the kind that spreads through forced selling into the public assets you also own."

— UAO Research.

— Three links worth your time —

- European Central Bank — "Stress in global private credit markets and its implications for euro area financial stability" (Financial Stability Review). The one stress exercise that puts a number on who actually absorbs the loss — and it isn't the banks.

- Financial Stability Board — "Report on Vulnerabilities in Private Credit." The primary document behind today's chart; read the data-gap section if nothing else.

- Bloomberg — "Sweden's Top Pension Gatekeeper Wants to Keep Private Credit Out." The interview that frames the week — a gatekeeper saying the quiet part out loud.

The Universal Owner Risk Radar runs every Friday. Reply to this email with a tip or a correction — we publish corrections within 24 hours. Contact: info@universalassetowners.com.