Volume 1, Issue 13. Wednesday, May 20, 2026. Sent 7:00 am ET / 14:00 GST.

The cracks in private credit got real this month, and the institutions most exposed are still buying. Semi-liquid funds run by Blue Owl and Blackstone have hit their redemption limits, the US private-credit default rate has touched a record, and the Financial Stability Board has put the $1.5–2 trillion market on its watchlist — while CalPERS, Dutch giant APG and the UK's Nest keep adding. At the same time CalPERS is about to retire strategic asset allocation altogether, US corporate pensions are the best-funded since 2007, and Mubadala bought into the world's largest offshore wind farm beside two pension giants. Five items, one chart, one take.

1. Private credit hits its first real liquidity test — and the pensions that own it keep buying.

The withdrawal queue arrived first. Across the major semi-liquid private-credit funds, redemption requests roughly doubled quarter-on-quarter in early 2026, reaching an estimated 10–14 percent of net asset value against quarterly caps of around 5 percent. Blue Owl moved to permanently restrict redemptions on several vehicles; Blackstone's $82 billion BCRED — the largest private-debt fund in the world — drew a record $3.8 billion in requests and injected roughly $400 million of firm and employee capital to meet them. Fitch put the US private-credit default rate at a record 9.2 percent for 2025.

None of this has slowed the buyers. CalPERS has endorsed lifting its private-markets target toward 40 percent from 33; APG, Europe's largest pension investor, is pushing private markets above 30 percent of assets and treating the volatility as an entry point; the UK's state-backed Nest has committed £450 million to US private credit. The logic is real — long-dated liabilities can harvest an illiquidity premium public markets do not pay — but it is being tested in public for the first time.

The universal-owner read: this is a liability-matching bet meeting a liquidity event. The question is no longer whether the premium exists, but whether the redemption terms, valuation marks and sector concentration you underwrote survive a year in which defaults rise and the gates actually close.

Source: CNBC, 8 May 2026. · FSB, 6 May 2026. · Congressional Research Service, 27 Mar 2026. | Coverage: Pension Strategy Watch, this week.

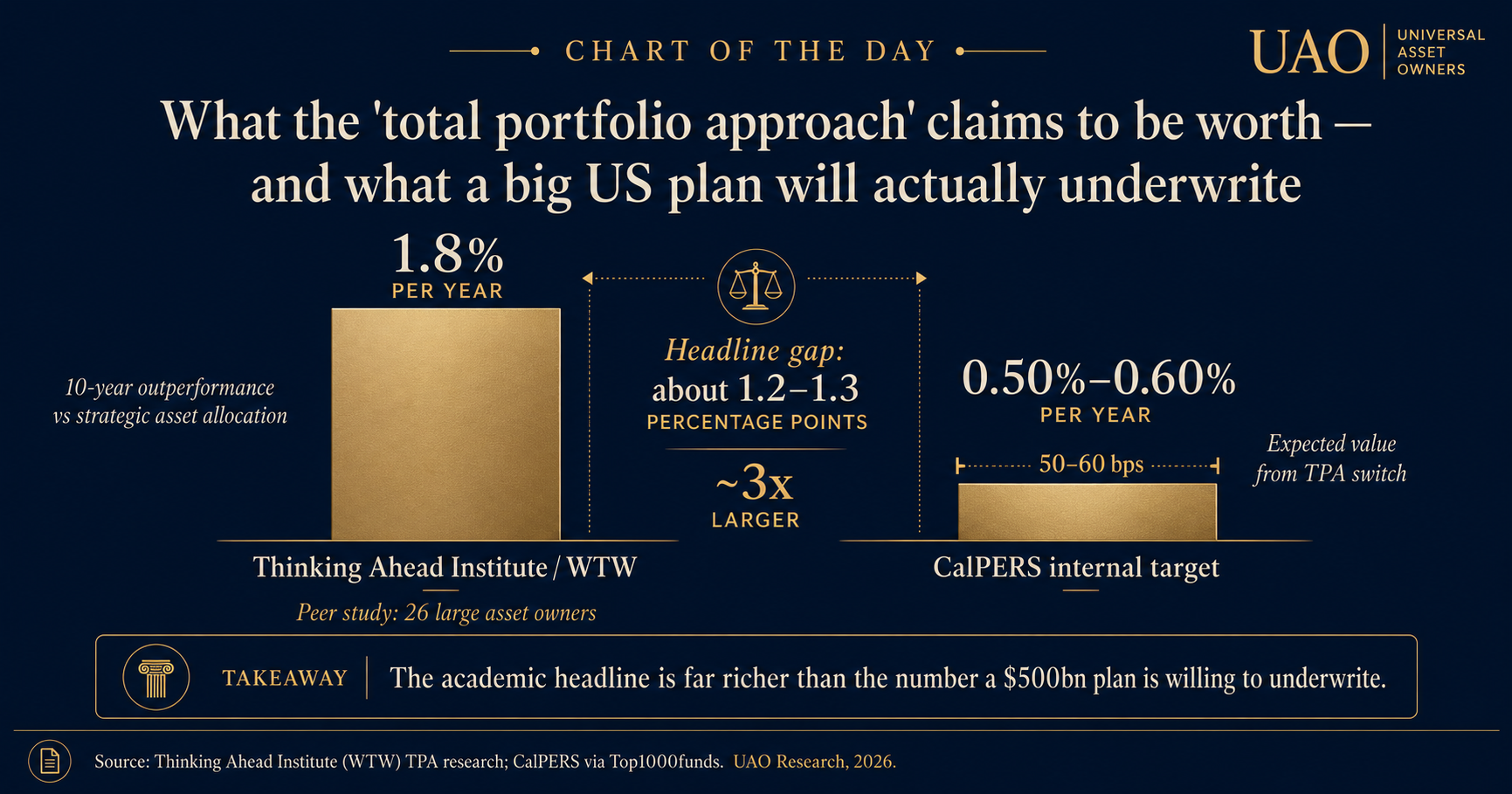

2. CalPERS retires strategic asset allocation — the largest US public pension goes "total portfolio" on July 1.

From 1 July 2026, the $500-billion-plus California Public Employees' Retirement System replaces the 11 asset-class benchmarks it has used for decades with a single reference portfolio — 75 percent equities, 25 percent bonds — and a 400-basis-point active-risk limit. Performance will be judged against that one number rather than against asset-class targets. The discount rate stays at 6.8 percent.

It is the first formal adoption of the total portfolio approach by a US public pension, importing an operating model long run by CPP Investments and Australia's Future Fund. CalSTRS, the $390 billion teachers' fund, is converging on the same idea through its "one-fund" model. CalPERS expects the switch to add 50–60 basis points a year; the deeper change is who decides what the fund owns, and against what yardstick.

Source: CalPERS, 2025. · Top1000funds, Dec 2025. | Coverage: today's deep-dive.

3. US corporate pensions are the healthiest since 2007 — which makes "what now" the harder question.

The Milliman 100 corporate defined-benefit funded ratio reached 107.8 percent at the end of April 2026, the highest since October 2007. Plan assets rose about $20 billion on a 2.13 percent monthly investment return, to roughly $1.297 trillion, while liabilities fell as discount rates ticked up. Twelve months earlier the ratio was 102.2 percent.

Surplus is a nicer problem than deficit, but it is still a decision. A fully funded corporate plan has to choose between locking in the win — de-risking into long-duration bonds and, increasingly, an insurer buy-out — and keeping return-seeking assets on to grow the surplus. For the OCIOs and insurers on the other side of that trade, the pension-risk-transfer pipeline just got deeper.

Source: Milliman Pension Funding Index, May 2026.

4. Mubadala buys into the world's largest offshore wind farm — beside two pension giants.

Mubadala committed $325 million to Ørsted's Hornsea 3, the 2.9-gigawatt project off the Norfolk coast that will power more than 3.3 million UK homes, investing through the Apollo-led consortium that also includes the UK's Universities Superannuation Scheme and Québec's La Caisse (CDPQ). Apollo-managed funds hold 50 percent of the joint venture; Ørsted retains the other half and continues to build and operate.

The structure is the signal. A Gulf sovereign and two of the world's larger pensions are co-underwriting core energy-transition infrastructure as the developer sells down equity to fund construction — exactly the capital-recycling model that lets utilities build at scale and lets long-horizon owners buy de-risked, contracted cash flows. Expect more sell-downs like it.

Source: Mubadala, May 2026. · The National, 12 May 2026.

5. CalPERS's private-equity book went from $60bn to ~$100bn in three years — what "doubling down" looks like.

In just over three years CalPERS scaled its private-equity program from about $60 billion to nearly $100 billion, citing a 14 percent one-year return and a funded ratio that climbed from the low-70s to the low-80s. It is the clearest primary-document picture of why pensions keep adding illiquidity even as Item 1's cracks widen: the program is credited with real contribution to the plan's recovery.

The caution travels with the number. A book built fast in a higher-rate, slower-distribution environment carries pacing and liquidity risk, and several US systems — Ohio, Oregon, Texas, Nevada among them — have trimmed PE targets even as CalPERS leans in. The dispersion between funds is now the story.

Source: CalPERS board materials, Jan 2026. · Markets Group, 2026.

— Chart of the day —

What the "total portfolio approach" claims to be worth — and what a big US plan will actually underwrite.

Source: Thinking Ahead Institute (WTW) TPA research; CalPERS via Top1000funds. UAO Research, 2026.

— Take of the day —

"Private credit's defenders and its regulators are both right, which is the problem. Pensions are structurally the natural owners of illiquid credit — and they are adding into the first quarter where the gates actually closed and defaults hit a record. The discipline that matters now is not the allocation decision; it is the redemption term, the valuation methodology, and the sector concentration buried in the LP agreement."

— UAO Research.

— Three links worth your time —

- Thinking Ahead Institute — Total Portfolio Approach research hub. The clearest evidence base behind the operating model CalPERS is about to adopt — read it before the July 1 go-live.

- Financial Stability Board — Report on Vulnerabilities in Private Credit (6 May 2026). The official-sector framing of the data gaps underneath Item 1; short and primary.

- GIC — GIC leads Anthropic's $30bn Series G. A reminder, from February, that the same long-horizon owners adding private credit are also the marginal underwriters of the AI build-out.

Presented by [Quarterly Sponsor].

This slot is open. The UAO Daily Brief reaches the people who allocate long-horizon capital. One quarterly founding sponsor, editorial firewall: sponsors@universalassetowners.com.

UAO Daily Brief is the morning briefing for the people who allocate long-horizon capital. Five minutes, five days a week.

Become a Premium subscriber · Listen: The Allocator Briefing · Forward to a colleague · Manage preferences

UniversalAssetOwners.com. Capital at the scale of the world.