Volume 1, Issue 1. Friday, May 15, 2026. Sent 7:00 am ET / 14:00 GST.

A global regulator spent this month warning about private credit. The world's largest asset owners spent it allocating more. That gap — between the official risk frame and the allocation behaviour — is this morning's story, and it runs through the whole brief: the Financial Stability Board's first dedicated report on private credit, a record quarter of pension commitments to private markets, Norway's fund quantifying what fragmentation would cost it, and the AI build-out that keeps pulling long capital toward infrastructure.

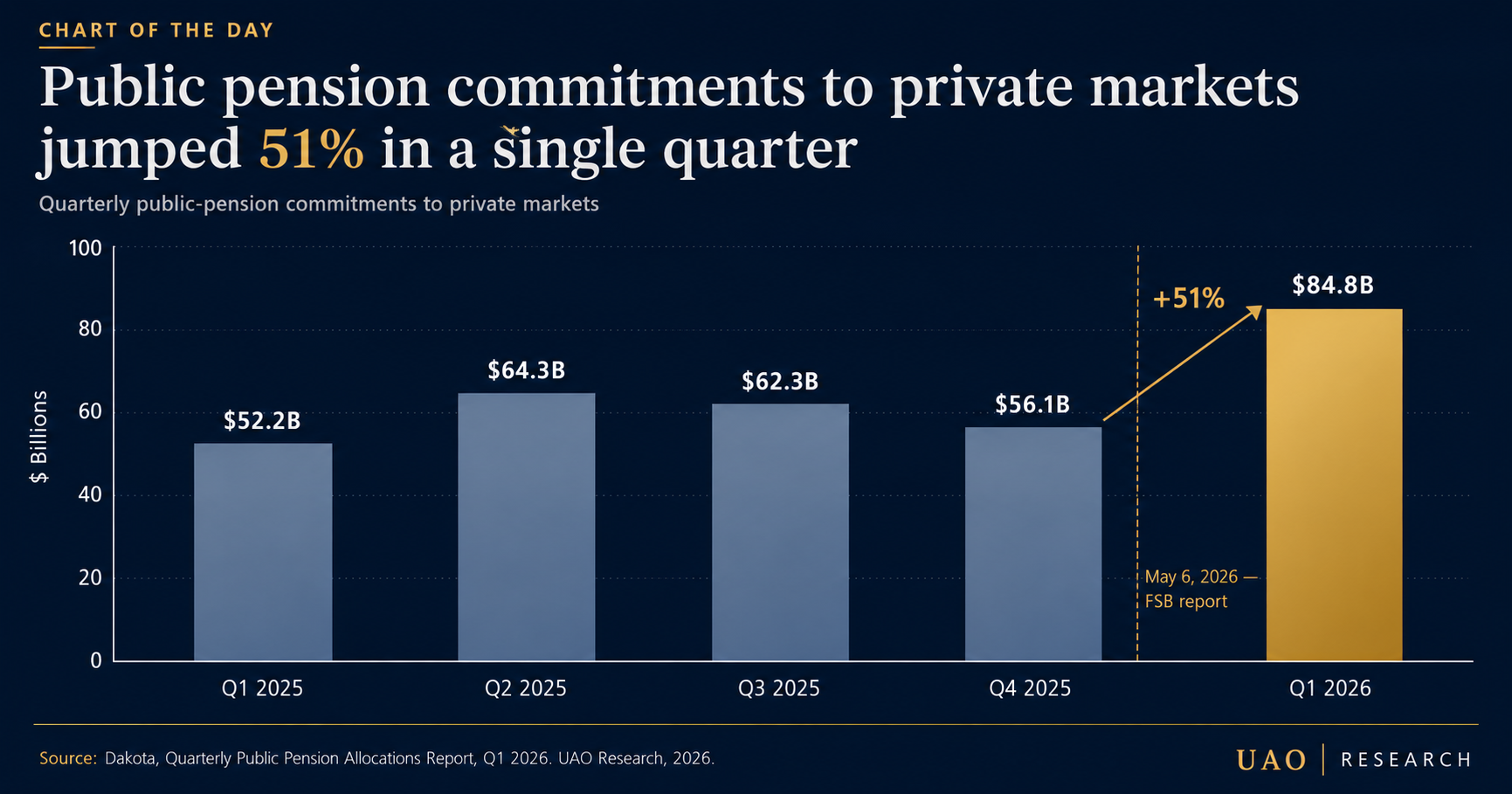

1. The FSB warned on private credit. Public pensions committed $84.8B anyway.

On May 6 the Financial Stability Board published its first dedicated Report on Vulnerabilities in Private Credit, putting the market at an estimated $1.5–2 trillion and naming four pressure points: leverage in opaque, multi-layered structures; liquidity risk from the spread of semi-liquid redemption-offering funds; concentration in technology, healthcare and services; and interlinkages with banks and insurers that the data cannot yet size — FSB members captured roughly $220 billion of bank credit lines to private credit funds, while the regulator notes the true figure could be more than twice that. Its blunt framing: the asset class has not been tested through a severe downturn.

The allocators are not waiting for that test. Public pensions committed $84.8 billion to private markets in the first quarter of 2026, up 51% from the fourth quarter, with corporate-lending and asset-backed credit strategies leading. The behaviour is rational on its own terms — these are long-dated, hard-to-unwind allocations, and owners are rotating within private credit toward middle-market and stronger-covenant deals rather than exiting. But the divergence between the regulator's caution and the allocation pace is the single most important thing on a universal owner's risk desk this week.

Source: FSB, Report on Vulnerabilities in Private Credit, May 6, 2026. | Pension data: Dakota, Q1 2026. | Coverage: Risk Radar, today.

2. Norway's fund put a number on fragmentation — and on an AI sell-off.

In a May 5 hearing on the management of the Government Pension Fund Global, Norges Bank Investment Management set out the risks it considers most threatening to a $2 trillion portfolio. Its stress testing identifies global economic fragmentation — alienated trade blocs, aggressive tariffs, investment restrictions — as the most damaging scenario modelled, capable of erasing more than a third of the fund's value. The second most damaging case is an AI-led market correction, which the fund estimates could cut its value by around 35%, driven by an equity book where the ten largest companies — seven of them US technology firms — now account for 21.3% of equity investments, a concentration the fund says it has never carried before.

For any universal owner running a large passive equity sleeve, NBIM is doing the public work of quantifying a risk most owners hold but few have sized.

Source: NBIM hearing testimony, May 5, 2026.

3. The AI build-out keeps pulling long capital into infrastructure.

The scale figures keep climbing. The four largest US hyperscalers are expected to deploy more than $650 billion of capital expenditure in 2026, most of it into AI data-centre capacity; Goldman Sachs estimates roughly $7.6 trillion of capital across compute, data centres and power between 2026 and 2031. Asset managers including BlackRock and Apollo are framing 2026 as the start of a "golden age" for private infrastructure, and pension, endowment and sovereign capital is rotating toward it — in many cases out of traditional fixed income.

The owner's question is not whether the capex is real. It is whether AI compute is being underwritten as infrastructure when its residual value, useful life and technology-obsolescence profile look nothing like a toll road. Item 1's covenant discipline applies here too.

Source: Goldman Sachs, "Tracking Trillions," 2026. | Coverage: AI & the Long-Term Portfolio, this month.

4. Sovereign capital: a US blueprint, a Canadian launch, a Gulf question.

The map of state capital is being redrawn. A US sovereign wealth fund blueprint was due in early May, following February's executive order. Canada launched the Canada Strong Fund, with roughly $18 billion in assets, in April — explicitly framed around financing strategic projects and reducing trade dependence. And the Council on Foreign Relations notes that the seven largest Gulf sovereign funds deployed an estimated $119 billion in 2025, most of it into the United States — capital that could partly reroute home if regional risk rises. New vehicles, new mandates, and a live question about where Gulf capital sits.

Source: CFR, "Disappearing Gulf Capital," 2026. | Coverage: Sovereign Wealth Monitor, Tuesday.

— Chart of the day —

Public pension commitments to private markets jumped 51% in a single quarter.

— Take of the day —

"A regulator's warning and an allocator's commitment are not in contradiction — they are two clocks running at different speeds. The FSB is pricing a tail; the pension is pricing a mandate it cannot fund any other way. The universal owner's job this quarter is to hold both clocks at once: keep allocating, and document — in covenants, liquidity terms and manager selection — exactly what would have to be true for the tail not to matter."

— UAO Research.

— Three links worth your time —

- Financial Stability Board. Report on Vulnerabilities in Private Credit (May 6). The primary document behind item 1 — read the section on bank interlinkages and the proposed common metrics.

- Norges Bank. Financial Stability Report 2026-1 (May 12). NBIM's parent on bank resilience to market stress; useful read alongside the fund's own stress tests.

- U.S. Office of Financial Research. Brief 26-02, Measuring Counterparty Exposures to Private Credit (March). The most concrete attempt yet to size who is actually on the other side of the trade.

UAO Daily Brief is the morning briefing for the people who allocate long-horizon capital. Five minutes, five days a week.

[Forward to a colleague] | [Manage preferences] | [Become a Premium subscriber] | [Listen: The Allocator Briefing]

UniversalAssetOwners.com. Capital at the scale of the world.