Volume 1, Issue 26. Friday, June 5, 2026. Sent 7:00 am ET / 14:00 GST.

The risk that should keep a long-horizon owner up at night is no longer any single fault line — it is several of them breaking together. That is the message from the global financial-stability watchdog's June meeting, and this Friday's Risk Radar reads it against the places the strain is already visible: a private-credit market posting record defaults even as pension funds keep adding to it, and the world's largest fund's stewardship engine sitting idle while its rulebook is rewritten. Plus the chart of the day and three links worth your time.

▶ Watch the video briefing

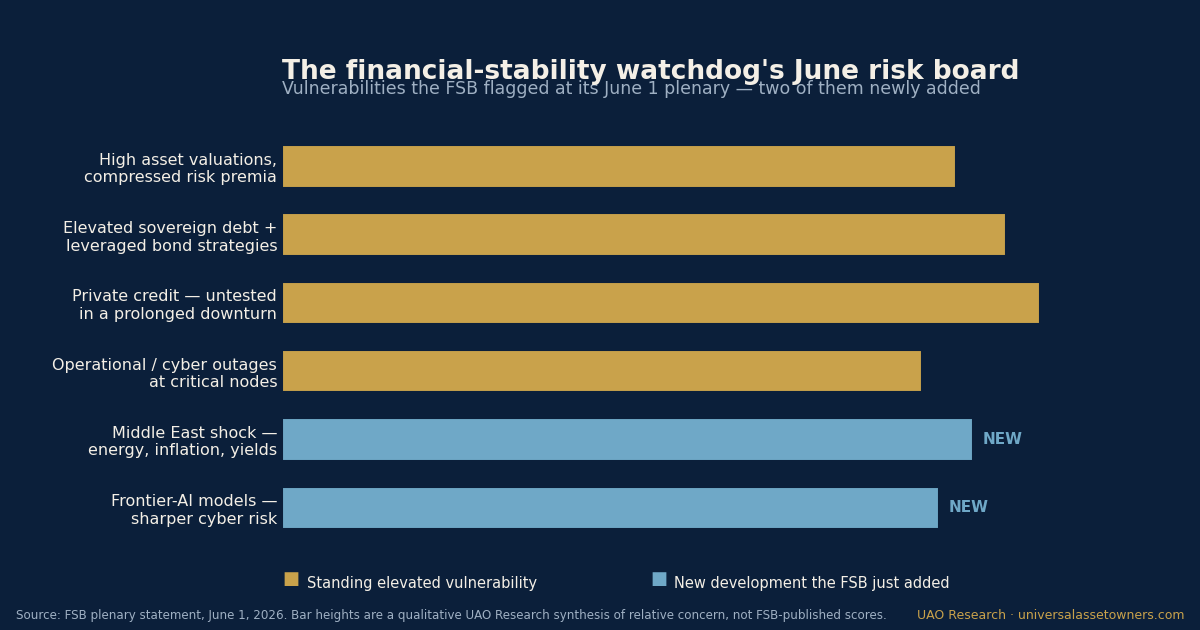

▶ Watch the video briefing1. The Financial Stability Board's new worry is correlation — and it named two fresh shocks to the list.

Meeting in London on June 1, the Financial Stability Board — the body that coordinates financial regulation across 24 jurisdictions for the G20 — used its plenary statement to shift the framing of systemic risk. The danger it stressed was not a single vulnerability but their coincidence: members "expressed particular concern that a combination of shocks could concurrently trigger multiple vulnerabilities, threatening financial stability." Asset valuations remain high and risk premia compressed; sovereign debt is elevated with shortening maturities and a growing use of leveraged trading strategies in government-bond markets; and private credit "has grown rapidly, and parts of the sector remain untested in a prolonged economic downturn."

To that standing list the FSB added two developments it said had "further complicated the risk landscape." First, the conflict in the Middle East — energy and commodity markets, higher inflation, and rising bond yields. Second, the arrival of powerful frontier AI models, which the board warned "may sharply increase cyber risks." "There is growing concern over new vulnerabilities to global financial stability," said FSB Chair Andrew Bailey, the Bank of England governor.

For a universal owner, the operative word is concurrently. A portfolio stress-tested against one shock at a time can still be fragile to two arriving together — a commodity-price spike that lifts yields while a cyber outage freezes a critical market node. The FSB is telling allocators to test the joints, not just the limbs.

Source: Financial Stability Board, June 1, 2026. | Coverage: The Universal Owner Risk Radar, Friday, this week.

2. The vulnerability the FSB keeps flagging is already showing up in the data.

The private-credit warning is not abstract. In its dedicated report of May 6, 2026, the FSB sized the global private-credit market at roughly $1.5–2.0 trillion in assets at end-2024, "heavily concentrated in a few jurisdictions," and warned that its "complexity, leverage, and interconnectedness could amplify stress in adverse scenarios." The report singled out valuation opacity, reliance on private credit ratings — increasingly from "lesser-known providers" — and the procyclical risk in funds that offer investors redemption options against illiquid assets.

The stress markers have begun to print. In a report released May 18, 2026, Fitch Ratings put the US private-credit default rate at a record 6.0% for the 12 months to end-April — 99 default events, 81 of them first-time defaulters — and earlier in the year several semi-liquid private-credit funds received redemption requests exceeding their stated withdrawal limits, prompting managers to restrict withdrawals. The asset class the regulator describes as "untested in a prolonged downturn" is getting an early, partial test — and the gates are the tell.

Source: Financial Stability Board, May 6, 2026.

3. Pension funds are still adding to the asset class the regulators just flagged.

Here is the governance tension on the trustee's desk. Even as the FSB and the IMF warn on private credit, retirement institutions keep raising allocations — drawn by yields the public markets no longer offer. As reported on May 8, 2026, pension funds are "doubling down" on private credit "despite deepening cracks," and on May 20 one of Switzerland's largest pension funds was reported to be weighing up to $1.1 billion in direct lending. The IMF has separately warned that insurers and pension funds using leverage against private credit "could face larger-than-expected losses during periods of stress."

The read-across is not that private credit is uninvestable — it is that the due-diligence burden has moved. A board adding to an asset class its own regulator calls opaque, leveraged, and untested owns the obligation to look through to valuation methodology, redemption terms, and the rating provider behind the number. The yield is visible; the risk, by the regulators' own account, is not.

4. The world's largest fund's stewardship engine is paused.

While the systemic dials flash, the single most-watched stewardship machine in the world is in a holding pattern. Norway's parliament has suspended new exclusion and observation decisions for its roughly $2-trillion Government Pension Fund Global while a committee chaired by former central-bank governor Svein Gjedrem reviews the ethical framework underpinning the fund's responsible-investment guidelines, with a report due October 15, 2026. Under the temporary guidelines, Norges Bank cannot add new companies to its exclusion or observation lists — though it may revoke prior exclusions; reporting has tied the pause to the prospect of excluding large technology holdings.

The fund's voting and engagement continue, but its sharpest tool — the threat of divestment that moves boards because the buyer of last resort is the world's largest single equity owner — is sheathed pending the review. For the universal-owner community that takes its cues from Oslo, the question is whether a months-long pause leaves a stewardship vacuum at precisely the moment the FSB is warning that governance and resilience matter most.

Source: Chief Investment Officer, 2026.

— Chart of the day —

The financial-stability watchdog's June risk board — the vulnerabilities it now ranks elevated, and the two it just added.

Source: FSB plenary statement, June 1, 2026. UAO Research synthesis, 2026.

— Take of the day —

"The FSB's shift from listing vulnerabilities to warning about their coincidence is the whole story. A universal owner's real exposure is not private credit, or sovereign-debt leverage, or a cyber outage — it is the correlation between them that no single risk model prices well. The discipline this demands is unglamorous: stop asking what each risk does alone, and start asking which two arrive together."

— UAO Research.

— Three links worth your time —

- Financial Stability Board — Report on Vulnerabilities in Private Credit (PDF). The primary document behind the warning — read the sections on valuation opacity and redemption procyclicality before your next private-credit commitment.

- International Monetary Fund — Global Financial Stability Report, April 2026, Chapter 1. The IMF's parallel mapping of private-credit leverage and the insurer-pension channel — the academic spine under the FSB's headline.

- CNBC — Why pension funds are doubling down on private credit despite deepening cracks. The clearest narrative read on why retirement boards keep buying the risk the regulators keep flagging.

The UAO Daily Brief is produced by Universal Asset Owners — intelligence for long-horizon capital. Read the archive and The Universal Owner Risk Radar franchise at universalassetowners.com. Questions, corrections, or to reach the desk: info@universalassetowners.com. Not investment advice.

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Allocator Briefing · view the chart of the day.

Produced and edited by the UAO editorial desk. Not investment advice.

Daily Oracle Brief

The Probability Desk’s governed read on the state of the world — the structural risks a universal owner carries, and what moved today.

2026-06-05 · model run 2026-06-05 17:21 UTC · 10 structural risks · radar load 8.3/100

The state of the world

The desk is tracking 10 structural risks at a combined radar load of 8.3/100 — 8 rising, 1 easing this run. The dominant vector is geopolitical fragmentation (a security premium repricing trade & energy), followed by market & capital regime. Read together, the board describes a world becoming less hedge-able and more security-priced: the diversification, globalization and disinflation dividends that quietly underwrite long-horizon return assumptions are eroding at the same time. For an owner of the whole market, the through-line is that systemic, cross-asset risk is migrating from the tails toward the base case — while the very tools used to hedge it (long bonds, geographic diversification, insurance, the dollar's exorbitant privilege) are each, separately, under quiet strain.

Forces, ranked by where capital is most exposed:

- Geopolitical fragmentation — a security premium repricing trade & energy (mean 59%, ▲ +14.0pp this run)

- Market & capital regime — the diversification & capital-cycle dividend fading (mean 26%, ▼ -2.0pp this run)

- Climate & resource stress — physical risk migrating into collateral & sovereigns (mean 40%, ▲ +11.0pp this run)

- Monetary & fiscal order — the dollar anchor & fiscal space eroding (mean 32%, ▲ +7.0pp this run)

- Demographic gravity — aging suppressing real rates, growth & the bid (mean 32%, ▲ +5.0pp this run)

What moved

- Chokepoint concentration as a standing factor (Hormuz + Taiwan + Malacca + Panama) 59.0% (+14pp) — Brent crude

- Transition-mineral & grid-interconnection bottleneck caps electrification / AI 43.0% (+5pp) — Copper (global price)

- Pension-system inversion 33.0% (+5pp) — 10y-2y curve

In focus: Chokepoint concentration as a standing factor (Hormuz + Taiwan + Malacca + Panama)

Governed estimate 59.0% (sourced prior 45.0%, +14pp from live signals; confidence 5/5; tail-priority 24.8).

The prior is a documented base rate — At least one portfolio-material maritime-chokepoint disruption (Hormuz / Suez-Bab-el-Mandeb / Malacca / Panama / Taiwan) in a rolling 3-year window (Systemic impacts of disruptions at maritime chokepoints (Nature Communications)).

Why a universal owner should care (consequence chain):

- A single strait disrupts ~20% of oil/LNG or container flow

- Freight + insurance + energy cost-push

- Inflation/rates repricing

- Route diversification capex; friend-shoring

- Globalization dividend in return assumptions erodes

Blind spot the desk is investigating

Surfaced by the source-gated simulation leg. It carries 0% weight on any published probability — it tells us what to investigate, not what is true.

- Insurance/freight cost-push as a distinct inflation channel — Agents separated war-risk premia + re-routing from the energy shock; this leg persists even when crude round-trips. (investigate: size historical insurance/freight cost-push vs oil in past chokepoint episodes; add to inflation stress test)

- Friend-shoring eroding the globalization dividend in CMAs — Recurring agent theme: low-vol, high-duration repricing of the return premium embedded in long-horizon assumptions. (investigate: quantify globalization-dividend assumption in our return model; sensitivity to friend-shoring)

What it means

For universal owners: Treat correlation-regime risk as a base case, not a tail: the bond hedge and the 60/40 may not cushion the next equity drawdown.

For sovereigns & SWFs: Reserve diversification and the erosion of dollar privilege argue for a deliberate currency and gold posture, not drift.

For pensions: Demographic gravity (aging, net-seller inflection, low real rates) is the long anchor — funding and contribution policy should assume it.

Explore it yourself: open the Scenario Lab (universalassetowners.com/scenario-lab/) to see any scenario as a live relationship map and put your own questions to the sovereign-wealth allocator, the pension CIO, the reinsurer and the markets desk.

Read the full reasoning behind any number at the Oracle (universalassetowners.com/oracle/) and the live board at the Command Center (universalassetowners.com/command-center/). Probabilities are the desk's analytical estimates, fused from public-source signals through a transparent, explainable model; they are not forecasts of certainty. Editorial scenario analysis for long-duration capital — not investment, actuarial, legal or financial advice.

More from today: listen to The Universal Owner · watch the video briefing · the chart of the day.

Produced and edited by the UAO editorial desk. Editorial analysis for long-duration capital — not investment advice.