Volume 1, Issue 27. Saturday, June 6, 2026. Sent 7:00 am ET / 14:00 GST.

The largest single commitment to India's data-centre sector this year is also a reminder of who is now underwriting the AI buildout: long-horizon institutional capital. On Friday a Blackstone- and pension-backed operator pledged thirty billion dollars to add five gigawatts of compute capacity; this weekend's edit reads that deal against two things it does not solve — a Gulf sovereign sector that is spending faster than before the war, and an electricity system that, on the regulators' own numbers, is becoming the binding constraint on the whole project. Plus the chart of the day and three links worth your time.

▶ Watch the video briefing

▶ Watch the video briefing1. A Blackstone- and pension-backed operator just pledged $30 billion to build five gigawatts of AI data centres in India.

On Friday, June 5, AirTrunk — the Asia-Pacific hyperscale data-centre operator owned by Blackstone and the Canada Pension Plan Investment Board — said it would invest US$30 billion to build more than five gigawatts of new data-centre capacity across India by 2030. The company announced the commitment after chief executive Robin Khuda met Prime Minister Narendra Modi, who called it one of the largest commitments yet to India's digital-infrastructure sector; the Indian government framed the figure as roughly ₹3 trillion. AirTrunk entered the Indian market earlier this year through its acquisition of Lumina CloudInfra.

For a universal owner, the ownership chain is the story. This is not a tech company spending its own cash flow; it is a portfolio company of a global private-markets manager and one of the world's largest pension funds, deploying patient capital into an asset that behaves like infrastructure — long-dated, capital-intensive, contracted. That is precisely the profile allocators have been chasing as they rotate from public equities into real assets. Five gigawatts is a serious number: roughly the continuous draw of a mid-sized national grid's worth of demand, concentrated in one country over four years.

The open question is not whether the capital exists — Friday proved it does — but whether the power, the permits and the water to run five gigawatts will arrive on the same schedule as the cheque. That is the subject of today's deep-dive.

Source: AirTrunk, June 5, 2026. | Coverage: the weekend edit, this week.

2. Gulf sovereign funds spent close to $26 billion in three months — and did not slow down for the war.

The other pool of capital underwriting global assets this spring is the Gulf, and the latest read shows no retreat. In a report dated June 1, the data house Global SWF found that the five biggest Gulf sovereign investors — Saudi Arabia's Public Investment Fund, the UAE's Mubadala and Abu Dhabi Investment Authority, Qatar's QIA and Abu Dhabi's Lunate — deployed almost $26 billion across March, April and May 2026, with the bulk flowing into developed-market assets. Global SWF noted these vehicles had "shown no sign of slowdown (yet), with a stronger average pace in the past quarter than in the five years before the start of the war."

The expectation in Washington and Brussels had been the opposite: that the conflict with Iran would pull Gulf capital home to shore up domestic budgets and defence. The data, as reported by Fortune on June 2, says it has not. PIF skewed toward emerging markets (about $6.1 billion) while Mubadala and ADIA leaned into developed markets; collectively the funds manage some $5.7 trillion.

For an allocator, the read-across is twofold. First, the Gulf remains a price-setter in the large private and infrastructure deals universal owners co-invest in — including, increasingly, AI infrastructure. Second, the war has not yet repriced that capital's risk appetite, which means the geopolitical premium the rest of the market is paying may not be showing up where the largest sovereign cheques are written.

Source: Fortune, June 2, 2026.

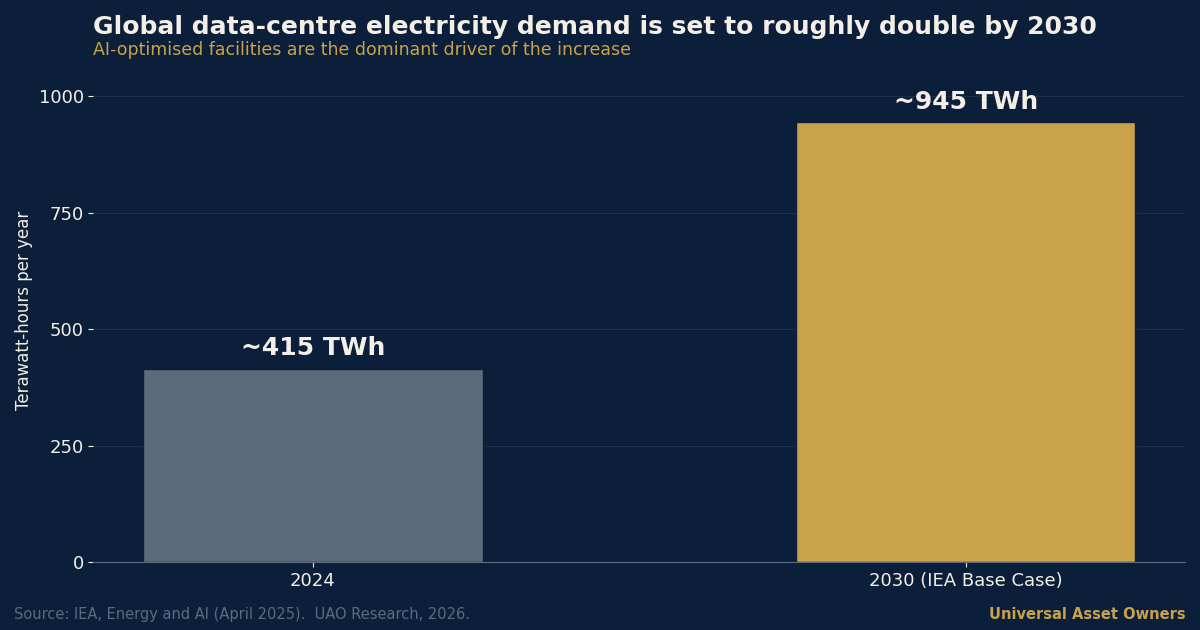

3. The binding constraint on all of this is increasingly the grid, not the cheque.

Read the AirTrunk pledge against the most authoritative power numbers and the tension is immediate. In its Energy and AI special report, published April 10, 2025, the International Energy Agency projected global data-centre electricity consumption roughly doubling to about 945 terawatt-hours by 2030 — just under three per cent of world electricity — with AI-optimised facilities the dominant driver. The IEA's own framing is that grid limitations, not demand or capital, are increasingly what slows the buildout.

The evidence is already on the ground. Interconnection queues in the United States stretch years; Ireland has imposed a de-facto cap on new data-centre grid connections around Dublin; concentration points such as Northern Virginia and Singapore are running into local power limits. A five-gigawatt commitment is therefore a power-procurement problem as much as a construction one — and for the pension and sovereign owners behind these assets, the return depends on securing firm electricity at a predictable price over the asset's life. That is a different risk than the deal headline suggests.

Source: International Energy Agency, April 10, 2025.

4. The exposure is not optional for a universal owner — it is already in the portfolio.

The same long-horizon capital building data centres is also the capital that owns the demand side of AI, directly and through managers. GIC co-led Anthropic's $30 billion Series G at a $380 billion post-money valuation in February 2026; across 2025, the five largest hyperscaler spenders committed more than $355 billion of AI-related capital expenditure — the largest single-cycle private infrastructure outlay in modern memory. A universal owner holds the index, so it holds the concentration: it cannot diversify away from a buildout this large becoming either the engine of returns or the source of the next impairment.

Source: GIC, February 12, 2026.

— Chart of the day —

Global data-centre electricity demand is set to roughly double by 2030 — which is the ceiling every gigawatt of new compute runs into.

Source: IEA, Energy and AI, April 2025. UAO Research, 2026.

— Take of the day —

"The AirTrunk pledge proves the capital is not the scarce input anymore — electricity is. For the pension and sovereign owners now financing AI infrastructure, the durable return will accrue to whoever locks in firm power at a known price for twenty years, not to whoever announces the biggest number. Underwrite the megawatts, not the headline."

— UAO Research.

— Three links worth your time —

- International Energy Agency — Energy and AI (special report). The single best primary source on why power, not capital, is the constraint on the compute supercycle.

- Global SWF — Latest news and league tables. The running record of where sovereign and pension capital is actually being deployed, with the methodology stated.

- S&P Global — Sovereign wealth fund private-market deals soar, pension activity slows. Useful context on the divergence between SWF and pension dealmaking pace.

The UAO Daily Brief is produced by Universal Asset Owners — intelligence for long-horizon capital. AI-assisted monitoring and drafting; reviewed and edited by the UAO editorial desk before publication. Not investment advice. Reach the desk at info@universalassetowners.com.

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Allocator Briefing · view the chart of the day.

Produced and edited by the UAO editorial desk. Not investment advice.

More from today: listen to The Universal Owner · watch the video briefing · the chart of the day.

Produced and edited by the UAO editorial desk. Editorial analysis for long-duration capital — not investment advice.