Volume 1, Issue 15. Friday, May 22, 2026. Sent 7:00 am ET / 14:00 GST.

The warning became a number this week. Fitch put the US private-credit default rate at a record 6% — and more than half of it was the kind of stress that hides in deferred and paid-in-kind interest rather than a missed payment. Underneath that, the official sector quietly moved private credit from the ninth-ranked risk to the fourth in six months, the world's largest index managers split apart the stewardship machinery that votes a universal owner's shares, four companies grew to 4% of the investment-grade bond market, and Norway paused ethical divestment because a handful of US tech names now carry its fund. Five items, one chart, one take — the Risk Radar edition.

1. The private-credit warning became a number: defaults hit a record 6%.

Fitch's US private-credit default rate reached 6.0% for the twelve months to April 30, a record since the firm began tracking the market in August 2024. The composition is the story. Of 99 default events, 81 were first-time defaulters — the most on record — and more than half of the defaults came through interest deferrals and payment-in-kind, the mechanism that lets a borrower pay interest in more debt rather than cash. Consumer-products borrowers defaulted at 11.1%, up from 5.9% a year earlier. Source: Bloomberg Law, May 21, 2026.

For a universal owner the number matters less than its texture. A default rate of 6% is uncomfortable but not, on its own, a crisis. A default rate where most of the stress is being capitalised into PIK — added to the loan balance rather than recognised as a loss — is a market that is choosing to defer its reckoning. It is the difference between a market that has marked its problems and one that has postponed them.

This lands on top of an official-sector warning. The Financial Stability Board in early May flagged private credit's leverage, complexity and interconnectedness as a financial-stability vulnerability, and noted that data gaps make the exposures hard to see. The asset class that every large allocator added in the cheap-money decade is now having its first real test — and the test is arriving through the slow channel, not the fast one. Source: Financial Stability Board, May 6, 2026.

Source: Bloomberg Law / Fitch Ratings, May 21, 2026. | Coverage: The Universal Owner Risk Radar, this week.

2. The great unbundling of stewardship: the Big Three are splitting the vote.

Going into the 2026 proxy season, the three managers that vote more shares than anyone on earth have each pulled their stewardship operations apart. BlackRock now runs a separate Investment Stewardship team for its index book and an Active Investment Stewardship team for its active strategies. State Street has split a core Asset Stewardship Team from a new Sustainability Stewardship Service for clients who want climate, nature, human-rights and diversity weighed explicitly. Vanguard is dividing its stewardship into two teams this year. Alongside them, ISS has shifted to judging climate and emissions proposals case-by-case rather than with a standing recommendation, and JPMorgan has dropped proxy-advisor recommendations in favour of an internal, AI-assisted voting platform. Source: Harvard Law School Forum on Corporate Governance, April 1, 2026.

The mechanism a universal owner relied on — delegate the index book, let the manager's house policy carry the vote — is being deliberately decentralised. Voting outcomes are becoming less predictable and more contextual, which cuts both ways: an asset owner that wants its capital voted a particular way can no longer assume the manager will, and increasingly has the option, through pass-through voting, to vote the book itself. The lever is still there. It is just no longer automatic.

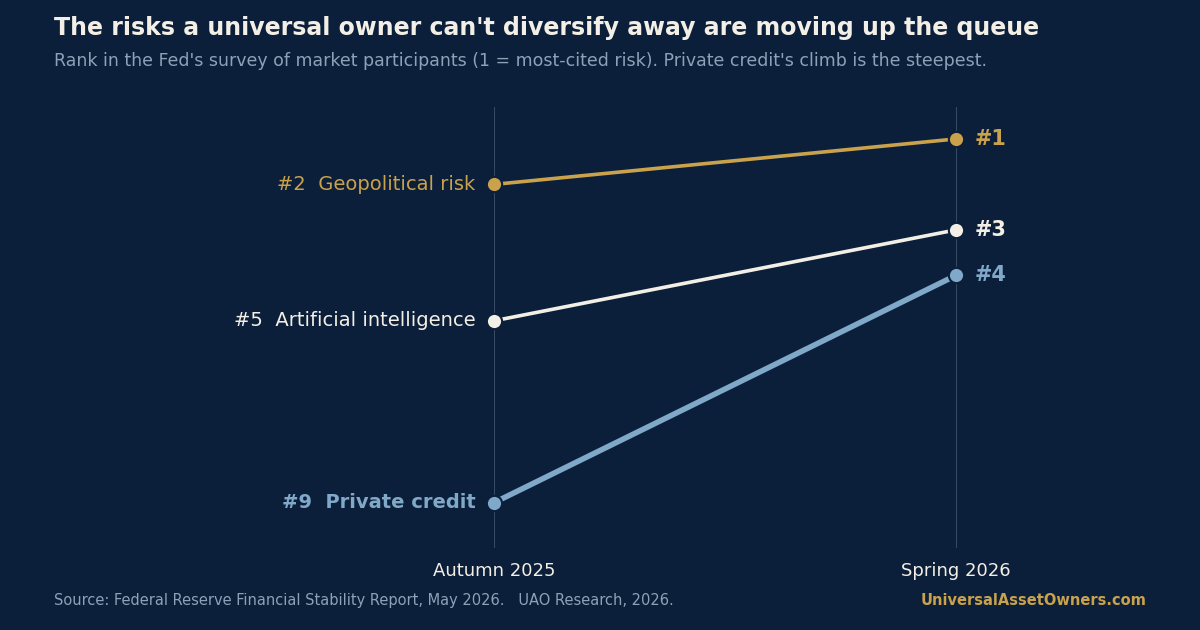

3. The official sector reshuffled its fears: geopolitics first, AI third, private credit up to fourth.

The Federal Reserve's May Financial Stability Report carried its semi-annual survey of market participants, and the ordering moved. Geopolitical risk took the top spot, up a notch from the autumn. AI rose to third from fifth. Private credit jumped to fourth from ninth — the sharpest climb in the survey and the official-sector echo of this week's default print. The report's severe stress scenario models a 58% fall in equity prices. Source: Federal Reserve Financial Stability Report, May 8, 2026.

The pattern is what a universal owner should notice. The risks moving up the list — geopolitics, AI, private credit — are precisely the ones a globally diversified, long-horizon owner cannot trade around. They are system risks, not security-selection risks. When the people who run other people's risk start agreeing on that, the question stops being "which assets" and becomes "which exposures can we actually shape."

Source: Federal Reserve, May 8, 2026.

4. Four companies now hold 4% of the investment-grade bond market.

The combined weight of Meta, Alphabet, Amazon and Oracle in the Bloomberg US Corporate Investment-Grade index nearly doubled in the year to April 1, from 2.2% to 4.1%, as the hyperscalers turned to debt to fund an AI build-out heading toward roughly $600bn of capital spending this year. Source: Breckinridge Capital Advisors, 2026.

For an owner who holds the whole market, this is one position wearing two costumes. The same names that dominate the equity index are now a fast-growing slice of the supposedly diversifying core of the bond portfolio. A correction in AI-infrastructure economics would not be a tech-equity event quarantined on one side of the balance sheet; it would arrive in credit and equity at once. The diversification a 60/40 owner assumes between the two is quietly thinning.

5. Norway pauses ethical divestment as a few US tech names carry the fund.

Norway's $2.2tn fund has suspended its ethical-divestment process while a government commission reviews the rules that made it a global benchmark for exclusion. Finance minister Stoltenberg framed the pause around a hard fact: the fund finances roughly a quarter of Norway's public spending, and a significant part of its value now rests on a handful of US tech giants — Nvidia, Meta, Amazon among them. Source: Reuters via U.S. News, May 12, 2026.

The collision is instructive. Exclusion is the universal owner's bluntest lever, and it works best on the margins of a portfolio. When the names that drive your returns are also the names most likely to attract an ethical or concentration objection, the lever starts to pull against the mandate. Norway's pause is not a retreat from values; it is an admission that exclusion and concentration are now arguing with each other on the same balance sheet. Source: Norges Bank Investment Management, 2026.

— Chart of the day —

In six months, private credit jumped from the ninth-ranked risk to the fourth.

Source: Federal Reserve Financial Stability Report, May 2026. UAO Research, 2026.

— Take of the day —

"A 6% default rate is not the problem; a 6% default rate where most of the stress is being capitalised into PIK is. Private credit's first real test is arriving through the slow channel — deferred interest, marks that lag — which is exactly how an asset class postpones a reckoning rather than recognising one. The universal owner's edge here is patience, but only if it can see what it owns; the FSB's point about data gaps is the real warning."

— UAO Research.

— Three links worth your time —

- Financial Stability Board — Report on Vulnerabilities in Private Credit. The primary document behind the week's lead — read it for the data-gap argument, not just the headline risk.

- ESG Today — bp Shareholders Defeat Resolution Aimed at Reducing Climate Disclosures. A 47% vote to roll back climate disclosure, in a season where outcomes are suddenly hard to call — the stewardship story made concrete.

- Harvard Law School Forum on Corporate Governance — 2026 Proxy Season Preview. The clearest map of how voting and stewardship were rewired for this season.

Presented by [Quarterly Sponsor].

This slot is open for a founding quarterly partner. UAO reaches the CIOs, deputy CIOs and investment teams of the world's largest asset owners. The team is at sponsors@universalassetowners.com.

UAO Daily Brief is the morning briefing for the people who allocate long-horizon capital. Five minutes, five days a week.

Become a Premium subscriber · Listen: The Allocator Briefing · Forward to a colleague · Manage preferences

UniversalAssetOwners.com. Capital at the scale of the world.

Continue the briefing. Daily brief · Chart of the day · The Allocator Briefing.

Produced with editorial automation by the UAO Content Engine.