Volume 1, Issue 25. Thursday, June 4, 2026. Sent 7:00 am ET / 14:00 GST.

The wartime test most allocators expected the Gulf to fail, it passed: through the Iran conflict, the region's sovereign funds kept deploying, and most of the money went to developed markets. Today's brief reads the June capital-flow map — where Gulf state capital actually went, the split opening up inside the Gulf itself, the official reserve managers quietly stepping the other way on the dollar, and why healthy-looking emerging-market inflows are not what they seem. Plus the chart of the day and three links worth your time.

▶ Watch the video briefing

▶ Watch the video briefing1. The Gulf didn't flinch — sovereign funds kept deploying through the war, mostly into developed markets.

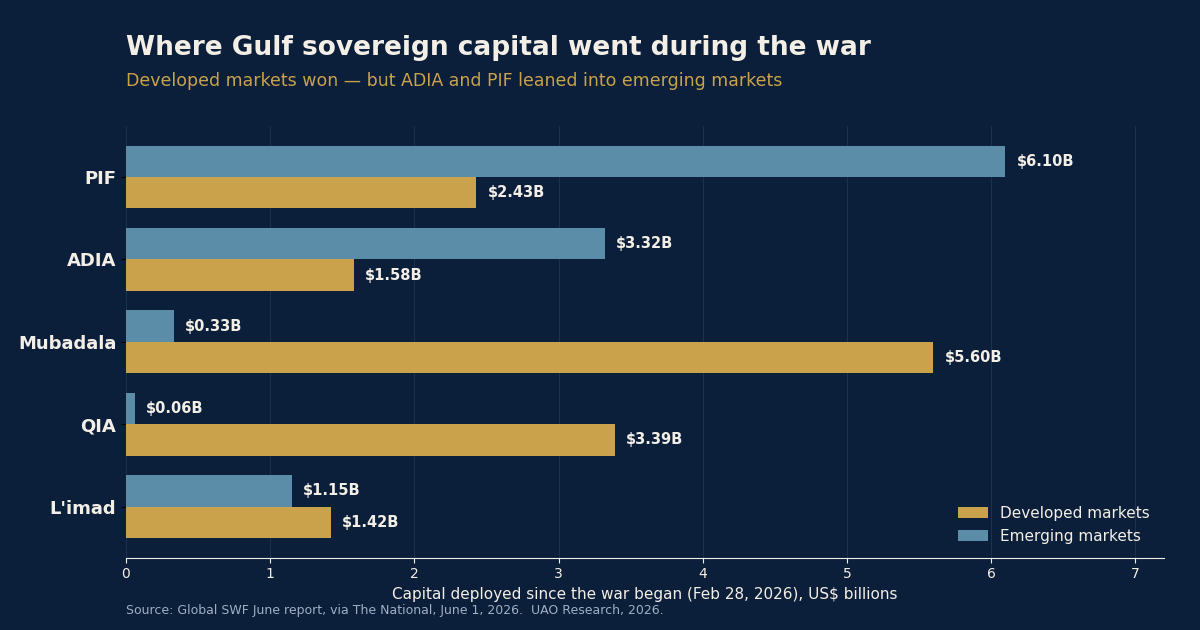

The Iran war that began on February 28 was supposed to slow the Gulf's biggest investors down. It did not. In its June report, the tracker Global SWF found that the state funds of the six-member Gulf Co-operation Council — managing about $5.7 trillion between them — held their quarterly investment pace, with most of the capital flowing into developed-market assets, chiefly the United States. "These vehicles have shown no sign of slowdown yet, with a stronger average pace in the past quarter than in the five years before the start of the war," Global SWF said.

The per-fund numbers, dated to the months since the war began, are striking. Abu Dhabi's Mubadala put more than $5.6 billion into developed markets against just $330 million in emerging markets; Qatar's QIA, $3.39 billion developed versus $60 million emerging; Abu Dhabi's newly created L'imad platform, $1.42 billion developed versus $1.15 billion emerging. Only QIA trimmed its overall pace, running about $2 billion lighter per quarter since March 1.

For a universal owner, the read-across is about behavior under stress. The largest discretionary pools of state capital in the world treated a regional war not as a reason to retreat to cash but as cover to keep adding long-duration exposure abroad — and they voted, with real money, for developed markets.

Source: The National, June 1, 2026. | Coverage: Capital Flow Watch, Thursday, this week.

2. Inside the Gulf, the money is splitting — only ADIA and PIF are leaning into emerging markets.

The same Global SWF data shows the Gulf is not moving as a bloc. The two largest funds broke from the developed-market herd: Saudi Arabia's Public Investment Fund, with assets approaching $1 trillion, put $6.1 billion into emerging markets against $2.43 billion in developed markets since the war began; Abu Dhabi's ADIA, estimated by Global SWF at roughly $1.1 trillion, deployed $3.32 billion to emerging markets versus $1.58 billion developed. "The capital has continued to flow into US companies and funds, with only ADIA and PIF showing a preference for China and other emerging markets," the report said.

That divergence matters because it is the two biggest, most sophisticated balance sheets in the region taking the contrarian side. When the largest sovereign investors tilt toward emerging markets while their peers crowd into US assets, allocators should at least ask which group is early and which is comfortable.

Source: The National, June 1, 2026.

3. The counter-current: official reserve managers are easing off the dollar even as private money pours into US assets.

Set the Gulf's developed-market buying against what the official sector is doing and a split appears. In research published in May 2026, OMFIF found the dollar had fallen sharply in central banks' demand rankings, with roughly 70% of reserve managers citing the US political environment as a deterrent and gold ranking as the most-demanded reserve asset. The hard data points the same way: US Treasury International Capital figures for March 2026 showed foreign official institutions net-sold about $14.9 billion of long-term Treasuries even as private foreign investors bought $111.4 billion (both figures dated to the March release).

The picture is a public-versus-private divergence in who finances the United States. Rules-based reserve managers are diversifying away from the dollar for reasons of sanctions risk and resilience; discretionary private and sovereign capital keeps adding US exposure for return. A universal owner sits on both sides of that line at once.

Source: OMFIF, May 2026. · U.S. Treasury TIC, March 2026.

4. Emerging-market inflows look healthy — but the gains are official money, not private conviction.

The headline number flatters the trend. The Institute of International Finance projects non-resident flows to emerging markets rising to about $935 billion in 2026, up from roughly $887 billion in 2025. But it expects private non-resident flows to fall, with the projected increase driven almost entirely by official flows to Argentina and Ukraine. Strip out the policy-driven money and the broad private appetite for emerging-market risk is thinner than the aggregate suggests.

That is the through-line of today's brief: capital that persists is increasingly selective. Whether it is the Gulf concentrating in US assets, reserve managers leaving the dollar, or official lenders carrying emerging-market inflows, the flows are being made deliberately, fund by fund and policy by policy — not as a single tide.

Source: Institute of International Finance, 2026.

— Chart of the day —

Where Gulf sovereign capital went during the war — developed markets won, but ADIA and PIF leaned the other way.

Source: Global SWF June report, via The National, June 1, 2026. UAO Research, 2026.

— Take of the day —

"The Gulf's wartime buying and the official sector's dollar diversification are not contradictory — they are the same signal seen from two seats. Discretionary capital is paid to take the US exposure that rules-based reserve managers are now paid to reduce. The universal owner's job is not to pick a side but to recognize that 'safe haven' has quietly become a relative, position-dependent idea rather than a fixed address."

— UAO Research.

— Three links worth your time —

- Fortune — The opposite is true: the Iran conflict didn't curb the Gulf's appetite for global investments. The clearest narrative read on why wartime uncertainty failed to slow Gulf deployment.

- IMF — Capital Flows to Emerging Markets: Disentangling Quantities from Prices (WP 2026/060). The analytical case that emerging-market flows are now driven by idiosyncratic, not common, shocks — selectivity as structure.

- Reason — Bernie Sanders' AI sovereign-wealth-fund proposal, dissected. A skeptical look at the June 2 bill to seed a US sovereign fund with AI-company equity — sovereign-capital ideas are going mainstream in Washington.

The UAO Daily Brief is produced by Universal Asset Owners — intelligence for long-horizon capital. Read the archive and the Capital Flow Watch franchise at universalassetowners.com. Questions, corrections, or to reach the desk: info@universalassetowners.com. Not investment advice.

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Allocator Briefing · view the chart of the day.

Produced and edited by the UAO editorial desk. Not investment advice.

Daily Oracle Brief

The Probability Desk’s governed read on the state of the world — the structural risks a universal owner carries, and what moved today.

2026-06-04 · model run 2026-06-04 15:02 UTC · 10 structural risks · radar load 8.3/100

The state of the world

The desk is tracking 10 structural risks at a combined radar load of 8.3/100 — 8 rising, 1 easing this run. The dominant vector is geopolitical fragmentation (a security premium repricing trade & energy), followed by market & capital regime. Read together, the board describes a world becoming less hedge-able and more security-priced: the diversification, globalization and disinflation dividends that quietly underwrite long-horizon return assumptions are eroding at the same time. For an owner of the whole market, the through-line is that systemic, cross-asset risk is migrating from the tails toward the base case — while the very tools used to hedge it (long bonds, geographic diversification, insurance, the dollar's exorbitant privilege) are each, separately, under quiet strain.

Forces, ranked by where capital is most exposed:

- Geopolitical fragmentation — a security premium repricing trade & energy (mean 59%, ▲ +14.0pp this run)

- Market & capital regime — the diversification & capital-cycle dividend fading (mean 26%, ▼ -2.0pp this run)

- Climate & resource stress — physical risk migrating into collateral & sovereigns (mean 40%, ▲ +11.0pp this run)

- Monetary & fiscal order — the dollar anchor & fiscal space eroding (mean 32%, ▲ +7.0pp this run)

- Demographic gravity — aging suppressing real rates, growth & the bid (mean 32%, ▲ +5.0pp this run)

What moved

- Chokepoint concentration as a standing factor (Hormuz + Taiwan + Malacca + Panama) 59.0% (+14pp) — Brent crude

- Transition-mineral & grid-interconnection bottleneck caps electrification / AI 43.0% (+5pp) — Copper (global price)

- Pension-system inversion 33.0% (+5pp) — 10y-2y curve

In focus: Chokepoint concentration as a standing factor (Hormuz + Taiwan + Malacca + Panama)

Governed estimate 59.0% (sourced prior 45.0%, +14pp from live signals; confidence 5/5; tail-priority 24.8).

The prior is a documented base rate — At least one portfolio-material maritime-chokepoint disruption (Hormuz / Suez-Bab-el-Mandeb / Malacca / Panama / Taiwan) in a rolling 3-year window (Systemic impacts of disruptions at maritime chokepoints (Nature Communications)).

Why a universal owner should care (consequence chain):

- A single strait disrupts ~20% of oil/LNG or container flow

- Freight + insurance + energy cost-push

- Inflation/rates repricing

- Route diversification capex; friend-shoring

- Globalization dividend in return assumptions erodes

Blind spot the desk is investigating

Surfaced by the source-gated simulation leg. It carries 0% weight on any published probability — it tells us what to investigate, not what is true.

- Insurance/freight cost-push as a distinct inflation channel — Agents separated war-risk premia + re-routing from the energy shock; this leg persists even when crude round-trips. (investigate: size historical insurance/freight cost-push vs oil in past chokepoint episodes; add to inflation stress test)

- Friend-shoring eroding the globalization dividend in CMAs — Recurring agent theme: low-vol, high-duration repricing of the return premium embedded in long-horizon assumptions. (investigate: quantify globalization-dividend assumption in our return model; sensitivity to friend-shoring)

What it means

For universal owners: Treat correlation-regime risk as a base case, not a tail: the bond hedge and the 60/40 may not cushion the next equity drawdown.

For sovereigns & SWFs: Reserve diversification and the erosion of dollar privilege argue for a deliberate currency and gold posture, not drift.

For pensions: Demographic gravity (aging, net-seller inflection, low real rates) is the long anchor — funding and contribution policy should assume it.

Explore it yourself: open the Scenario Lab (universalassetowners.com/scenario-lab/) to see any scenario as a live relationship map and put your own questions to the sovereign-wealth allocator, the pension CIO, the reinsurer and the markets desk.

Read the full reasoning behind any number at the Oracle (universalassetowners.com/oracle/) and the live board at the Command Center (universalassetowners.com/command-center/). Probabilities are the desk's analytical estimates, fused from public-source signals through a transparent, explainable model; they are not forecasts of certainty. Editorial scenario analysis for long-duration capital — not investment, actuarial, legal or financial advice.

More from today: listen to The Universal Owner · watch the video briefing · the chart of the day.

Produced and edited by the UAO editorial desk. Editorial analysis for long-duration capital — not investment advice.