Volume 1, Issue 14. Thursday, May 21, 2026. Sent 7:00 am ET / 14:00 GST.

The marginal buyer of US assets is no longer a government. Monday's Treasury data showed foreign official institutions were net sellers of US securities in March while private foreign investors bought on a scale that more than covered them — the clearest single-month picture yet of a structural change in who funds the United States. Underneath it, China's Treasury holdings fell to a 17-year low and Japan's slipped again, while the reserves that left bought gold: central banks added 244 tonnes in the first quarter. Meanwhile sovereign funds kept routing surplus capital into AI and digital infrastructure, and Norway's $2.2 trillion fund was challenged on whether its climate votes match its words. Five items, one chart, one take.

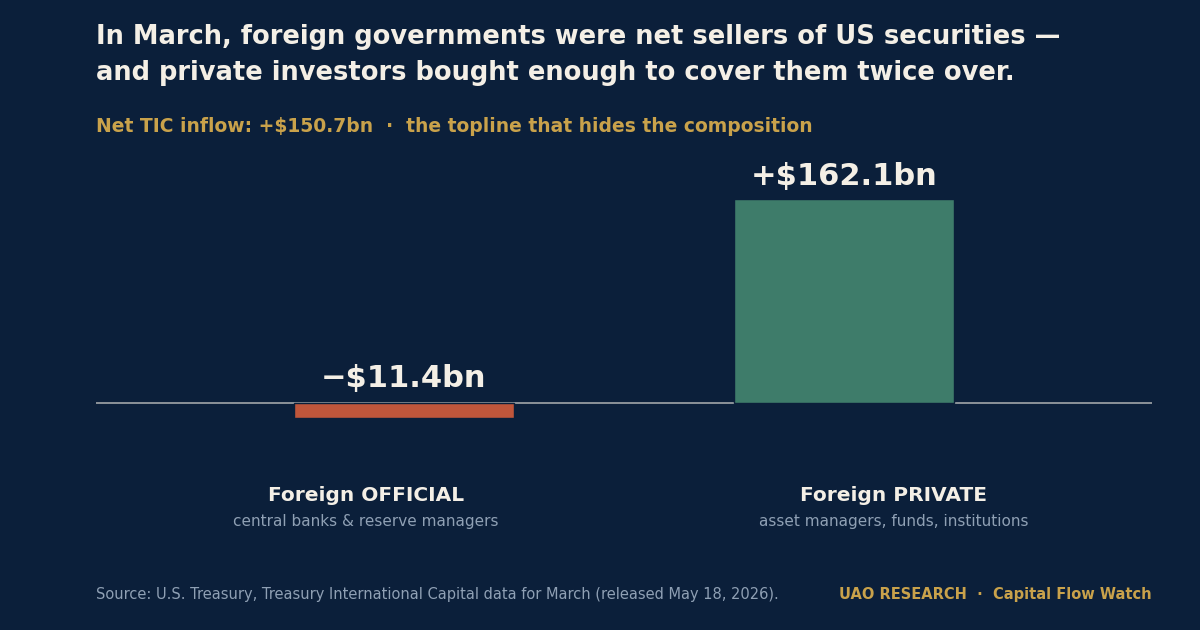

1. The official sector is quietly selling US Treasuries — and private money is filling the gap.

The headline number from the March Treasury International Capital report, released Monday, was a healthy net inflow of $150.7 billion. The composition is the story. Net foreign official flows were negative — a $11.4 billion outflow, including $14.9 billion of net official sales of long-term US securities — while net foreign private inflows ran to $162.1 billion. Governments and reserve managers stepped back; private institutions stepped in with room to spare. Source: U.S. Treasury TIC data for March, May 18, 2026.

For a universal owner this is the question that sits underneath every dollar-asset allocation: who is the price-setter at the margin? When the official sector — historically the patient, price-insensitive holder — becomes a net seller, the marginal buyer is a return-seeking private institution that can leave. That changes the risk character of the world's deepest market without changing its size.

The reassurance is that the gap was filled, and easily. The unease is what it implies about the future: a Treasury market increasingly funded by investors who hold it for yield rather than for reserves.

Source: U.S. Treasury, May 18, 2026. | Coverage: Capital Flow Watch, this week.

2. China's Treasury stack hits a 17-year low; the UK custody hub absorbs the difference.

Total foreign-held Treasuries fell 1.5% in March to $9.348 trillion, down from a record $9.487 trillion in February. The decline was concentrated: China's holdings dropped about 6% to $652.3 billion — the lowest since September 2008 — and Japan, still the largest foreign creditor, slipped roughly 4% to $1.192 trillion. The United Kingdom moved the other way, up 3.3% to $926.9 billion. Source: Prism News, May 19, 2026.

Read the UK figure with care. London is a custody hub, so its position is usually read as a window into global hedge-fund and institutional positioning rather than a national tally — which reinforces Item 1's point: the demand that is growing is private and mobile, not official.

The China line is the geopolitical one. A holding at levels last seen in the year of the Lehman collapse is a slow, deliberate reallocation, not a market accident. For an owner of dollar assets, the signal is not a crash; it is a steady erosion of the official bid.

Source: U.S. Treasury TIC, Major Foreign Holders (Table 5), May 18, 2026.

3. Where reserves go when they leave Treasuries: 244 tonnes of gold in a quarter.

The World Gold Council reports central banks bought a net 244 tonnes of gold in the first quarter of 2026 — up 3% year on year and above the five-year average. Poland was the largest buyer, adding 31 tonnes to reach 582; Uzbekistan added 25 tonnes; the People's Bank of China added 7 tonnes, lifting its reserves to 2,313 tonnes, now about 9% of the total. Source: World Gold Council, Gold Demand Trends Q1 2026, May 2026.

This is the other side of Item 1's ledger. The official money trimming dollar exposure is not, on the whole, moving into another sovereign's debt — it is buying bullion, an asset no government can freeze or sanction. OMFIF's reserve-manager survey reports that roughly a third of central banks expect to add gold in the short term. Source: OMFIF, Global Public Investor 2026.

A universal owner does not run a reserve book, but the behaviour matters: the institutions that set the terms of the global system are pricing political risk into their reserve composition, and that filters into the real rate on the asset everyone else benchmarks against.

Source: World Gold Council, May 2026.

4. Sovereign funds are routing the world's surplus capital into AI and digital infrastructure.

The deployment side of the same flows is concentrated and growing. Sovereign wealth funds, with combined assets above $12 trillion, lifted private-markets allocations to roughly 29% at the end of 2025 from 25% in 2020 — a shift supercharged by data centres, fibre and the power assets behind AI. Sovereign deal value rose even as pension deal activity slowed. Source: S&P Global Market Intelligence, Jan 2026.

GIC, ADIA, Mubadala and PIF have each built sizeable positions in digital infrastructure, both as direct owners and as co-investors alongside the large alternatives platforms. Source: EY, 2026. The point for the universal owner is that the surplus capital leaving low-yield reserve assets and the surplus capital chasing the AI build-out are, increasingly, the same pools — which makes concentration in a handful of compute and energy assets a flow risk as much as a thematic one.

5. Norway's $2.2tn fund is challenged on whether its climate votes match its words.

A Norwegian environmental group argues that Norges Bank Investment Management — which expects roughly 7,200 portfolio companies to align with a net-zero-by-2050 pathway — is falling short where it counts most: board accountability at fossil-fuel companies expanding production. NBIM rejects the framing, noting that voting is one tool alongside extensive bilateral engagement, and has just published Nature Expectations setting out what it wants companies to disclose on ecosystem risk. Source: Reuters via MarketScreener, May 5, 2026.

The universal owner has two levers: where the capital goes, and how the votes are cast. Items 1–4 are about the first. This is about the second — and the scrutiny is a reminder that for an owner of the whole market, stewardship is not a side activity but the part of the mandate that addresses risks allocation alone cannot diversify away. Source: Norges Bank Investment Management, Responsible Investment, 2026.

— Chart of the day —

In March, foreign governments were net sellers of US securities — and private investors bought enough to cover them twice over.

Source: U.S. Treasury, Treasury International Capital data for March (released May 18, 2026). UAO Research, 2026.

— Take of the day —

"The size of the US Treasury market is not in question; the character of its demand is. As official holders trim and private institutions become the marginal buyer, the world's safe asset is increasingly funded by capital that holds it for return rather than for reserves. That does not break anything today — there is, as GIC and Temasek both note, no market deep enough to replace it — but it means the deepest market on earth now rests on the most mobile money. Universal owners should treat that as a slow change in the risk of their largest, most passive holding, not a headline to trade."

— UAO Research.

— Three links worth your time —

- IMF — Global Financial Stability Report, April 2026, Chapter 2: Capital Flows to Emerging Markets. The primary-research backbone of today's deep-dive: nonbanks now provide ~80% of emerging-market portfolio debt, and those flows are more risk-sensitive than what they replaced.

- Top1000funds — Limited alternatives keep global capital anchored to the US. GIC's and Temasek's leaders on why "fraying" US exceptionalism still has no credible substitute — the absorption-capacity argument, from the allocators who live it.

- World Gold Council — Gold Demand Trends, Q1 2026. The cleanest read on where official reserve diversification is actually going, by buyer and tonnage.

Presented by [Quarterly Sponsor].

This space is reserved for UAO's founding quarterly sponsor. To reach the people who allocate long-horizon capital, the team is at sponsors@universalassetowners.com.

UAO Daily Brief is the morning briefing for the people who allocate long-horizon capital. Five minutes, five days a week.

Become a Premium subscriber · Listen: The Allocator Briefing · Forward to a colleague · Manage preferences

UniversalAssetOwners.com. Capital at the scale of the world.