Volume 1, Issue 24. Wednesday, June 3, 2026. Sent 7:00 am ET / 14:00 GST.

In four weeks, on July 1, two of the most-watched public funds in the United States enact opposite bets on private markets — and they are not alone. Today: the fiscal-year turn that splits large allocators on whether private assets still pay; Alaska Permanent's CIO making the most candid bear case among big owners; the larger group of pensions still building private-credit targets into the new year; and the Financial Stability Board's May warning on a $1.5–2.0 trillion market it admits it cannot yet see clearly. The through-line for a universal owner is uncomfortable: the people who hold capital the longest no longer agree on whether the illiquidity premium is real — and they are acting on opposite conclusions at the same boundary.

▶ Watch the video briefing

▶ Watch the video briefing1. On July 1, the largest U.S. public funds move in opposite directions on private markets.

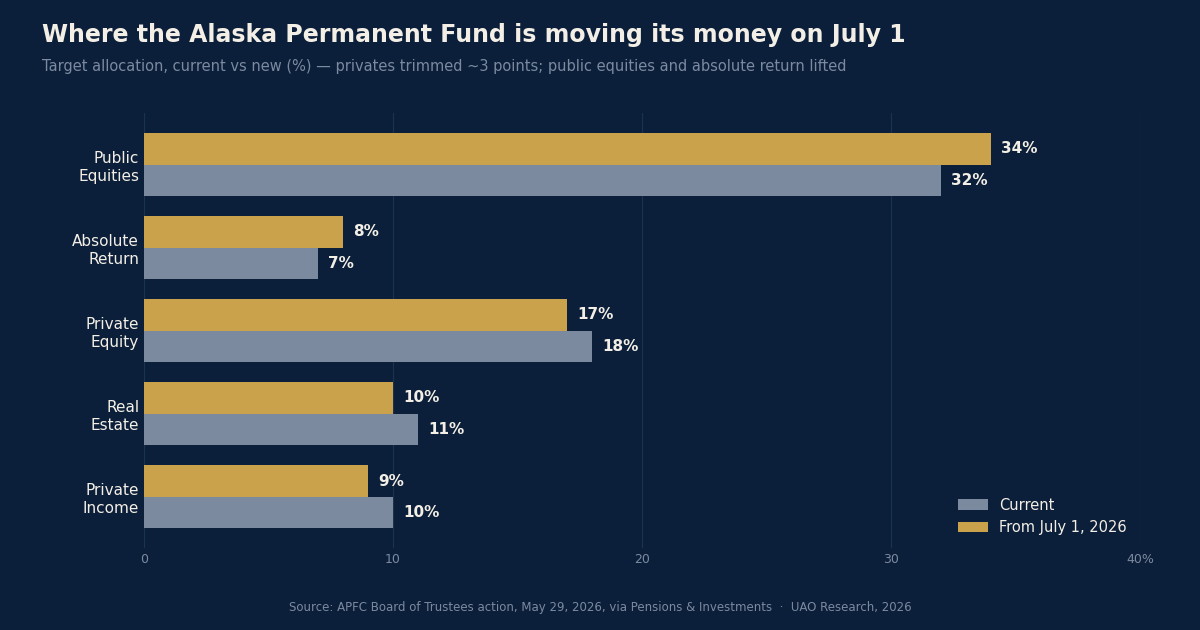

The fiscal-year boundary on July 1 will mark a rare public split between sophisticated long-horizon owners. The Alaska Permanent Fund's board approved a recalibration — effective that day — that lifts public equities to 34% and absolute-return strategies to 8%, and trims private equity to 17%, real estate to 10% and private income to 9%, a cut of roughly three points across private markets. The same day, the $556 billion California Public Employees' Retirement System switches from a strategic asset-allocation model to a Total Portfolio Approach, judging the whole fund against a single 75/25 equity-bond reference portfolio rather than asset-class benchmarks.

These are not the same decision, but they rhyme: both are large, watched funds rebuilding how — and how much — they hold illiquid private assets, and doing it at the turn of the fiscal year. For a universal owner, the signal is that the consensus of the past decade, that long-dated capital should keep migrating into private markets, is no longer a consensus. The clearing price for private assets is set by exactly these buyers; when they disagree this openly, every other allocator is taking a side whether it means to or not.

Source: Pensions & Investments, May 2026. | Coverage: Pension Strategy Watch, this week.

2. Alaska's CIO is making the most candid bear case among large allocators — and voting his allocation.

Marcus Frampton, the Alaska Permanent Fund's chief investment officer, has been the bluntest large-fund skeptic on private markets, describing the asset class as "flashing red" and arguing the illiquidity premium investors once earned has "evaporated." His evidence is concrete: U.S. mid-market buyouts now trade at mid-teens multiples of EBITDA, against the five-to-six times he saw earlier in his career, and he has cut the fund's private-equity commitments by roughly half since 2021. The May 29 board action makes that view portfolio policy from July 1.

The reason this matters beyond Alaska is that Frampton is not a marginal voice — he runs one of the better-regarded U.S. public funds and is acting against the grain of his peers. When a respected owner says the premium for locking up capital has gone, and reduces exposure rather than re-underwriting it, the burden of proof shifts to the funds still adding. The question every CIO now has to answer in writing is whether they are being paid for illiquidity, or merely accepting it.

Source: Private Markets Insights, May 2026.

3. Most public pensions are leaning the other way — building private-credit targets into the new fiscal year.

The larger group of public funds has spent the spring moving the opposite direction. The Washington State Investment Board set a standalone private-credit target of 3%, up from 1.5%; Connecticut's retirement plans committed roughly $2.75 billion to private credit en route to lifting the allocation from 6% to 10% by 2029; and Virginia's retirement system added more than $1 billion in new private-credit commitments. Across the institutional base, new inflows into private-credit vehicles held near $300 billion in 2025, broadly steady on the year, according to Mercer.

For a universal owner, the divergence is the story. The same asset class is being trimmed by one disciplined fund as a deteriorating trade and built up by many others as a structural income source. Both cannot be fully right, and the gap between them is not noise — it is a live disagreement about whether the spread on private credit still compensates for its illiquidity and its opacity. A CIO co-investing alongside either camp is implicitly underwriting one reading of that question.

Source: Private Investment Works, May 6, 2026.

4. The regulator's backdrop: the FSB used its May report to flag a market it cannot yet see clearly.

The split is unfolding over a sector its own overseers admit they cannot fully measure. The Financial Stability Board's Report on Vulnerabilities in Private Credit, published May 6, estimated the market at $1.5–2.0 trillion in assets at the end of 2024 and warned of complex interlinkages with banks, valuation opacity, leverage embedded in multi-layered structures, and liquidity terms that could make the sector procyclical in stress. Data collected from FSB members captured roughly $220 billion of drawn and undrawn credit lines — but the body's own estimate is that the true figure is more than twice that.

That gap between what regulators can see and what exists is the part a long-horizon owner should sit with. A market this large that is "untested in a prolonged downturn," in the FSB's words, is not a reason to avoid it — pensions are precisely the investors built to hold through a cycle. But it is a reason to demand the disclosure, the covenants and the liquidity terms that make holding through a cycle survivable. The funds adding exposure into July 1 are betting they have those terms; the FSB's report is a reminder that, system-wide, no one can yet confirm it.

Source: Financial Stability Board, May 6, 2026.

— Chart of the day —

Where the Alaska Permanent Fund is moving its money on July 1.

Source: APFC Board of Trustees action, May 29, 2026, via Pensions & Investments. UAO Research, 2026.

— Take of the day —

"The private-markets consensus that defined a decade of pension investing has quietly fractured at the top. When one of the most respected public CIOs calls the illiquidity premium gone and trims, while his peers keep building, the disagreement itself is the signal — and it tells universal owners that 'add privates' has stopped being a default and become a decision that has to be defended on terms, price and liquidity, not on faith in the asset class."

— UAO Research.

— Three links worth your time —

- Financial Stability Board — Report on Vulnerabilities in Private Credit. The primary document behind this week's debate — read the data-gap section, not just the headline.

- OECD — Pension Markets in Focus 2025. The scale frame: $70 trillion in global pension assets, and where it actually sits.

- Institutional Investor — Alaska's CIO on being contrarian. The fullest articulation of the bear case from inside a large fund.

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Allocator Briefing · view the chart of the day.

Produced and edited by the UAO editorial desk. Not investment advice.

Daily Oracle Brief

The Probability Desk’s governed read on the state of the world — the structural risks a universal owner carries, and what moved today.

2026-06-03 · model run 2026-06-03 15:36 UTC · 10 structural risks · radar load 7.8/100

The state of the world

The desk is tracking 10 structural risks at a combined radar load of 7.8/100 — 6 rising, 1 easing this run. The dominant vector is geopolitical fragmentation (a security premium repricing trade & energy), followed by market & capital regime. Read together, the board describes a world becoming less hedge-able and more security-priced: the diversification, globalization and disinflation dividends that quietly underwrite long-horizon return assumptions are eroding at the same time. For an owner of the whole market, the through-line is that systemic, cross-asset risk is migrating from the tails toward the base case — while the very tools used to hedge it (long bonds, geographic diversification, insurance, the dollar's exorbitant privilege) are each, separately, under quiet strain.

Forces, ranked by where capital is most exposed:

- Geopolitical fragmentation — a security premium repricing trade & energy (mean 59%, ▲ +14.0pp this run)

- Market & capital regime — the diversification & capital-cycle dividend fading (mean 24%, ▼ -6.0pp this run)

- Climate & resource stress — physical risk migrating into collateral & sovereigns (mean 37%, ▲ +4.0pp this run)

- Monetary & fiscal order — the dollar anchor & fiscal space eroding (mean 32%, ▲ +7.0pp this run)

- Demographic gravity — aging suppressing real rates, growth & the bid (mean 32%, ▲ +5.0pp this run)

What moved

- Chokepoint concentration as a standing factor (Hormuz + Taiwan + Malacca + Panama) 59.0% (+14pp) — Brent crude

- Pension-system inversion 33.0% (+5pp) — 10y-2y curve

- Insurance retreat to collateral repricing 39.0% (+4pp) — GDACS current hazards (all)

In focus: Chokepoint concentration as a standing factor (Hormuz + Taiwan + Malacca + Panama)

Governed estimate 59.0% (sourced prior 45.0%, +14pp from live signals; confidence 5/5; tail-priority 24.8).

The prior is a documented base rate — At least one portfolio-material maritime-chokepoint disruption (Hormuz / Suez-Bab-el-Mandeb / Malacca / Panama / Taiwan) in a rolling 3-year window (Systemic impacts of disruptions at maritime chokepoints (Nature Communications)).

Why a universal owner should care (consequence chain): 1. A single strait disrupts ~20% of oil/LNG or container flow 2. Freight + insurance + energy cost-push 3. Inflation/rates repricing 4. Route diversification capex; friend-shoring 5. Globalization dividend in return assumptions erodes

Blind spot the desk is investigating

Surfaced by the source-gated simulation leg. It carries 0% weight on any published probability — it tells us what to investigate, not what is true.

- Insurance/freight cost-push as a distinct inflation channel — Agents separated war-risk premia + re-routing from the energy shock; this leg persists even when crude round-trips. (investigate: size historical insurance/freight cost-push vs oil in past chokepoint episodes; add to inflation stress test)

- Friend-shoring eroding the globalization dividend in CMAs — Recurring agent theme: low-vol, high-duration repricing of the return premium embedded in long-horizon assumptions. (investigate: quantify globalization-dividend assumption in our return model; sensitivity to friend-shoring)

What it means

For universal owners: Treat correlation-regime risk as a base case, not a tail: the bond hedge and the 60/40 may not cushion the next equity drawdown. For sovereigns & SWFs: Reserve diversification and the erosion of dollar privilege argue for a deliberate currency and gold posture, not drift. For pensions: Demographic gravity (aging, net-seller inflection, low real rates) is the long anchor — funding and contribution policy should assume it.

Explore it yourself: open the Scenario Lab (universalassetowners.com/scenario-lab/) to see any scenario as a live relationship map and put your own questions to the sovereign-wealth allocator, the pension CIO, the reinsurer and the markets desk.

Read the full reasoning behind any number at the Oracle (universalassetowners.com/oracle/) and the live board at the Command Center (universalassetowners.com/command-center/). Probabilities are the desk's analytical estimates, fused from public-source signals through a transparent, explainable model; they are not forecasts of certainty. Editorial scenario analysis for long-duration capital — not investment, actuarial, legal or financial advice.

More from today: listen to The Universal Owner · watch the video briefing · the chart of the day.

Produced and edited by the UAO editorial desk. Editorial analysis for long-duration capital — not investment advice.