Volume 1, Issue 16. Monday, May 25, 2026. Sent 7:00 am ET / 14:00 GST.

The asset that is supposed to be the calm centre of a long-horizon portfolio had its loudest week in years. With US markets shut for Memorial Day, the action this morning is in Asia and Europe — and it is in the long end of the government-bond market, where 30-year yields touched levels not seen in 15 to 28 years, and in Japan a record. The trigger is a Middle East oil shock that has rekindled inflation; the deeper worry is fiscal. Four things for owners of long-horizon capital: the global long-bond repricing, Europe's growth downgrade that names the shock, an emerging-market central bank moving to defend its currency, and the structural power demand sitting underneath the cyclical energy story.

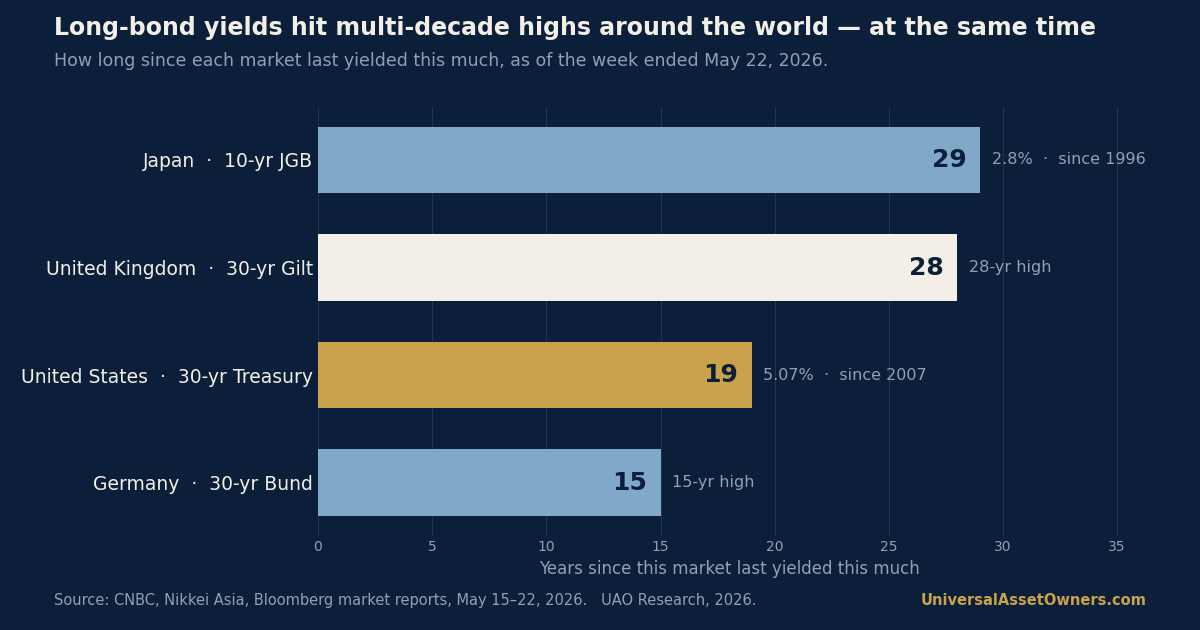

1. The world repriced the long bond — and the records landed simultaneously.

The long end of the developed-market government-bond curve set multi-decade highs across four major issuers at once. The US 30-year Treasury yield reached 5.07% on May 22 — a level it had not seen since 2007 — after the 10-year jumped roughly 12 basis points to 4.6% the prior week, its biggest weekly move since the April 2025 tariff shock. Japan's 30-year yield hit a record near 4.2% intraday before easing to about 4.01%, while the 10-year JGB touched 2.8%, its highest since 1996. Germany's 30-year Bund reached a 15-year high and the UK's 30-year Gilt a 28-year high. Source: CNBC, May 22, 2026.

The proximate cause is an oil price shock tied to the Middle East conflict and uncertainty over the Strait of Hormuz, which has revived inflation fears and pushed the market toward a consensus that the Federal Reserve will not cut at its next meeting. But the more durable driver is the term premium — the extra yield investors demand to hold long debt — rising as supply mounts. The OECD's Global Debt Report 2026, a primary source, projects OECD gross sovereign borrowing of around $18 trillion in 2026 against an outstanding stock that already reached a record $61 trillion, with maturities shortening and refinancing risk building. Source: OECD Global Debt Report 2026, March 2026.

For a universal owner the read-across is uncomfortable. The long government bond is the asset most balanced and liability-driven portfolios lean on to offset equity risk. When it sells off alongside equities on an inflation scare, the hedge is firing in reverse — and it is doing so just as the world asks markets to absorb record new issuance.

Source: CNBC / OECD, May 2026. | Coverage: feeds the Risk Radar duration theme, this week.

2. Europe names the shock: growth cut to 0.9%, inflation lifted to 3%.

The European Commission's Spring 2026 Economic Forecast, released May 21, cut eurozone GDP growth to 0.9% for 2026 — down from the 1.4% recorded in 2025 — and raised expected 2026 inflation to 3%, well above the 1.9% it projected six months ago. The Commission attributed the revision squarely to the energy shock stemming from the Middle East conflict, and warned the impact would persist into 2027. Germany was marked down to 0.6% growth, France to 0.8%, Italy to 0.5%. Source: European Commission, Spring 2026 Economic Forecast, May 21, 2026.

This is the macro logic underneath the bond move stated in an official document: an energy-driven inflation impulse that slows growth while lifting prices — the uncomfortable combination that keeps central banks on hold and term premia elevated. For an owner with European exposure, it sharpens the question of whether the region's disinflation story has been interrupted or reversed.

Source: European Commission, May 21, 2026.

3. The emerging-market defense begins: Bank Indonesia hikes 50bp to shield the rupiah.

Bank Indonesia surprised markets on May 20 with a 50-basis-point increase in its policy rate to 5.25% — its first hike since April 2024 and double the 25bp the market expected — explicitly to stabilise a rupiah that had slid to a record low near 17,600 per dollar. The deposit and lending facility rates rose in step, to 4.25% and 6%. Source: Bank Indonesia, May 20, 2026.

This is the other side of the developed-market story. When long yields in the US and Europe rise and oil climbs, capital pulls toward the core and emerging-market currencies come under pressure; the central-bank response is to raise rates into a slowdown. For owners holding emerging-market local-currency debt or unhedged EM equity, the episode is a reminder that the same global shock that repriced Treasuries is now setting the cost of capital in Jakarta. Source: Bloomberg, May 20, 2026.

Source: Bank Indonesia, May 20, 2026.

4. Under the cyclical oil shock sits a structural one: AI's power demand.

The week's inflation scare is cyclical — an oil shock that may pass. The electricity story underneath it is not. The US Department of Energy opened a roughly $1.9 billion funding round to upgrade the power grid, with full applications due May 20 and selections expected in August, as data-centre load is projected to roughly double to about 8% of US electricity by 2030 against a capacity shortfall already exceeding 11 gigawatts and seen widening past 45 GW by 2028. Source: US Department of Energy, May 2026.

For long-horizon owners this is migrating from a thematic equity view to a direct allocation. House research from infrastructure managers — Apollo and Morgan Stanley among them, and these are house views, not neutral findings — frames grid, transmission, and generation as a multi-decade capital-formation need that institutional portfolios are increasingly funding through unlisted infrastructure rather than public equity. The energy line in the long-horizon portfolio is becoming less about commodities and more about wires and turbines. Source: Apollo, Infrastructure Outlook 2026.

Source: US Department of Energy / Apollo, May 2026.

— Chart of the day —

Long government-bond yields hit multi-decade highs around the world — at the same time.

Source: CNBC, Nikkei Asia, Bloomberg market reports, May 15–22, 2026. UAO Research, 2026.

— Take of the day —

"For a generation the long government bond was the universal owner's shock absorber — the asset that rallied when everything else fell. A world where 30-year yields set multi-decade records on an oil shock, while issuance hits records, is a world where that hedge can fire in reverse. The anchor is not broken, but it is no longer free: owners who treated duration as ballast now have to price it as a position."

— UAO Research.

— Three links worth your time —

- OECD — Global Debt Report 2026: Sovereign borrowing outlook. The primary source on record issuance, shortening maturities, and why the market's capacity to absorb debt is the real story behind the term premium.

- European Commission — Spring 2026 Economic Forecast. Official confirmation that the energy shock is a growth-down, inflation-up event for Europe — read it as the macro backdrop to the bond move.

- Bank of Canada — The rise in the Canadian term premium in a global context. A central-bank research note showing the term-premium rise is a global phenomenon, with correlations near 0.92 across advanced economies — the analytical frame for this week.

Presented by [Quarterly Sponsor].

This edition of the UAO Daily Brief is seeking a founding quarterly sponsor. If your firm reaches institutional allocators, the team is at sponsors@universalassetowners.com.

UAO Daily Brief is the morning briefing for the people who allocate long-horizon capital. Five minutes, five days a week.

Become a Premium subscriber · Listen: The Allocator Briefing · Forward to a colleague · Manage preferences

UniversalAssetOwners.com. Capital at the scale of the world.

Continue the briefing. Read the daily brief · watch the daily video briefing · listen to The Allocator Briefing · view the chart of the day.

Produced with the UAO Content Engine. AI-assisted; editorially reviewed before release. Not investment advice.