Executive Summary

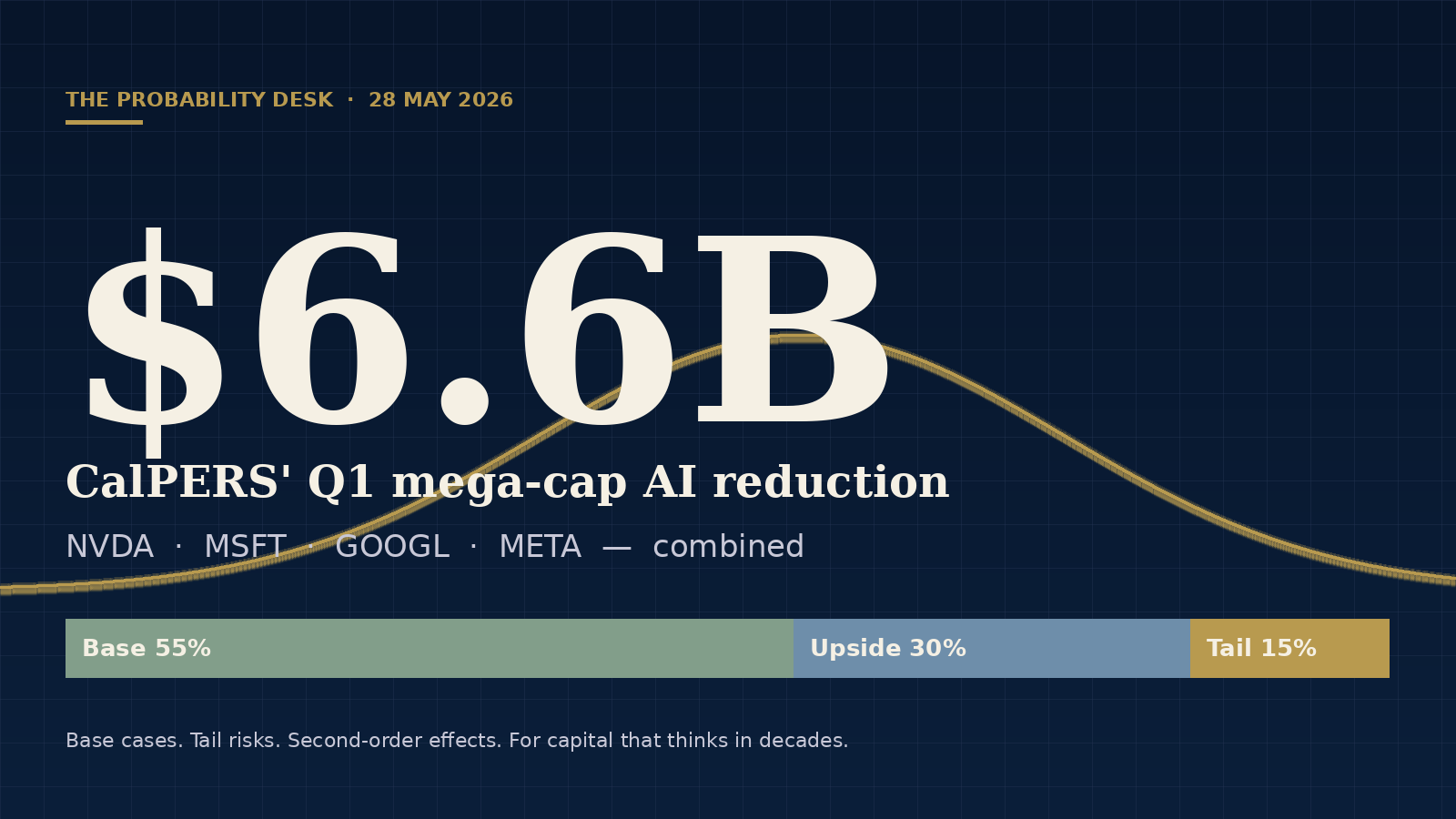

- CalPERS' Q1 2026 Form 13F-HR shows the fund's combined position in NVIDIA, Microsoft, Alphabet (both classes), and Meta declined by $6.59 billion versus end-2025 — a mix of active share reduction and price decline.

- Capital was redirected into semiconductor equipment and memory (Lam Research, Micron, KLA, Intel) and oil majors (Exxon, Chevron, ConocoPhillips) — a pattern directionally consistent with rotating from owners of the AI capex cycle to the enablers of it.

- The Probability Desk assigns a 55% probability that the rotation persists through CalPERS' Q4 2026 filing (mid-February 2027), with a 30% probability the cohort recovers to or above its Q1 2026 level, and a 15% tail probability of accelerated divestment.

- This is one filing, not a trend — but it is one of the larger mega-cap AI reductions in CalPERS' recent disclosure history, against a macro backdrop of Brent crude above $100 and the US 10-year holding near 4.5%.

- For long-duration allocators, the practical question is whether marginal-buyer support for the mega-cap AI cohort is thinning, and what that does to concentration, benchmark, and rebalancing risk over the next two quarters.

The Trigger

CalPERS, the largest US public pension fund at approximately $537 billion in assets, filed its Q1 2026 Form 13F-HR with the Securities and Exchange Commission on 6 May 2026, covering its US equity book as of 31 March 2026. The filing reports 1,064 disclosed positions with $162.5 billion in aggregate reported value. Comparison with the fund's prior 13F (covering 31 December 2025) reveals an unambiguous rotation across the largest names in the portfolio.

The macro context is relevant: Brent crude is trading at $116.73 per barrel, the US 10-year Treasury yield sits at 4.5%, and EUR/USD is at 1.1637 (ECB reference rate, 27 May 2026). Inflation is still expensive to fight, and the long end of the curve is not budging — a regime in which growth-duration assets are structurally disadvantaged relative to cash-flow-rich cyclical and energy names.

What Changed

Four mega-cap AI positions saw their reported value decline by a combined $6.59 billion versus the prior quarter, broken down as follows:

- NVIDIA: −$2.33 billion (−8.04 million shares). Both share reduction and price decline.

- Microsoft: −$2.11 billion (+782,000 shares). Notably, CalPERS added shares while the position value fell — a pure price effect, with the fund holding into a falling tape.

- Alphabet (Class A and Class C combined): −$1.52 billion (−2.78 million shares). Active reduction in both classes.

- Meta Platforms: −$0.63 billion (−209,000 shares). Smaller but directionally consistent.

Other large-cap reductions add another $2.10 billion: Broadcom −$0.60B, Tesla −$0.43B, Berkshire Hathaway B −$0.37B, Salesforce −$0.37B, Eli Lilly −$0.32B.

On the buy side, the redirection is decisive:

- Semiconductor equipment and memory (+$1.32 billion combined): Lam Research +$0.59B (+1.97M shares), Micron Technology +$0.45B (+1.01M shares), KLA +$0.14B, Intel +$0.14B (+1.25M shares).

- Oil majors (+$0.71 billion combined): Exxon Mobil +$0.37B, Chevron +$0.20B, ConocoPhillips +$0.14B.

- Defensive cyclicals: Walmart +$0.13B, Caterpillar +$0.12B.

The filing does not reveal intent, but the position changes are directionally consistent with risk reduction in concentration and growth-duration exposure, paired with a rotation into the picks-and-shovels enablers of the AI capex cycle and into cash-flow-rich names that benefit from sticky inflation. This is an inference from the disclosed data — not a confirmed motive — but the pattern is too coherent to attribute to passive rebalancing alone.

The Probability Call

The Probability Desk assigns a 55% probability that the rotation persists through CalPERS' Q4 2026 filing (mid-February 2027). The resolution criterion is unambiguous: at the next year-end filing, the combined value of CalPERS' positions in NVIDIA, Microsoft, Alphabet (Class A and Class C), and Meta will sit below the Q1 2026 baseline of $30.41 billion (the previous quarter's combined value was approximately $37.0 billion).

Confidence level: medium. Time horizon: nine months. What would move the probability higher: evidence that CalSTRS' Q2 2026 13F (due mid-August) shows a comparable rotation; another disappointing quarter from NVIDIA in late August; aggregate hyperscaler 2027 capex revisions to the downside. What would move the probability lower: a clear Federal Reserve signal toward Q4 2026 cuts; broad-based Q3 earnings beats from the mega-cap AI cohort; meaningful re-acceleration in measured productivity attributable to AI capex.

Q1 2026 Baseline

| Position | Class | Q1 2026 reported value |

|---|---|---|

| NVIDIA | Common | $11.92B |

| Microsoft | Common | $8.11B |

| Alphabet | Capital Stock Class A | $4.21B |

| Alphabet | Capital Stock Class C | $2.96B |

| Meta Platforms | Class A | $3.21B |

| Total | $30.41B |

Q4 2025 combined: approximately $37.0 billion. The $6.59 billion quarter-over-quarter decline captures both active share reductions and the price decline across the cohort.

Model Inputs

The Probability Desk uses a proprietary ensemble methodology combining public filings analysis, macroeconomic data, market-implied signals, expert-prior analysis, base-rate evidence, and narrative-risk simulation. Inputs are weighted based on recency, reliability, liquidity, relevance, and institutional materiality. Signals that do not meet the desk's publication threshold may be monitored as qualitative tripwires but are excluded from the formal probability estimate.

Today's published probability reflects the two input classes that met the desk's inclusion standard for this episode:

- Public filings analysis. CalPERS' Q1 2026 Form 13F-HR was reviewed against the fund's prior-quarter filing and against the disclosed historical sequence of comparable-scale rotations. Position counts, share movements, and reported values were verified line-by-line.

- Expert-prior analysis. Current sell-side consensus on the mega-cap AI cohort, published asset-owner positioning surveys, and the analyst-prior reading of CalPERS' disclosed rotation behaviour back to 2015. The Desk's formal reference-class library is in build; until it is published, this leg is described as analyst prior rather than an audited rate, and the audited episode ledger will be released as soon as it lands.

The following input classes were monitored but excluded from today's formal ensemble because they did not meet the desk's publication threshold:

- Market-implied signals. Prediction-market signals in the relevant cluster (FOMC outcomes, NVIDIA earnings, broad-market levels) were reviewed; no market met the desk's liquidity and reliability threshold for inclusion in the formal probability estimate. The single most relevant market — the near-term FOMC outcome currently pricing essentially zero probability of a June cut — is monitored as a qualitative tripwire only.

- Narrative-risk simulation. Second-order and contagion-pathway signals were monitored but did not meet today's publication threshold; they are treated qualitatively rather than incorporated as a formal ensemble input.

- Macroeconomic and rate environment. Brent above $100, the US 10-year holding near 4.5%, and a stable euro-dollar provide directional context. They are not incorporated as independent inputs to today's estimate; they shape the regime in which the base-rate evidence is interpreted.

Scenario Tree

Scenario A — Controlled Rotation (Base) Probability: 55% CalPERS continues the rotation at a slower pace while the mega-cap AI cohort also re-prices modestly downward. Combined cohort value ends Q4 2026 in the $23–28 billion range. Resolves YES. Key drivers: NVIDIA prints another underwhelming quarter; the Fed remains on hold through Q3; oil holds above $100; sell-side consensus on the cohort gradually revises lower. Asset-owner implication: Marginal-buyer support for the cohort thins. Concentration risk for benchmark-tied allocators rises. Rebalancing discipline becomes the practical question for investment committees.

Scenario B — Re-Add (Upside) Probability: 30% Earnings beats across the mega-cap cohort plus a Federal Reserve pivot pull positions back to benchmark weight. Combined cohort value recovers to $31–38 billion. Resolves NO. Key drivers: Fed cuts in Q4 2026; NVIDIA and Microsoft beat Q3 earnings; index-overlay rebalancing pulls weight back to neutral; productivity data re-accelerates. Asset-owner implication: The rotation reads as a one-off rebalance rather than a regime change. The question is deferred for at least one more quarter, and the case for sustained AI concentration remains intact.

Scenario C — Accelerated Divestment (Tail) Probability: 15% Recession confirmation or a material AI-capex disappointment triggers a faster reduction across the cohort. Combined cohort value drops below $20 billion. Resolves YES at a much larger magnitude. Key drivers: Q3 NIPA confirms contraction; or aggregate hyperscaler 2027 capex guides down materially; or a Google antitrust ruling materially impairs the cohort; or a credit event re-prices growth-duration assets broadly. Asset-owner implication: This is the genuinely uncomfortable scenario for benchmark-tied long-duration capital — a left-tail outcome in which AI concentration becomes the primary driver of portfolio drawdown rather than a source of return. Private-market AI marks would follow on a lag, amplifying the read-through.

Weights sum to 100% and round to nearest 5%.

Tripwires

Indicators the Probability Desk monitors and that would update the published estimate:

- CalSTRS Q2 2026 13F-HR (due mid-August). A comparable rotation in California's other large public pension would confirm the signal extends beyond CalPERS-specific behaviour and would lift the base case toward 60%.

- NVIDIA Q2 2026 earnings (late August). Another miss versus whisper raises the base case and reduces the upside.

- Hyperscaler 2027 capex guides (Q3 earnings cycle, late October). Aggregate Microsoft + Alphabet + Amazon + Meta capex revision of ≥10% lower versus current consensus would lift the tail-leg weight by approximately 5 percentage points.

- Federal Reserve communication. A clear pivot toward Q4 2026 cuts would shift weight toward the upside scenario.

- Brent crude sustainably below $90. Would remove the inflation tailwind for the oil-major leg of the rotation and weaken the broader thesis.

- Credit-spread movement. Meaningful widening in investment-grade or high-yield spreads would increase the tail-leg weight.

- Private-market AI valuations. Material markdowns reported by large private-market managers in their Q2 disclosures would amplify the rotation signal and raise the tail.

- Geopolitical escalation in any major chokepoint or sanction regime. Would tighten the inflation-rate-energy regime and reinforce the base case.

Asset Owner Implications

The most consequential question this filing raises is not whether AI remains a transformative investment theme. It does. The question is whether marginal-buyer support for the mega-cap cohort is thinning, and what that does to portfolio risk across the universal-owner constituency.

Sovereign wealth funds. At policy-portfolio weight, the mega-cap AI cohort is roughly 30% of the S&P 500 and a meaningful share of any global-equity sleeve. Passive overlays do not move on a single 13F. The relevant question is whether the active sleeve underneath those overlays should be reviewed against the same concentration metrics that CalPERS appears to be applying. For funds with explicit concentration limits, this is procurement-grade material for the next investment-committee review.

Public pensions. The benchmark-relative concentration risk is structural and well-known. Public pensions with formal allocation policies face an awkward governance question: if the cohort underperforms materially in Q4 or Q1 2027, the funded-ratio impact is meaningful, and the optics of being long the cohort into a known peer rotation is a board-level conversation. CalPERS' own behaviour is now the relevant precedent.

Endowments and foundations. Longer time horizons and lower benchmark sensitivity make the AI concentration more a question of portfolio resilience than tracking error. The relevant framing for investment committees is whether the cohort's role in the portfolio has shifted from "growth-engine alpha" to "concentrated beta with embedded liquidity risk."

Insurers. Investment-grade balance sheets with strict diversification rules already cap individual-issuer exposure. The relevant implication is downstream. Private-market AI infrastructure debt and equity carry the same cohort sensitivity, and if mega-cap AI re-prices materially, marks in private credit and private equity will follow on a lag. The asset-liability matching question intensifies under the tail scenario.

Family offices. The greatest flexibility, the greatest discretion. The relevant question is whether to continue paying multiple expansion in a cohort the largest US public pension has actively reduced — or to rotate into the same picks-and-shovels names CalPERS just bought.

Long-duration allocators broadly. When the largest holders reduce, marginal demand support thins. When concentration risk is structurally high and active sellers emerge, the asymmetry of holding through a re-pricing becomes uncomfortable. The Probability Desk's view is not that the AI theme is broken — it is that the conditions under which the theme is held are evolving, and that the universal-owner constituency should be examining those conditions actively rather than passively.

Bottom Line

AI remains a transformative investment theme. That is not what this filing changes.

What it changes is the read on whether the largest long-duration capital owners are beginning to separate their long-term belief in the theme from their near-term tolerance for the concentration, valuation, and liquidity risk that comes with it. CalPERS is one fund. CalSTRS reports in three months. The signal is not yet a trend — but it is no longer noise.

The Probability Desk's working estimate is that the rotation persists. We will revise on the next filing.

Editorial scenario analysis only. Not investment, actuarial, or geopolitical advice. Probabilities are the Probability Desk's, weighted across the input classes that met today's inclusion standards. Methodology available on request.