Volume 1, Issue 12. Tuesday, May 19, 2026. Sent 7:00 am ET / 14:00 GST.

The world's largest sovereign fund admitted this week that three straight years of negative relative returns are mostly a real-estate story, and laid out a sector-based replacement strategy explicitly weighted toward logistics and "living." Reading across to the kingdom that is most actively rewiring its own capital plumbing: PIF's $100 million anchor in State Street's new SAQL UCITS ETF — already listed on Deutsche Börse and the London Stock Exchange — is now a working front door for foreign institutional flows. Ontario Teachers' confirmed it cut its US-dollar exposure by 56 percent. Underneath all of it: a Financial Stability Board report flagging private credit's transparency problem, and another quarter of hyperscaler capex numbers that put 2026 spend on track for a trillion dollars — with sovereign-state vehicles now an explicit underwriting line. Five items, one chart, one take.

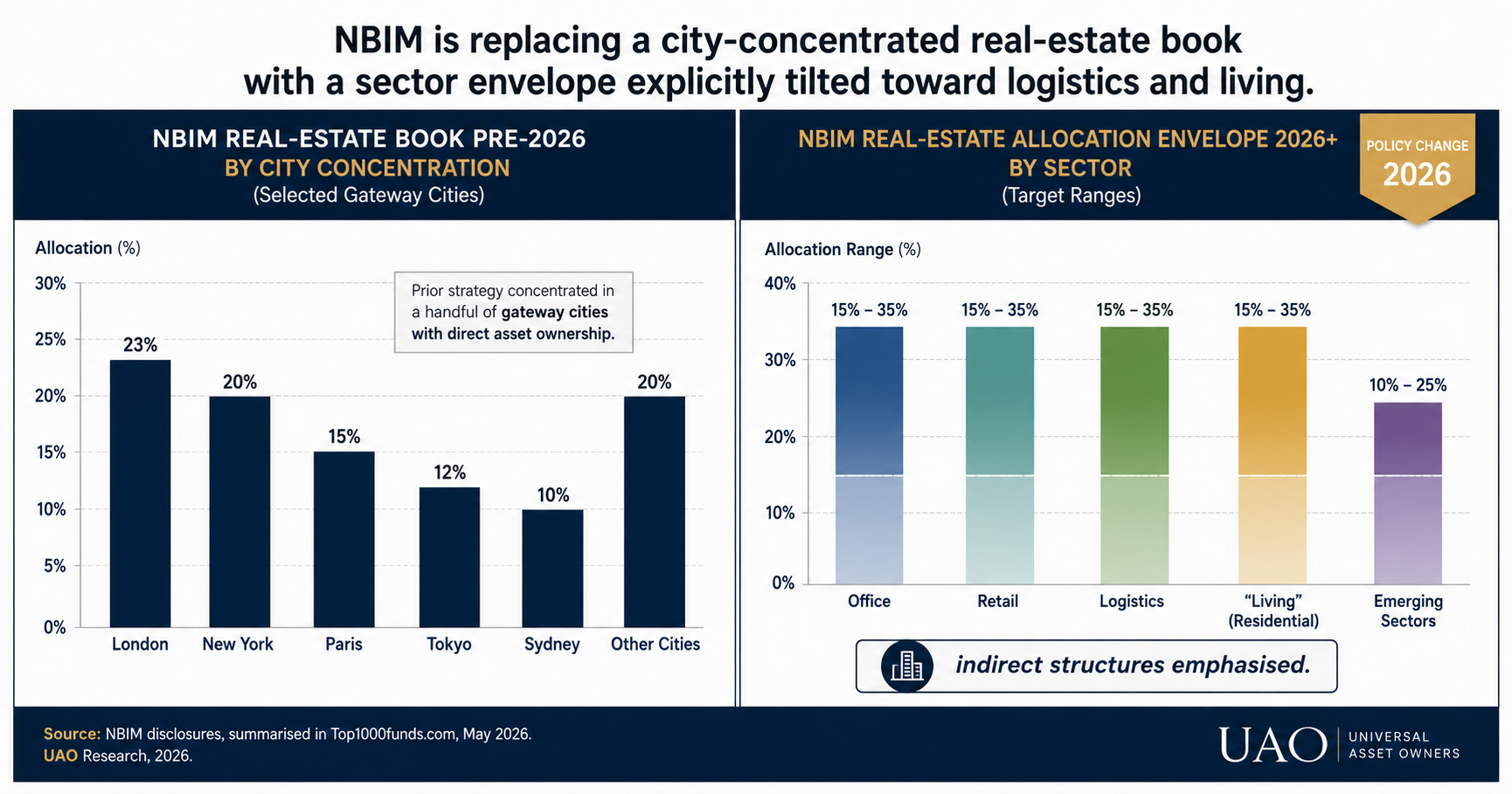

1. NBIM concedes its real-estate strategy underperformed, and bets the pivot on logistics and "living."

Norges Bank Investment Management chief executive Nicolai Tangen told the Norwegian parliament this week that the $2.1 trillion Government Pension Fund Global is "not satisfied" with its real-estate portfolio, which Tangen named as the main contributor to three consecutive years of negative relative returns. The replacement framework drops the fund's prior gateway-cities approach in favour of four sector pillars — office, retail, logistics, and "living" (residential) — each given a 15–35 percent allocation range, with emerging sectors allowed 10–25 percent. The fund will also lean further on "indirect structures," meaning more capital through real-estate platforms and funds rather than direct asset ownership.

For a universal owner, what NBIM is saying out loud is that geographic diversification across a handful of gateway cities did not solve the problem the asset class was bought to solve, and that the next decade's defensible real estate is closer to the AI build-out — logistics, data-centre-adjacent industrial, multi-family — than to trophy offices. The half-year report, due at Arendalsuka, will reveal how fast the book is moving.

Source: NBIM lays out case for real estate turnaround, Top1000funds.com, May 2026. | Coverage: Sovereign Wealth Monitor, this week.

2. The PIF / State Street Saudi ETF is now trading — a $100m anchor and a UCITS structure point at where the kingdom wants institutional flows to come from.

State Street's Saudi Arabia Enhanced Active Equity UCITS ETF — ticker SAQL — listed on Deutsche Börse on 16 April 2026 and on the London Stock Exchange on 20 April, anchored by a $100 million commitment from the Public Investment Fund. The vehicle is an active, not index, strategy designed to outperform Saudi listed equities over the medium term, and it sits in the UCITS wrapper — the European-domiciled structure most non-US institutional allocators already use.

The choice is the tell. A UCITS vehicle in Frankfurt and London is built to absorb pension, insurance, and sovereign flows out of Europe, the UK, the Gulf, and Asia rather than US 40-Act money. Combined with PIF's anchor capital and a global asset manager's name on the prospectus, it is the most institutionally-legible front door into Saudi listed equities from a state issuer mid-Vision-2030 — and a signal that the kingdom is willing to underwrite the plumbing that long-horizon foreign capital actually uses. The number to watch over the next two quarters is non-PIF flows: a SAQL book that grows past its anchor is the story.

Source: State Street launches Saudi Arabia active equity ETF with $100m PIF backing, QuotedData, 22 April 2026. Corroborating: PIF anchors State Street's newly launched Saudi equity ETF, PIF press release, 2026. · PIF anchors State Street's Saudi equity ETF: SAQL, ETF Express, 22 April 2026.

3. OTPP cut its US-dollar exposure by 56 percent — a quiet currency reroute from a closely-watched plan.

Ontario Teachers' Pension Plan reported a 6.7 percent one-year net return for 2025 and a $31.2 billion preliminary funding surplus at the start of 2026, with the plan fully funded. The headline inside the disclosure: OTPP cut its net US-dollar exposure from C$90.9 billion at the end of 2024 to C$41.3 billion at the end of 2025 — a 56 percent reduction, the lowest level since mid-2021 — as the Canadian dollar surged more than 5 percent in the first half of the year. Total foreign-currency net exposure fell to C$99.4 billion from C$142 billion. The plan also appointed Feifei Wu as senior managing director, investment technology and applied intelligence, on May 4.

OTPP's hedging shift is, on its own, one fund's decision. As a data point inside the broader 2025–26 pattern — Canadian and European plans reweighting toward home-currency assets and tightening dollar hedges — it is more telling. Universal owners with a non-USD funding base are increasingly willing to tolerate the carry cost of hedging in exchange for the smoother glide path; the question for the next twelve months is whether the move accelerates if the dollar trends weaker into year-end.

Source: Ontario Teachers' announces positive 2025 results, OTPP, 2026. Corroborating: Ontario Teachers Cuts US Dollar Exposure By 56%, Bloomberg, 12 August 2025. · Loonie surge drives OTPP to slash US dollar exposure, Benefits and Pensions Monitor, 2026.

4. The FSB names private credit's transparency problem — and the insurance balance sheet is the conduit.

The Financial Stability Board's May 6 report on private-credit vulnerabilities estimates the global market at $1.5 to $2 trillion and flags valuation opacity, the prevalence of private credit ratings (used in place of public ratings), and sector concentration in technology, healthcare, and services. The IMF's April 2026 Global Financial Stability Report separately notes that private credit now accounts for roughly 35 percent of North American insurance investment portfolios, and that the conflicts of interest inside private-equity-owned or PE-managed insurers create transparency and surveillance problems regulators have not yet matched with policy.

For asset owners with insurance exposure on either side — large allocations to insurance-linked debt, or insurance subsidiaries inside the corporate group — the surveillance gap is the live risk. The mechanism the FSB is most worried about is familiar: a firm- or sector-specific shock in private credit gets amplified by opaque valuations and concentrated holdings, lands on insurance balance sheets, and from there into the broader financial system. The report is a flag, not a forecast — but for universal owners, the right read is that the regulatory perimeter around private credit is going to widen.

Source: Report on Vulnerabilities in Private Credit, Financial Stability Board, 6 May 2026.

5. 2026 hyperscaler capex is on track to print near a trillion dollars — and sovereigns are now a financing line.

Industry trackers now put 2026 compute capital expenditure at roughly $1.04 trillion: about $725 billion from the four largest hyperscalers, $80 billion from China, $50 billion from Oracle, $13 billion from Apple, $60 billion from neoclouds, $60 billion from sovereign-state vehicles, and a residual $48 billion from other sources. Roughly three-quarters of aggregate hyperscaler capex this year is AI-related — call it $450 billion of AI-specific spend.

The shape of the financing is the universal-owner story. Equity, corporate debt, secured asset-level financing, private credit, and sovereign capital are all in the stack, and the demand side concentrates on a small number of model-developer counterparties whose combined free cash flow remains negative. Universal owners sit on both sides — they own the hyperscalers in public equity, increasingly fund the infrastructure via private credit and direct platforms, and through their sovereign peers underwrite the marginal dollar. Concentration risk is the real question.

Source: AI Capex 2026 — The $690B Infrastructure Sprint, Futurum, 2026.

— Chart of the day —

Neplacing a city-concentrated real-estate book with a sector envelope explicitly tilted toward logistics and living.

Source: NBIM disclosures, summarised in Top1000funds.com, May 2026. UAO Research, 2026.

— Take of the day —

*"When a $2.1 trillion fund explicitly drops geographic diversification for sector allocation, the asset class has stopped being about cities and started being about cash-flow biology."